Answered step by step

Verified Expert Solution

Question

1 Approved Answer

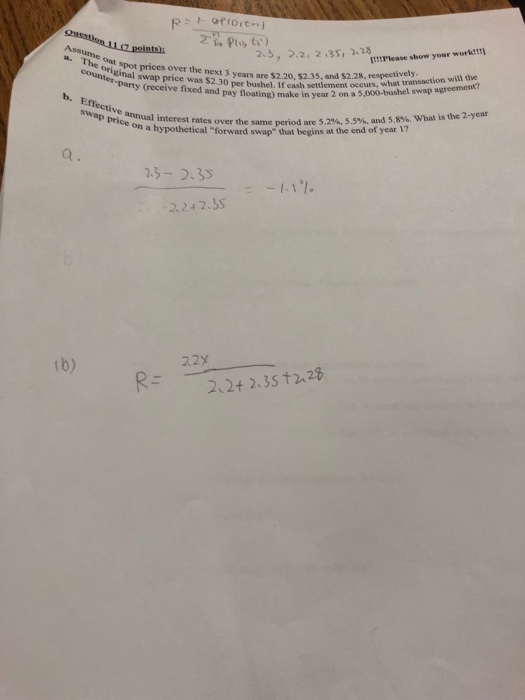

Ass 2.3, 2, 2,35, 2.23 um . The orig ipot prices over the next 3 years are $2.20, $2.35, and $2.28, reapehaineras,saction well dhe Ittt

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Concepts and Applications

Authors: Stephen Foerster

1st edition

013293664X, 978-0132936644