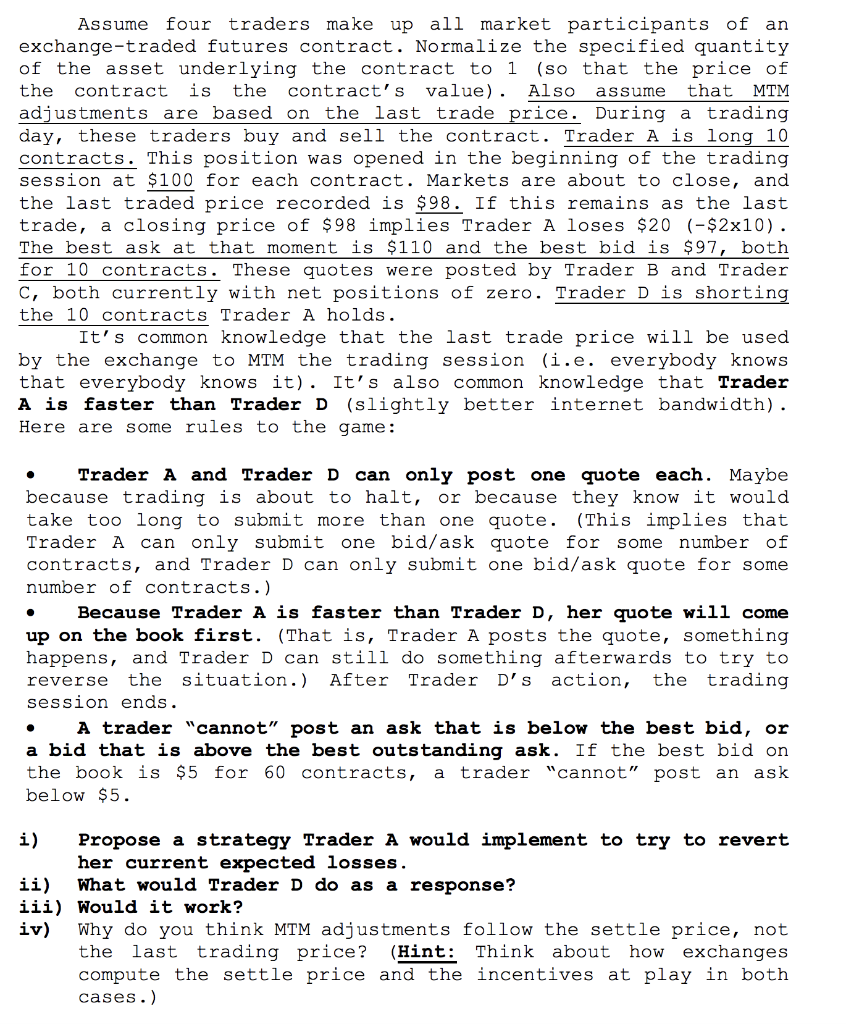

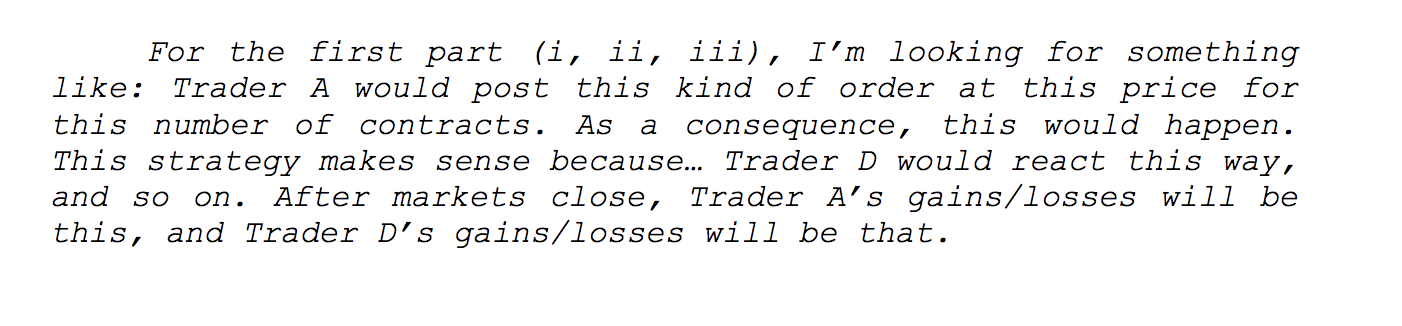

Assume four traders make up all market participants of an exchange-traded futures contract. Normalize the specified quantity of the asset underlying the contract to 1 (so that the price of the contract is the contract's value). Also assume that MTM adjustments are based on the last trade price. During a trading day, these traders buy and sell the contract. Trader A is long 10 contracts. This position was opened in the beginning of the trading session at $100 for each contract. Markets are about to close, and the last traded price recorded is $98. If this remains as the last trade, a closing price of $98 implies Trader A loses $20 (-$2x10). The best ask at that moment is $110 and the best bid is $97, both for 10 contracts. These quotes were posted by Trader B and Trader c, both currently with net positions of zero. Trader Dis shorting the 10 contracts Trader A holds. It's common knowledge that the last trade price will be used by the exchange to MTM the trading session (i.e. everybody knows that everybody knows it). It's also common knowledge that Trader A is faster than Trader D (slightly better internet bandwidth). Here are some rules to the game: C Trader A and Trader D can only post one quote each. Maybe because trading is about to halt, or because they know it would take too long to submit more than one quote. (This implies that Trader A can only submit one bid/ask quote for some number of contracts, and Trader D can only submit one bid/ask quote for some number of contracts.) Because Trader A is faster than Trader D, her quote will come up on the book first. (That is, Trader A posts the quote, something happens, and Trader D can still do something afterwards to try to reverse the situation.) After Trader D's action, the trading session ends. A trader "cannot" post an ask that is below the best bid, or a bid that is above the best outstanding ask. If the best bid on the book is $5 for 60 contracts, trader "cannot" post an ask below $5. i) Propose a strategy Trader A would implement to try to revert her current expected losses. ii) What would Trader D do as a response? iii) Would it work? iv) Why do you think MTM adjustments follow the settle price, not the last trading price? (Hint: Think about how exchanges compute the settle price and the incentives at play in both cases.) a For the first part (i, ii, iii), I'm looking for something like: Trader A would post this kind of order at this price for this number of contracts. As consequence, this would happen. This strategy makes sense because... Trader D would react this way, and so After markets close, Trader A's gains/losses will be this, and Trader D's gains/losses will be that. on. Assume four traders make up all market participants of an exchange-traded futures contract. Normalize the specified quantity of the asset underlying the contract to 1 (so that the price of the contract is the contract's value). Also assume that MTM adjustments are based on the last trade price. During a trading day, these traders buy and sell the contract. Trader A is long 10 contracts. This position was opened in the beginning of the trading session at $100 for each contract. Markets are about to close, and the last traded price recorded is $98. If this remains as the last trade, a closing price of $98 implies Trader A loses $20 (-$2x10). The best ask at that moment is $110 and the best bid is $97, both for 10 contracts. These quotes were posted by Trader B and Trader c, both currently with net positions of zero. Trader Dis shorting the 10 contracts Trader A holds. It's common knowledge that the last trade price will be used by the exchange to MTM the trading session (i.e. everybody knows that everybody knows it). It's also common knowledge that Trader A is faster than Trader D (slightly better internet bandwidth). Here are some rules to the game: C Trader A and Trader D can only post one quote each. Maybe because trading is about to halt, or because they know it would take too long to submit more than one quote. (This implies that Trader A can only submit one bid/ask quote for some number of contracts, and Trader D can only submit one bid/ask quote for some number of contracts.) Because Trader A is faster than Trader D, her quote will come up on the book first. (That is, Trader A posts the quote, something happens, and Trader D can still do something afterwards to try to reverse the situation.) After Trader D's action, the trading session ends. A trader "cannot" post an ask that is below the best bid, or a bid that is above the best outstanding ask. If the best bid on the book is $5 for 60 contracts, trader "cannot" post an ask below $5. i) Propose a strategy Trader A would implement to try to revert her current expected losses. ii) What would Trader D do as a response? iii) Would it work? iv) Why do you think MTM adjustments follow the settle price, not the last trading price? (Hint: Think about how exchanges compute the settle price and the incentives at play in both cases.) a For the first part (i, ii, iii), I'm looking for something like: Trader A would post this kind of order at this price for this number of contracts. As consequence, this would happen. This strategy makes sense because... Trader D would react this way, and so After markets close, Trader A's gains/losses will be this, and Trader D's gains/losses will be that. on