Answered step by step

Verified Expert Solution

Question

1 Approved Answer

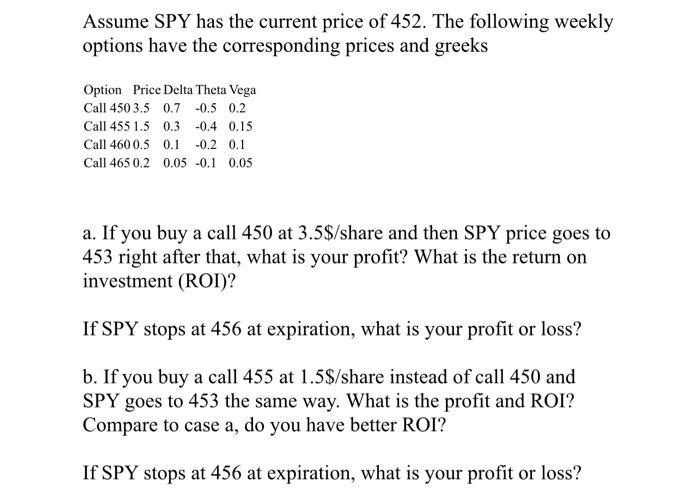

Assume SPY has the current price of 452. The following weekly options have the corresponding prices and greeks Option Price Delta Theta Vega Call 450

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Alexander Hamilton On Finance Credit And Debt

Authors: Richard Sylla

1st Edition

0231174012, 978-0231184571