Answered step by step

Verified Expert Solution

Question

1 Approved Answer

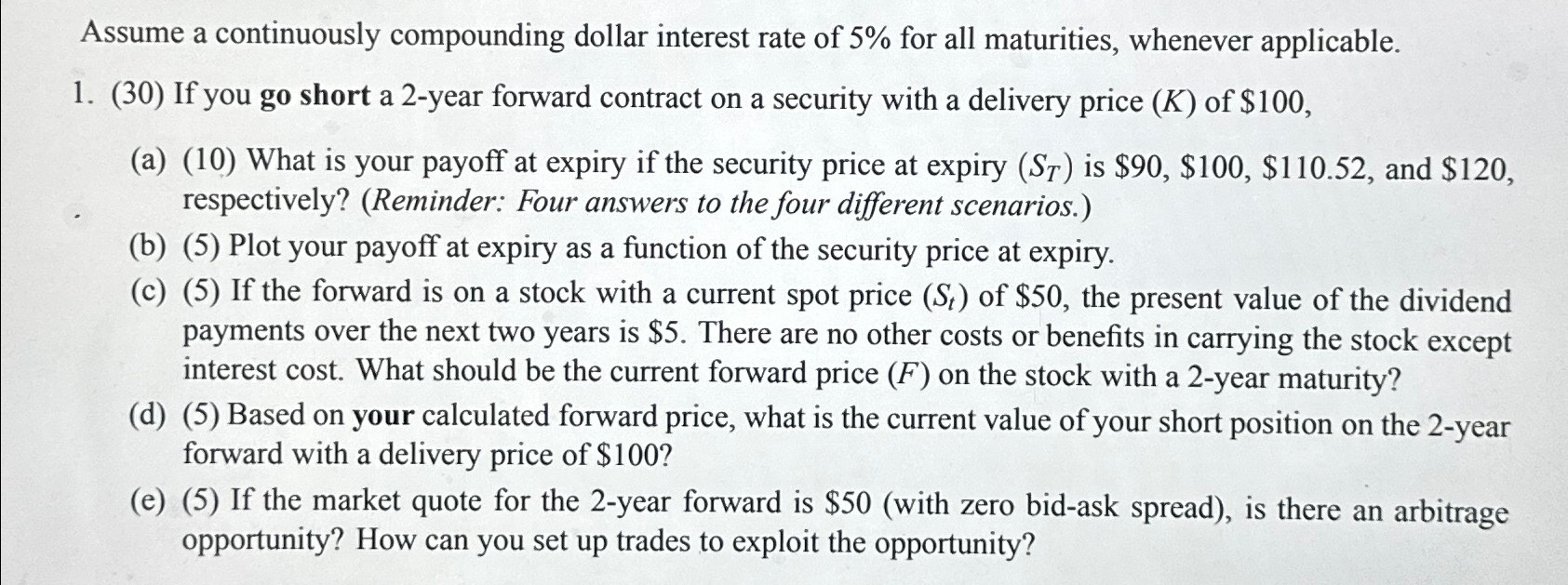

Assume a continuously compounding dollar interest rate of 5 % for all maturities, whenever applicable. If you go short a 2 - year forward contract

Assume a continuously compounding dollar interest rate of for all maturities, whenever applicable.

If you go short a year forward contract on a security with a delivery price of $

a What is your payoff at expiry if the security price at expiry is $$$ and $ respectively? Reminder: Four answers to the four different scenarios.

b Plot your payoff at expiry as a function of the security price at expiry.

c If the forward is on a stock with a current spot price of $ the present value of the dividend payments over the next two years is $ There are no other costs or benefits in carrying the stock except interest cost. What should be the current forward price on the stock with a year maturity?

d Based on your calculated forward price, what is the current value of your short position on the year forward with a delivery price of $

e If the market quote for the year forward is $with zero bidask spread is there an arbitrage opportunity? How can you set up trades to exploit the opportunity?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Development

Authors: Barbara Stallings

1st Edition

0815780850, 978-0815780854