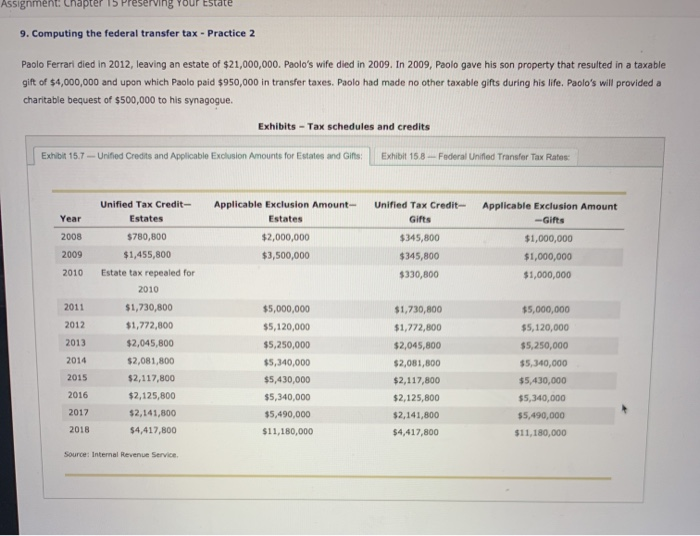

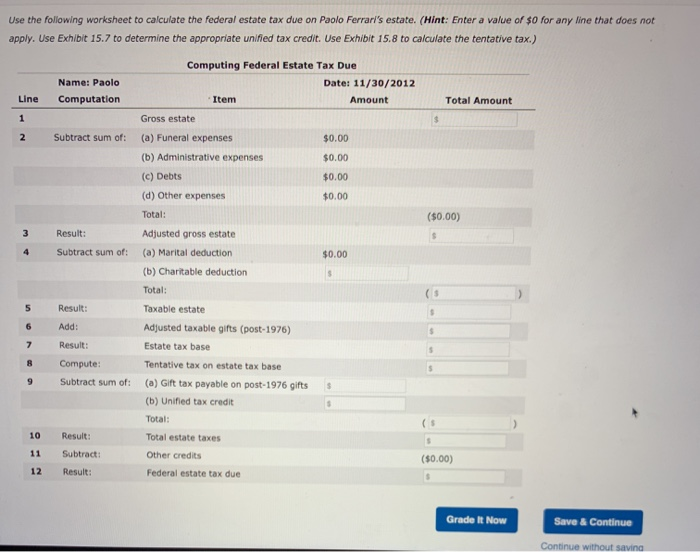

Assignment: Chapter erving Your Estate 9. Computing the federal transfer tax - Practice 2 Paolo Ferrari died in 2012, leaving an estate of $21,000,000. Paolo's wife died in 2009. In 2009, Paolo gave his son property that resulted in a taxable gift of $4,000,000 and upon which Paolo paid $950,000 in transfer taxes. Paolo had made no other taxable gifts during his life. Paolo's will provided a charitable bequest of $500,000 to his synagogue. Exhibits - Tax schedules and credits Exhibit 15.7 --- Unified Credits and Applicable Exclusion Amounts for Estates and Gifts Exhibit 158 -- Federal Unified Transfer Tax Rates: Unified Tax Credit- Estates Unified Tax Credit Gifts Applicable Exclusion Amount -Gifts Year 2008 2009 Applicable Exclusion Amount- Estates $2,000,000 $3,500,000 $780,800 $1,455,800 Estate tax repealed for 2010 $345,800 $345,800 $330,800 $1,000,000 $1,000,000 $1,000,000 2010 2011 2012 2013 2014 $1,730,800 $1,772,800 $2,045,800 $2,081,800 $2,117,800 $2,125,800 $5,000,000 $5,120,000 $5,250,000 $5,340,000 $5,430,000 $5,340,000 $5,490,000 $11,180,000 $1,730,800 $1,772,800 $2,045,800 $2,081,800 $2,117,800 $2,125,800 $2,141,800 $4,417,800 $5,000,000 $5,120,000 $5,250,000 $5,340,000 $5,430,000 $5,340,000 $5,490,000 $11,180,000 2015 2016 2017 $2,141,800 $4,417,800 2018 Source: Internal Revenue Service 1 3 Use the following worksheet to calculate the federal estate tax due on Paolo Ferrari's estate. (Hint: Enter a value of $0 for any line that does not apply. Use Exhibit 15.7 to determine the appropriate unified tax credit. Use Exhibit 15.8 to calculate the tentative tax.) Computing Federal Estate Tax Due Name: Paolo Date: 11/30/2012 Line Computation Item Amount Total Amount Gross estate $ 2 Subtract sum of: (a) Funeral expenses $0.00 (b) Administrative expenses $0.00 (c) Debts $0.00 (d) Other expenses $0.00 Total: ($0.00) Result: Adjusted gross estate $ Subtract sum of: (a) Marital deduction $0.00 (b) Charitable deduction Total: Result: Taxable estate . 6 Add: Adjusted taxable gifts (post-1976) 7 Result: Estate tax base Compute: Tentative tax on estate tax base S Subtract sum of: (a) Gift tax payable on post-1976 gifts $ (b) Unified tax credit . Total: 10 Result: Total estate taxes 11 Subtract: Other credits (50.00) 12 Result: Federal estate tax due 5 8 5 Grade It Now Save & Continue Continue without saving Assignment: Chapter erving Your Estate 9. Computing the federal transfer tax - Practice 2 Paolo Ferrari died in 2012, leaving an estate of $21,000,000. Paolo's wife died in 2009. In 2009, Paolo gave his son property that resulted in a taxable gift of $4,000,000 and upon which Paolo paid $950,000 in transfer taxes. Paolo had made no other taxable gifts during his life. Paolo's will provided a charitable bequest of $500,000 to his synagogue. Exhibits - Tax schedules and credits Exhibit 15.7 --- Unified Credits and Applicable Exclusion Amounts for Estates and Gifts Exhibit 158 -- Federal Unified Transfer Tax Rates: Unified Tax Credit- Estates Unified Tax Credit Gifts Applicable Exclusion Amount -Gifts Year 2008 2009 Applicable Exclusion Amount- Estates $2,000,000 $3,500,000 $780,800 $1,455,800 Estate tax repealed for 2010 $345,800 $345,800 $330,800 $1,000,000 $1,000,000 $1,000,000 2010 2011 2012 2013 2014 $1,730,800 $1,772,800 $2,045,800 $2,081,800 $2,117,800 $2,125,800 $5,000,000 $5,120,000 $5,250,000 $5,340,000 $5,430,000 $5,340,000 $5,490,000 $11,180,000 $1,730,800 $1,772,800 $2,045,800 $2,081,800 $2,117,800 $2,125,800 $2,141,800 $4,417,800 $5,000,000 $5,120,000 $5,250,000 $5,340,000 $5,430,000 $5,340,000 $5,490,000 $11,180,000 2015 2016 2017 $2,141,800 $4,417,800 2018 Source: Internal Revenue Service 1 3 Use the following worksheet to calculate the federal estate tax due on Paolo Ferrari's estate. (Hint: Enter a value of $0 for any line that does not apply. Use Exhibit 15.7 to determine the appropriate unified tax credit. Use Exhibit 15.8 to calculate the tentative tax.) Computing Federal Estate Tax Due Name: Paolo Date: 11/30/2012 Line Computation Item Amount Total Amount Gross estate $ 2 Subtract sum of: (a) Funeral expenses $0.00 (b) Administrative expenses $0.00 (c) Debts $0.00 (d) Other expenses $0.00 Total: ($0.00) Result: Adjusted gross estate $ Subtract sum of: (a) Marital deduction $0.00 (b) Charitable deduction Total: Result: Taxable estate . 6 Add: Adjusted taxable gifts (post-1976) 7 Result: Estate tax base Compute: Tentative tax on estate tax base S Subtract sum of: (a) Gift tax payable on post-1976 gifts $ (b) Unified tax credit . Total: 10 Result: Total estate taxes 11 Subtract: Other credits (50.00) 12 Result: Federal estate tax due 5 8 5 Grade It Now Save & Continue Continue without saving