Answered step by step

Verified Expert Solution

Question

1 Approved Answer

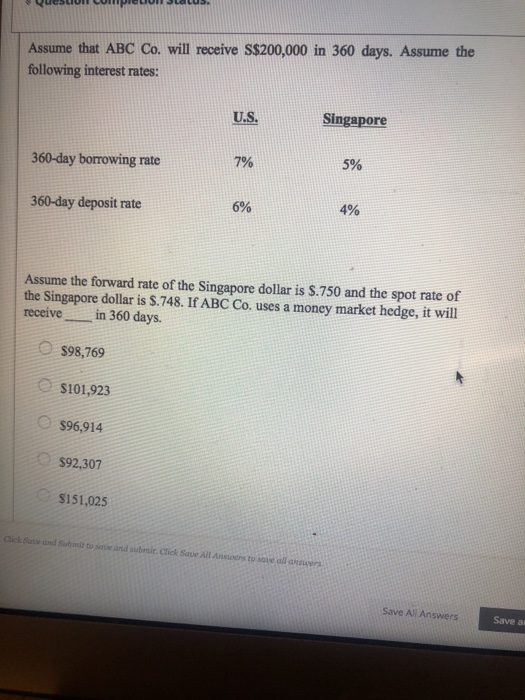

Assume that ABC Co. will receive S$200,000 in 360 days. Assume the following interest rates: U.S. Singapore 360-day borrowing rate 5% 360-day deposit rate 6%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Applications and Theory

Authors: Marcia Cornett, Troy Adair

3rd edition

1259252221, 007786168X, 9781259252228, 978-0077861681