Question

Assume that in a two period model the current stock price is $25/share. The gross rate of return on the stock over each period is

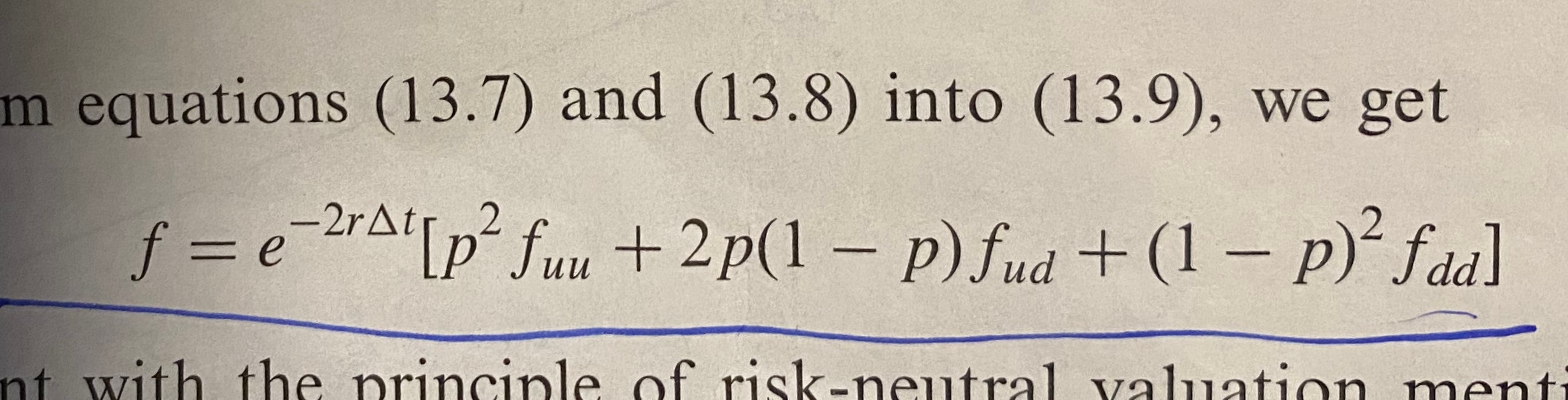

Assume that in a two period model the current stock price is $25/share. The gross rate of return on the stock over each period is either +40% or -20% while the single period simple rate of interest is 10%. Can you price a European put option on the stock with a strike of $30/share that expires at the end of the second period? Would you be able to price an American put with the same characteristics as the one above? Does it ever make sense to exercise the put at the end of the first period?

Please use the below formula to solve for P for both European and American Put

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Marketing For Small B2b Businesses

Authors: Andrew Schulkind

1st Edition

1484287436, 978-1484287439