Answered step by step

Verified Expert Solution

Question

1 Approved Answer

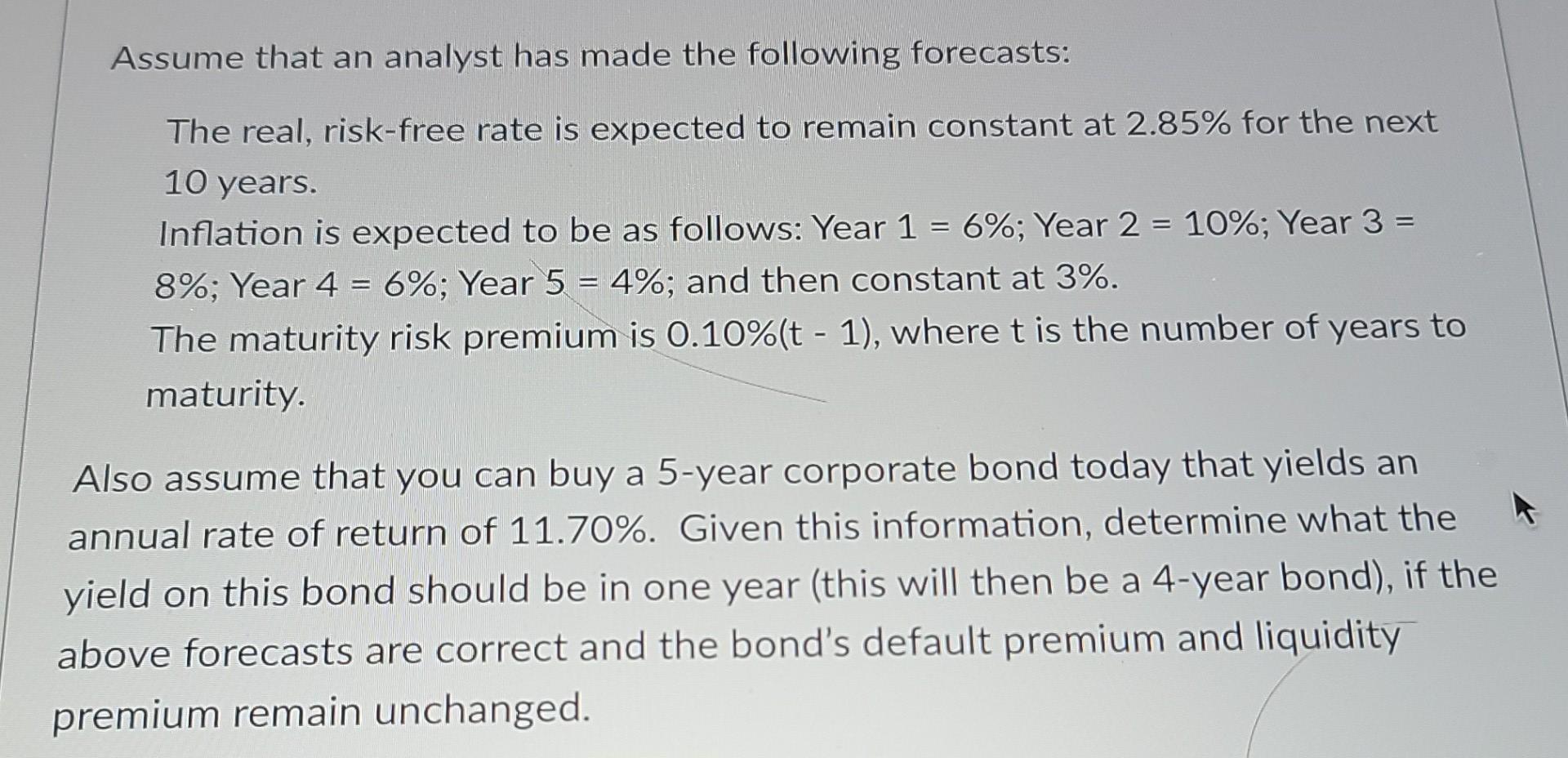

Assume that an analyst has made the following forecasts: The real, risk-free rate is expected to remain constant at 2.85% for the next 10

Assume that an analyst has made the following forecasts: The real, risk-free rate is expected to remain constant at 2.85% for the next 10 years. Inflation is expected to be as follows: Year 1 = 6%; Year 2 = 10%; Year 3 = 8%; Year 4 = 6%; Year 5 = 4%; and then constant at 3%. The maturity risk premium is 0.10% (t-1), where t is the number of years to maturity. Also assume that you can buy a 5-year corporate bond today that yields an annual rate of return of 11.70%. Given this information, determine what the yield on this bond should be in one year (this will then be a 4-year bond), if the above forecasts are correct and the bond's default premium and liquidity premium remain unchanged.

Step by Step Solution

★★★★★

3.47 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Yield on 4year corporate bond 1230 Working Note Rate of return ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Gordon Ro

7th Canadian Edition

007090653X, 978-0070906532, 978-0071339575