Answered step by step

Verified Expert Solution

Question

1 Approved Answer

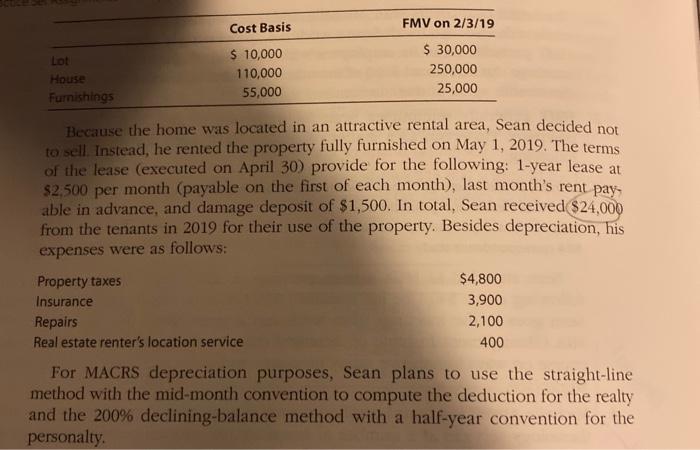

As Lucy's sole heir, Sean inherited her home and its furnishings Clocated at 5422 SW Sena Drive, Topeka, KS 66604). The costs and values involved

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Succeeding in Business with Microsoft Excel 2013 A Problem Solving Approach

Authors: Debra Gross, Frank Akaiwa, Karleen Nordquist

1st edition

978-1285099149, 9781285963969, 1285099141, 1285963962, 978-1285715346