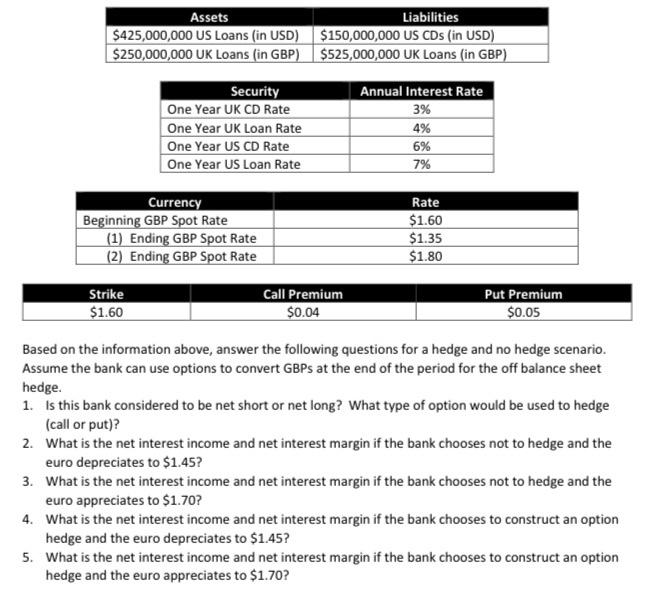

Assets Liabilities $425,000,000 US Loans (in USD) $150,000,000 US CDs (in USD) $250,000,000 UK Loans (in GBP) $525,000,000 UK Loans (in GBP) Annual Interest Rate 3% Security One Year UK CD Rate One Year UK Loan Rate One Year US CD Rate One Year US Loan Rate 4% 6% 7% Currency Beginning GBP Spot Rate (1) Ending GBP Spot Rate (2) Ending GBP Spot Rate Rate $1.60 $1.35 $1.80 Strike $1.60 Call Premium $0.04 Put Premium $0.05 Based on the information above, answer the following questions for a hedge and no hedge scenario. Assume the bank can use options to convert GBPs at the end of the period for the off balance sheet hedge. 1. Is this bank considered to be net short or net long? What type of option would be used to hedge (call or put)? 2. What is the net interest income and net interest margin if the bank chooses not to hedge and the euro depreciates to $1.45? 3. What is the net interest income and net interest margin if the bank chooses not to hedge and the euro appreciates to $1.70? 4. What is the net interest income and net interest margin if the bank chooses to construct an option hedge and the euro depreciates to $1.45? 5. What is the net interest income and net interest margin if the bank chooses to construct an option hedge and the euro appreciates to $1.70? Assets Liabilities $425,000,000 US Loans (in USD) $150,000,000 US CDs (in USD) $250,000,000 UK Loans (in GBP) $525,000,000 UK Loans (in GBP) Annual Interest Rate 3% Security One Year UK CD Rate One Year UK Loan Rate One Year US CD Rate One Year US Loan Rate 4% 6% 7% Currency Beginning GBP Spot Rate (1) Ending GBP Spot Rate (2) Ending GBP Spot Rate Rate $1.60 $1.35 $1.80 Strike $1.60 Call Premium $0.04 Put Premium $0.05 Based on the information above, answer the following questions for a hedge and no hedge scenario. Assume the bank can use options to convert GBPs at the end of the period for the off balance sheet hedge. 1. Is this bank considered to be net short or net long? What type of option would be used to hedge (call or put)? 2. What is the net interest income and net interest margin if the bank chooses not to hedge and the euro depreciates to $1.45? 3. What is the net interest income and net interest margin if the bank chooses not to hedge and the euro appreciates to $1.70? 4. What is the net interest income and net interest margin if the bank chooses to construct an option hedge and the euro depreciates to $1.45? 5. What is the net interest income and net interest margin if the bank chooses to construct an option hedge and the euro appreciates to $1.70