Answered step by step

Verified Expert Solution

Question

1 Approved Answer

asap One-Period Model - Option Pricing Consider the following discrete time one period market model. The interest rate is zero. The stock price is given

asap

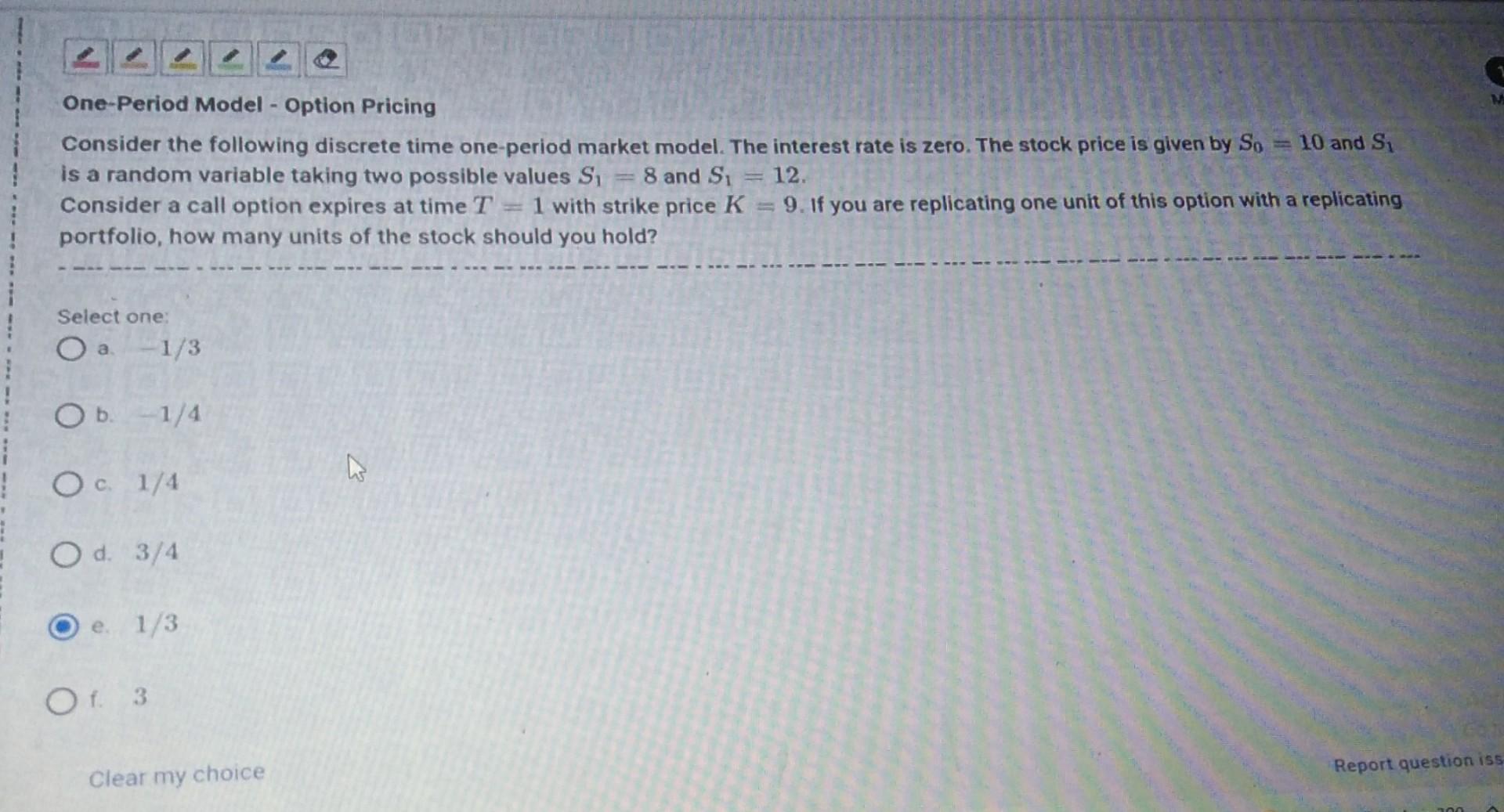

One-Period Model - Option Pricing Consider the following discrete time one period market model. The interest rate is zero. The stock price is given by So =10 and Si is a random variable taking two possible values Si 8 and Si 12. Consider a call option expires at time T 1 with strike price K : 9. If you are replicating one unit of this option with a replicating portfolio, how many units of the stock should you hold? Select one Oa - 1/3 Ob. 1/4 O c. 1/4 O d. 3/4 e. 1/3 Of. 3 Report question iss Clear my choice 100Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Pillars Of Finance The Misalignment Of Finance Theory And Investment Practice

Authors: G. Fraser-Sampson

2014th Edition

1137264055, 978-1137264053