Answered step by step

Verified Expert Solution

Question

1 Approved Answer

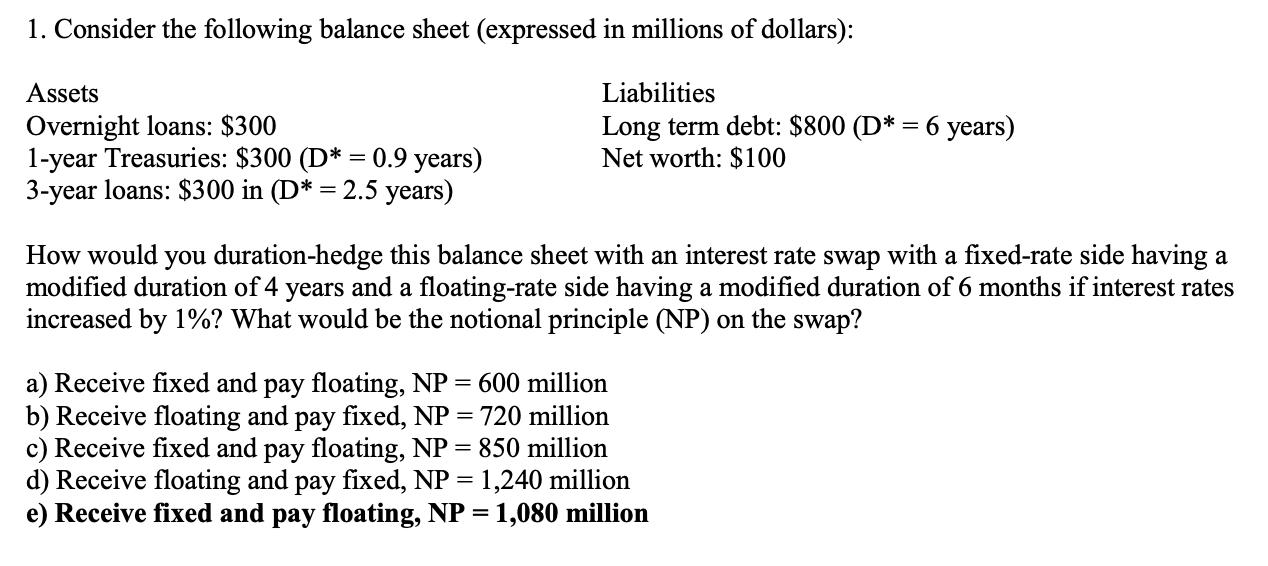

1. Consider the following balance sheet (expressed in millions of dollars): Assets Overnight loans: $300 1-year Treasuries: $300 (D* = 0.9 years) 3-year loans:

1. Consider the following balance sheet (expressed in millions of dollars): Assets Overnight loans: $300 1-year Treasuries: $300 (D* = 0.9 years) 3-year loans: $300 in (D* = 2.5 years) Liabilities Long term debt: $800 (D* = 6 years) Net worth: $100 How would you duration-hedge this balance sheet with an interest rate swap with a fixed-rate side having a modified duration of 4 years and a floating-rate side having a modified duration of 6 months if interest rates increased by 1%? What would be the notional principle (NP) on the swap? a) Receive fixed and pay floating, NP = 600 million b) Receive floating and pay fixed, NP = 720 million c) Receive fixed and pay floating, NP = 850 million d) Receive floating and pay fixed, NP = 1,240 million e) Receive fixed and pay floating, NP = 1,080 million

Step by Step Solution

★★★★★

3.43 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

In order to durationhedge the balance sheet the goal is to make the duration of assets DA match the duration of liabilities DL The durations provided ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Survey of Mathematics with Applications

Authors: Allen R. Angel, Christine D. Abbott, Dennis Runde

10th edition

134112105, 134112342, 9780134112343, 9780134112268, 134112261, 978-0134112107