Answered step by step

Verified Expert Solution

Question

1 Approved Answer

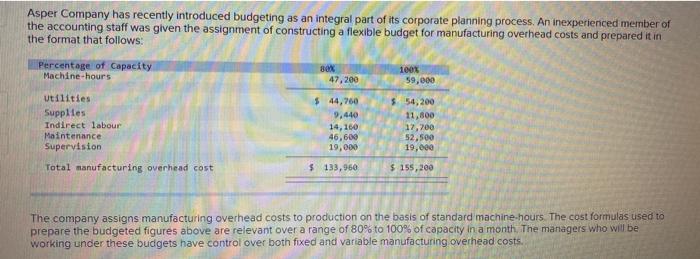

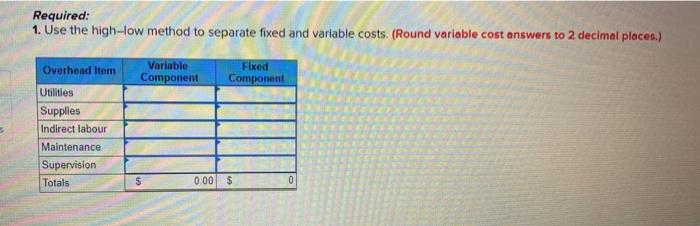

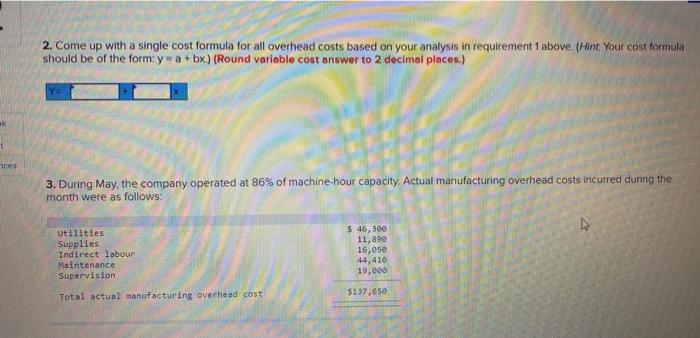

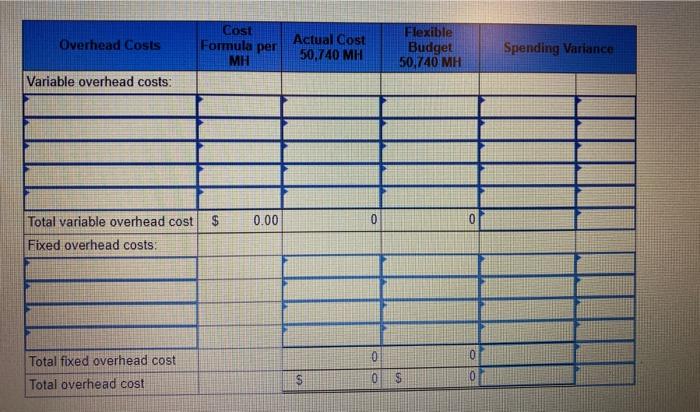

Asper Company has recently introduced budgeting as an integral part of its corporate planning process. An inexperienced member of the accounting staff was given the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

High Performance Cloud Auditing And Applications

Authors: Keesook J. Han, Baek-Young Choi, Sejun Song

1st Edition

1493944355, 978-1493944354