Answered step by step

Verified Expert Solution

Question

1 Approved Answer

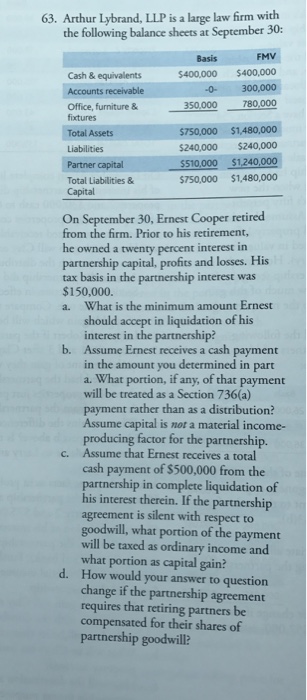

Arthur Lybrand, LLP is a large law firm with the following balance sheets at September 30: On September 30, Ernest Cooper retired from the firm.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computers Electronics And High Tech Industry Irs Audit Techniques Guide

Authors: Internal Revenue Service

1st Edition

1304133834, 978-1304133830