Answered step by step

Verified Expert Solution

Question

1 Approved Answer

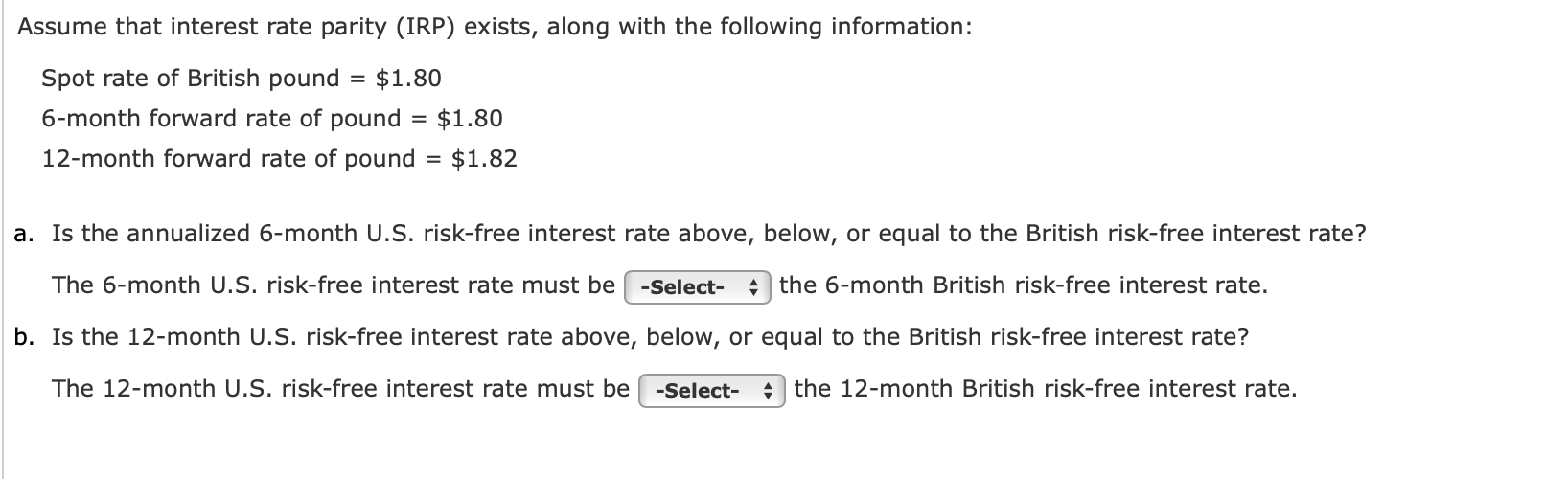

Assume that interest rate parity ( IRP ) exists, along with the following information: Spot rate of British pound = $ 1 . 8 0

Assume that interest rate parity IRP exists, along with the following information:

Spot rate of British pound $

month forward rate of pound $

month forward rate of pound $

a Is the annualized month US riskfree interest rate above, below, or equal to the British riskfree interest rate?

The month US riskfree interest rate must be

the month British riskfree interest rate.

b Is the month US riskfree interest rate above, below, or equal to the British riskfree interest rate?

The month US riskfree interest rate must be

the month British riskfree interest rate.

boxes show, above, below, equal to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Preppers Financial Guide

Authors: Jim Cobb

1st Edition

1612434037, 978-1612434032