Answered step by step

Verified Expert Solution

Question

1 Approved Answer

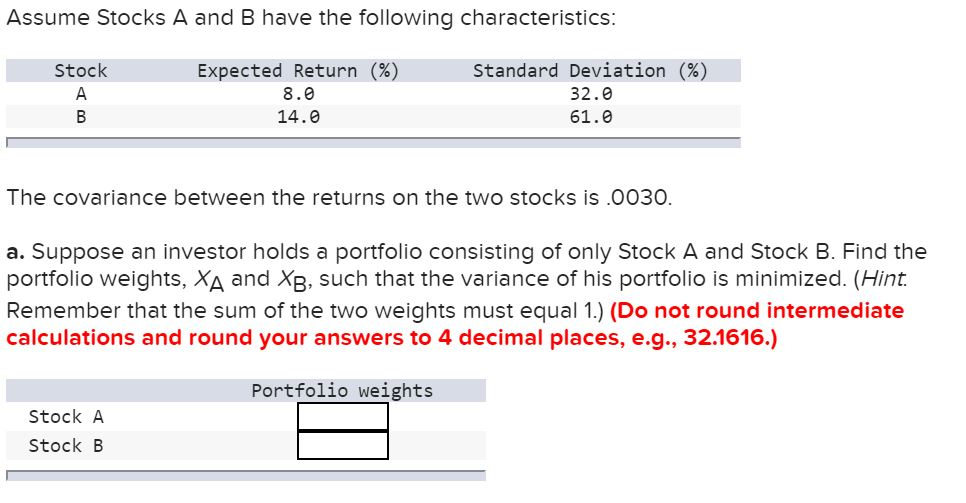

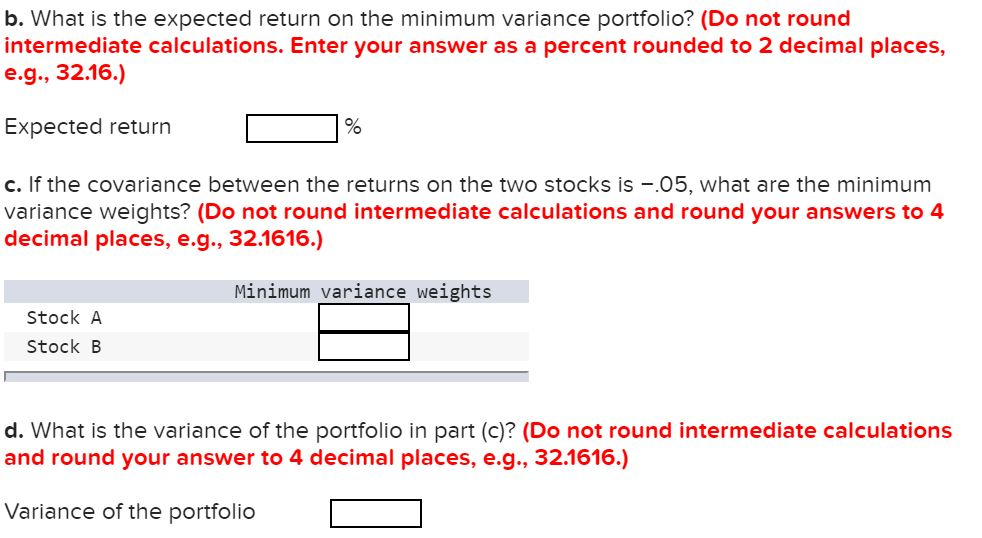

Assume Stocks A and B have the following characteristics: Stock B Expected Return (%) 8.0 14.0 Standard Deviation (%) 32.0 61.0 The covariance between the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey Rosen, Ted Gayer

10th edition

9781259716874, 78021685, 1259716872, 978-0078021688