Answered step by step

Verified Expert Solution

Question

1 Approved Answer

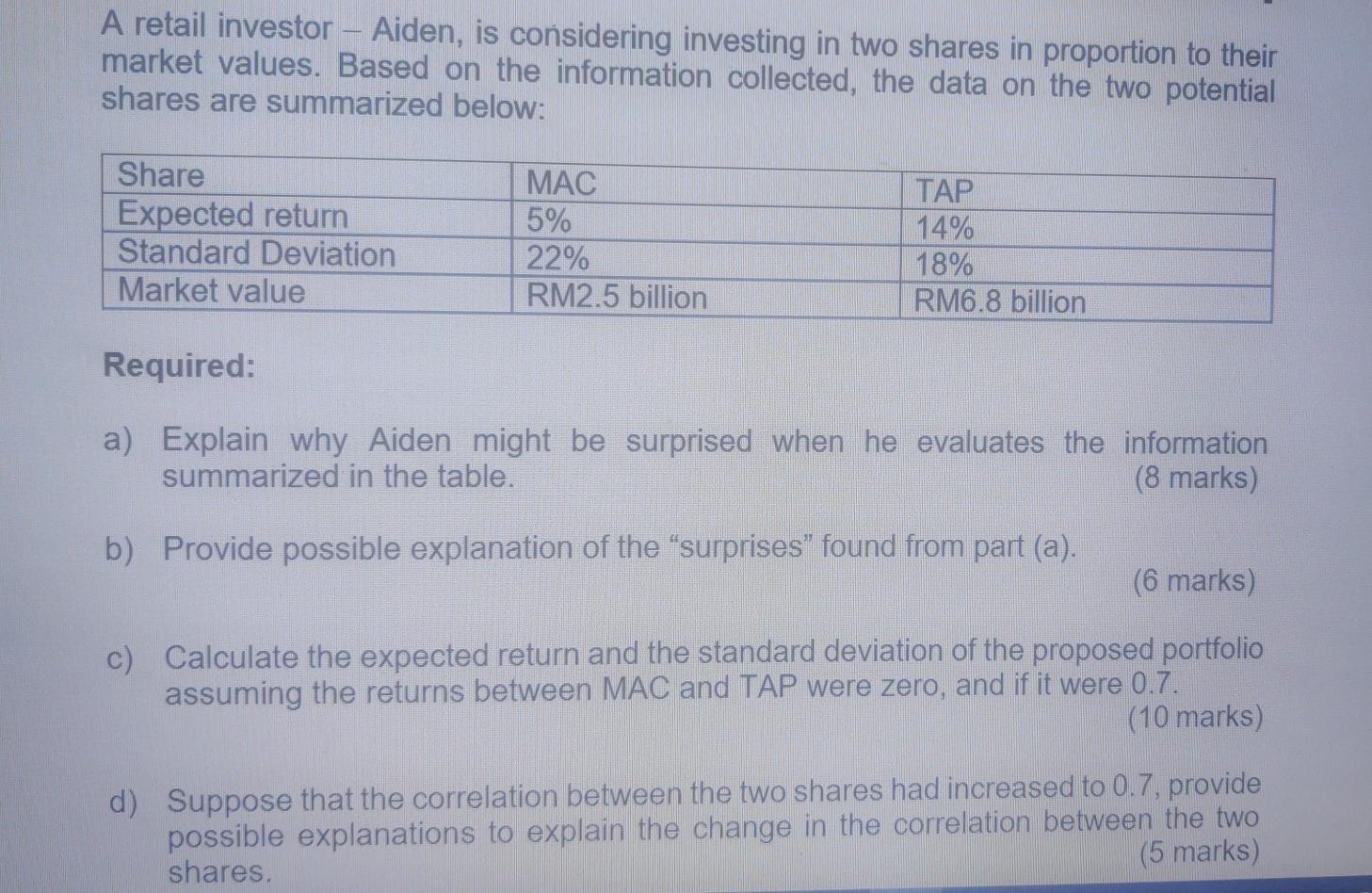

Ask for extra questions if required. A retail investor - Aiden, is considering investing in two shares in proportion to their market values. Based on

Ask for extra questions if required.

A retail investor - Aiden, is considering investing in two shares in proportion to their market values. Based on the information collected, the data on the two potential shares are summarized below: Share Expected return Standard Deviation Market value MAC 5% 22% RM2.5 billion TAP 14% 18% RM6.8 billion Required: a) Explain why Aiden might be surprised when he evaluates the information summarized in the table. (8 marks) b) Provide possible explanation of the surprises found from part (a). (6 marks) c) Calculate the expected return and the standard deviation of the proposed portfolio assuming the returns between MAC and TAP were zero, and if it were 0.7. (10 marks) d) Suppose that the correlation between the two shares had increased to 0.7, provide possible explanations to explain the change in the correlation between the two shares. (5 marks) A retail investor - Aiden, is considering investing in two shares in proportion to their market values. Based on the information collected, the data on the two potential shares are summarized below: Share Expected return Standard Deviation Market value MAC 5% 22% RM2.5 billion TAP 14% 18% RM6.8 billion Required: a) Explain why Aiden might be surprised when he evaluates the information summarized in the table. (8 marks) b) Provide possible explanation of the surprises found from part (a). (6 marks) c) Calculate the expected return and the standard deviation of the proposed portfolio assuming the returns between MAC and TAP were zero, and if it were 0.7. (10 marks) d) Suppose that the correlation between the two shares had increased to 0.7, provide possible explanations to explain the change in the correlation between the two sharesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forex This Book Includes Forex Beginners Forex

Authors: Jordon Sykes

1st Edition

154063180X, 978-1540631800