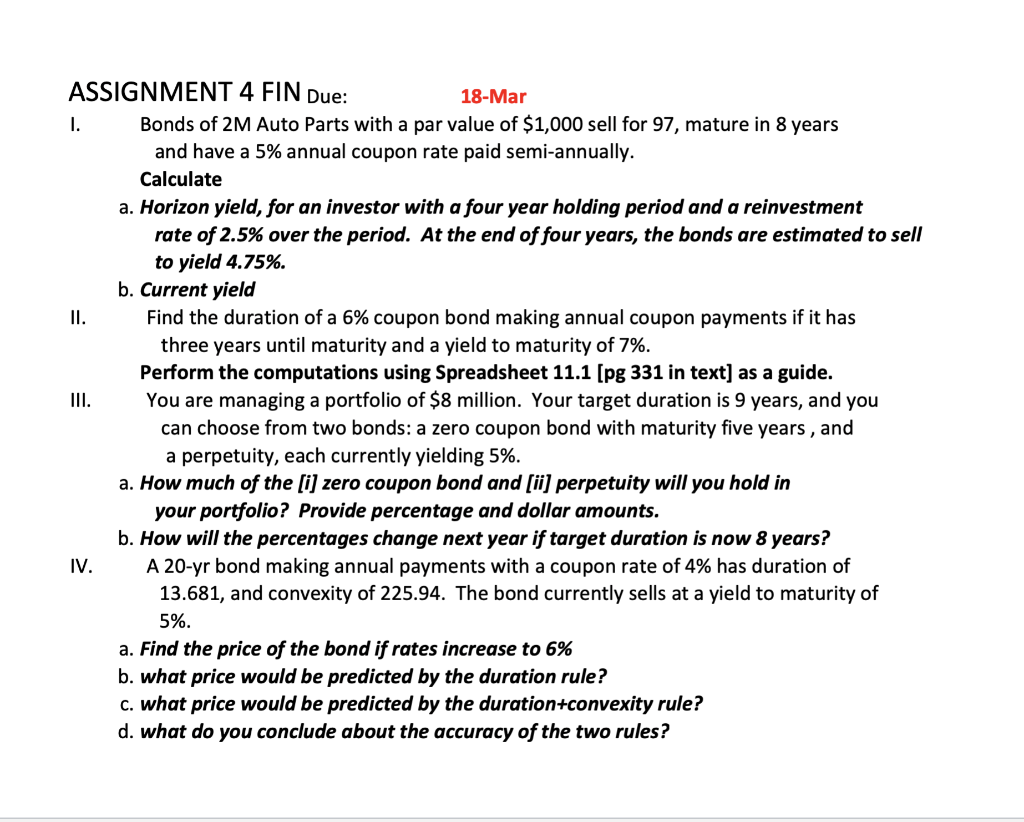

ASSIGNMENT 4 FIN Due: 18-Mar I. Bonds of 2M Auto Parts with a par value of $1,000 sell for 97, mature in 8 years and have a 5% annual coupon rate paid semi-annually. Calculate a. Horizon yield, for an investor with a four year holding period and a reinvestment rate of 2.5% over the period. At the end of four years, the bonds are estimated to sell to yield 4.75%. b. Current yield II. Find the duration of a 6% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7%. Perform the computations using Spreadsheet 11.1 [pg 331 in text] as a guide. III. You are managing a portfolio of $8 million. Your target duration is 9 years, and you can choose from two bonds: a zero coupon bond with maturity five years, and a perpetuity, each currently yielding 5%. a. How much of the [i] zero coupon bond and [ii] perpetuity will you hold in your portfolio? Provide percentage and dollar amounts. b. How will the percentages change next year if target duration is now 8 years? IV. A 20-yr bond making annual payments with a coupon rate of 4% has duration of 13.681, and convexity of 225.94. The bond currently sells at a yield to maturity of 5%. a. Find the price of the bond if rates increase to 6% b. what price would be predicted by the duration rule? C. what price would be predicted by the duration+convexity rule? d. what do you conclude about the accuracy of the two rules? ASSIGNMENT 4 FIN Due: 18-Mar I. Bonds of 2M Auto Parts with a par value of $1,000 sell for 97, mature in 8 years and have a 5% annual coupon rate paid semi-annually. Calculate a. Horizon yield, for an investor with a four year holding period and a reinvestment rate of 2.5% over the period. At the end of four years, the bonds are estimated to sell to yield 4.75%. b. Current yield II. Find the duration of a 6% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7%. Perform the computations using Spreadsheet 11.1 [pg 331 in text] as a guide. III. You are managing a portfolio of $8 million. Your target duration is 9 years, and you can choose from two bonds: a zero coupon bond with maturity five years, and a perpetuity, each currently yielding 5%. a. How much of the [i] zero coupon bond and [ii] perpetuity will you hold in your portfolio? Provide percentage and dollar amounts. b. How will the percentages change next year if target duration is now 8 years? IV. A 20-yr bond making annual payments with a coupon rate of 4% has duration of 13.681, and convexity of 225.94. The bond currently sells at a yield to maturity of 5%. a. Find the price of the bond if rates increase to 6% b. what price would be predicted by the duration rule? C. what price would be predicted by the duration+convexity rule? d. what do you conclude about the accuracy of the two rules