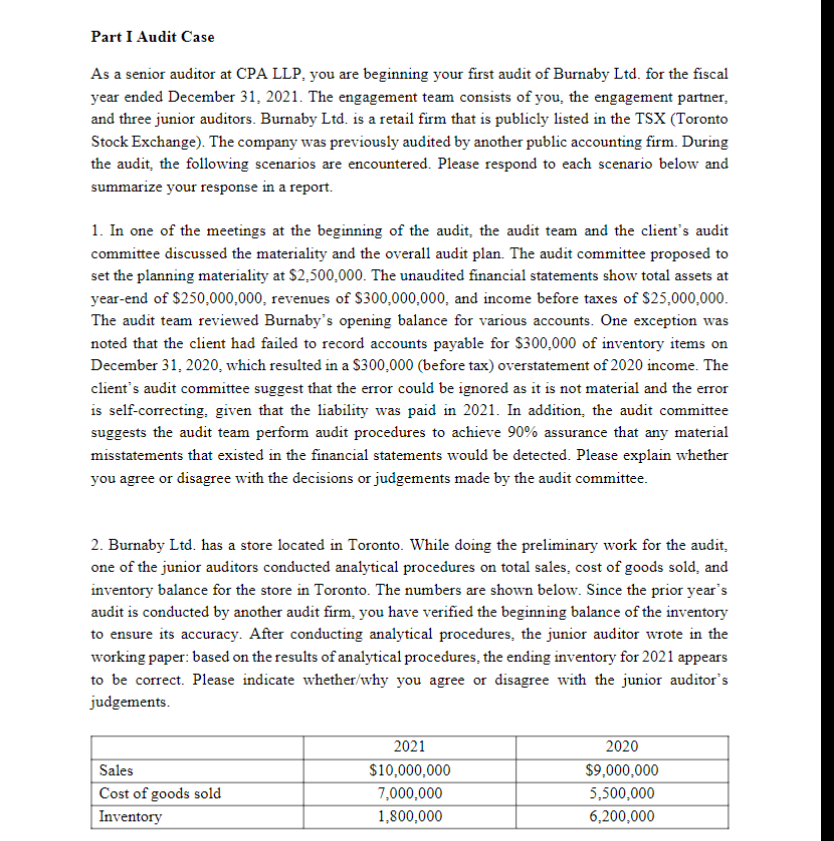

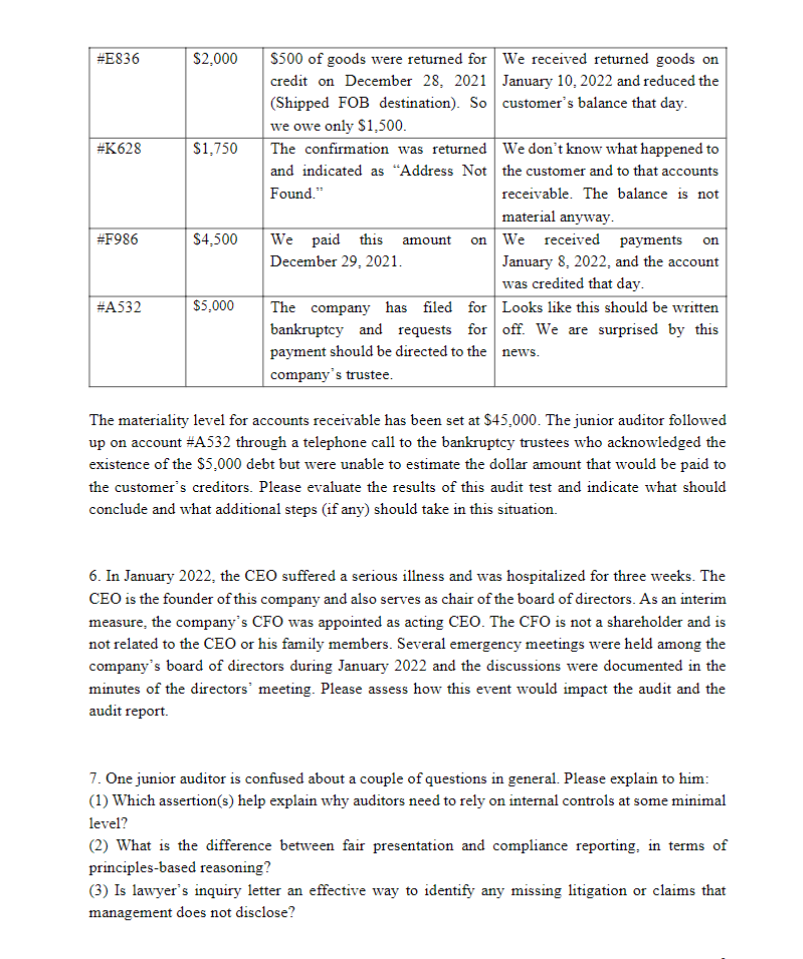

As a senior auditor at CPA LLP, you are beginning your first audit of Burnaby Ltd. for the fiscal year ended December 31, 2021. The engagement team consists of you, the engagement partner, and three junior auditors. Burnaby Ltd. is a retail firm that is publicly listed in the TSX (Toronto Stock Exchange). The company was previously audited by another public accounting firm. During the audit, the following scenarios are encountered. Please respond to each scenario below and summarize your response in a report. 1. In one of the meetings at the beginning of the audit, the audit team and the client's audit committee discussed the materiality and the overall audit plan. The audit committee proposed to set the planning materiality at $2,500,000. The unaudited financial statements show total assets at year-end of $250,000,000, revenues of $300,000,000, and income before taxes of $25,000,000. The audit team reviewed Burnaby's opening balance for various accounts. One exception was noted that the client had failed to record accounts payable for $300,000 of inventory items on December 31, 2020, which resulted in a $300,000 (before tax) overstatement of 2020 income. The client's audit committee suggest that the error could be ignored as it is not material and the error is self-correcting, given that the liability was paid in 2021. In addition, the audit committee suggests the audit team perform audit procedures to achieve 90% assurance that any material misstatements that existed in the financial statements would be detected. Please explain whether you agree or disagree with the decisions or judgements made by the audit committee. 2. Burnaby Ltd. has a store located in Toronto. While doing the preliminary work for the audit, one of the junior auditors conducted analytical procedures on total sales, cost of goods sold, and inventory balance for the store in Toronto. The numbers are shown below. Since the prior year's audit is conducted by another audit firm, you have verified the beginning balance of the inventory to ensure its accuracy. After conducting analytical procedures, the junior auditor wrote in the working paper: based on the results of analytical procedures, the ending inventory for 2021 appears to be correct. Please indicate whether/why you agree or disagree with the junior auditor's judgements. 3. When auditing the payroll, the junior auditors studied the company's payroll processing systems, completed an internal control questionnaire for payrolls, and verified the details of 50 payroll transactions during September 2021. No exceptions were found in this test. The only weakness noted was that the company often hires "casual laborers" to work on certain jobs and pays these laborers in cash. The supervisor on every job has control over a petty cash fund (usually $5,000 ) designated for that purpose and is authorized by management to make such payments. The supervisor submits a list of laborers and amounts paid as "casual labor" to the head office at the end of each week and receives reimbursement. When a job is completed, the supervisor returns any excess cash to the company and the fund is closed out on the books. According to the company's records, about 5% of payroll expenses were handled in this manner during the fiscal year. Based on studies of the client's system, the junior auditors suggest concluding that control risk over payroll transactions was low, except in the area of casual labor, where the risk should be set to maximum. Junior auditors further comment that while controls over payments to casual laborers are poor, there is no effect on the financial statements. Please indicate whether/why you agree or disagree with the junior auditors' assessments. 4. An assessment of goodwill impairment is conducted by the management. The goodwill is resulted from previous mergers and acquisitions. During the impairment testing, a discounted cash flow (DCF) is estimated based on internal forecasts (developed using historical financial data) that are subject to a rigorous process and management has demonstrated an ability to accurately forecast. While largely consistent with forecasts used for other internal analysis and tracking, the forecasts used in the goodwill DCF are modified prior to being used elsewhere. Management is using a projected revenue growth rate that is consistent with industry expectations and historical results. Please analyze the risk of material misstatement with the goodwill impairment testing process and suggest appropriate audit procedures. 5. When audit accounts receivable, following your instruction, a junior auditor sent 30 positive confirmation requests to a random sample of customers as the substantive procedure. The recorded accounts receivable total $600,000 and include 210 individual customer accounts. Of the 30 confirmations received from the customers, 25 had no exceptions noted, while 5 confirmations yielded the following results: The materiality level for accounts receivable has been set at $45,000. The junior auditor followed up on account \#A532 through a telephone call to the bankruptcy trustees who acknowledged the existence of the $5,000 debt but were unable to estimate the dollar amount that would be paid to the customer's creditors. Please evaluate the results of this audit test and indicate what should conclude and what additional steps (if any) should take in this situation. 6. In January 2022, the CEO suffered a serious illness and was hospitalized for three weeks. The CEO is the founder of this company and also serves as chair of the board of directors. As an interim measure, the company's CFO was appointed as acting CEO. The CFO is not a shareholder and is not related to the CEO or his family members. Several emergency meetings were held among the company's board of directors during January 2022 and the discussions were documented in the minutes of the directors' meeting. Please assess how this event would impact the audit and the audit report. 7. One junior auditor is confused about a couple of questions in general. Please explain to him: (1) Which assertion(s) help explain why auditors need to rely on internal controls at some minimal level? (2) What is the difference between fair presentation and compliance reporting, in terms of principles-based reasoning? (3) Is lawyer's inquiry letter an effective way to identify any missing litigation or claims that management does not disclose? As a senior auditor at CPA LLP, you are beginning your first audit of Burnaby Ltd. for the fiscal year ended December 31, 2021. The engagement team consists of you, the engagement partner, and three junior auditors. Burnaby Ltd. is a retail firm that is publicly listed in the TSX (Toronto Stock Exchange). The company was previously audited by another public accounting firm. During the audit, the following scenarios are encountered. Please respond to each scenario below and summarize your response in a report. 1. In one of the meetings at the beginning of the audit, the audit team and the client's audit committee discussed the materiality and the overall audit plan. The audit committee proposed to set the planning materiality at $2,500,000. The unaudited financial statements show total assets at year-end of $250,000,000, revenues of $300,000,000, and income before taxes of $25,000,000. The audit team reviewed Burnaby's opening balance for various accounts. One exception was noted that the client had failed to record accounts payable for $300,000 of inventory items on December 31, 2020, which resulted in a $300,000 (before tax) overstatement of 2020 income. The client's audit committee suggest that the error could be ignored as it is not material and the error is self-correcting, given that the liability was paid in 2021. In addition, the audit committee suggests the audit team perform audit procedures to achieve 90% assurance that any material misstatements that existed in the financial statements would be detected. Please explain whether you agree or disagree with the decisions or judgements made by the audit committee. 2. Burnaby Ltd. has a store located in Toronto. While doing the preliminary work for the audit, one of the junior auditors conducted analytical procedures on total sales, cost of goods sold, and inventory balance for the store in Toronto. The numbers are shown below. Since the prior year's audit is conducted by another audit firm, you have verified the beginning balance of the inventory to ensure its accuracy. After conducting analytical procedures, the junior auditor wrote in the working paper: based on the results of analytical procedures, the ending inventory for 2021 appears to be correct. Please indicate whether/why you agree or disagree with the junior auditor's judgements. 3. When auditing the payroll, the junior auditors studied the company's payroll processing systems, completed an internal control questionnaire for payrolls, and verified the details of 50 payroll transactions during September 2021. No exceptions were found in this test. The only weakness noted was that the company often hires "casual laborers" to work on certain jobs and pays these laborers in cash. The supervisor on every job has control over a petty cash fund (usually $5,000 ) designated for that purpose and is authorized by management to make such payments. The supervisor submits a list of laborers and amounts paid as "casual labor" to the head office at the end of each week and receives reimbursement. When a job is completed, the supervisor returns any excess cash to the company and the fund is closed out on the books. According to the company's records, about 5% of payroll expenses were handled in this manner during the fiscal year. Based on studies of the client's system, the junior auditors suggest concluding that control risk over payroll transactions was low, except in the area of casual labor, where the risk should be set to maximum. Junior auditors further comment that while controls over payments to casual laborers are poor, there is no effect on the financial statements. Please indicate whether/why you agree or disagree with the junior auditors' assessments. 4. An assessment of goodwill impairment is conducted by the management. The goodwill is resulted from previous mergers and acquisitions. During the impairment testing, a discounted cash flow (DCF) is estimated based on internal forecasts (developed using historical financial data) that are subject to a rigorous process and management has demonstrated an ability to accurately forecast. While largely consistent with forecasts used for other internal analysis and tracking, the forecasts used in the goodwill DCF are modified prior to being used elsewhere. Management is using a projected revenue growth rate that is consistent with industry expectations and historical results. Please analyze the risk of material misstatement with the goodwill impairment testing process and suggest appropriate audit procedures. 5. When audit accounts receivable, following your instruction, a junior auditor sent 30 positive confirmation requests to a random sample of customers as the substantive procedure. The recorded accounts receivable total $600,000 and include 210 individual customer accounts. Of the 30 confirmations received from the customers, 25 had no exceptions noted, while 5 confirmations yielded the following results: The materiality level for accounts receivable has been set at $45,000. The junior auditor followed up on account \#A532 through a telephone call to the bankruptcy trustees who acknowledged the existence of the $5,000 debt but were unable to estimate the dollar amount that would be paid to the customer's creditors. Please evaluate the results of this audit test and indicate what should conclude and what additional steps (if any) should take in this situation. 6. In January 2022, the CEO suffered a serious illness and was hospitalized for three weeks. The CEO is the founder of this company and also serves as chair of the board of directors. As an interim measure, the company's CFO was appointed as acting CEO. The CFO is not a shareholder and is not related to the CEO or his family members. Several emergency meetings were held among the company's board of directors during January 2022 and the discussions were documented in the minutes of the directors' meeting. Please assess how this event would impact the audit and the audit report. 7. One junior auditor is confused about a couple of questions in general. Please explain to him: (1) Which assertion(s) help explain why auditors need to rely on internal controls at some minimal level? (2) What is the difference between fair presentation and compliance reporting, in terms of principles-based reasoning? (3) Is lawyer's inquiry letter an effective way to identify any missing litigation or claims that management does not disclose