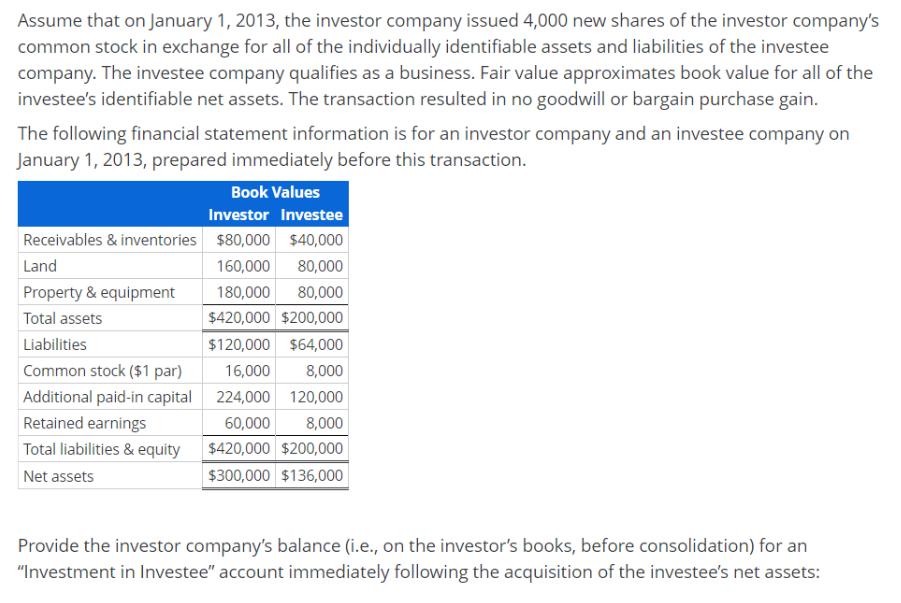

Assume that on January 1, 2013, the investor company issued 4,000 new shares of the investor company's common stock in exchange for all of

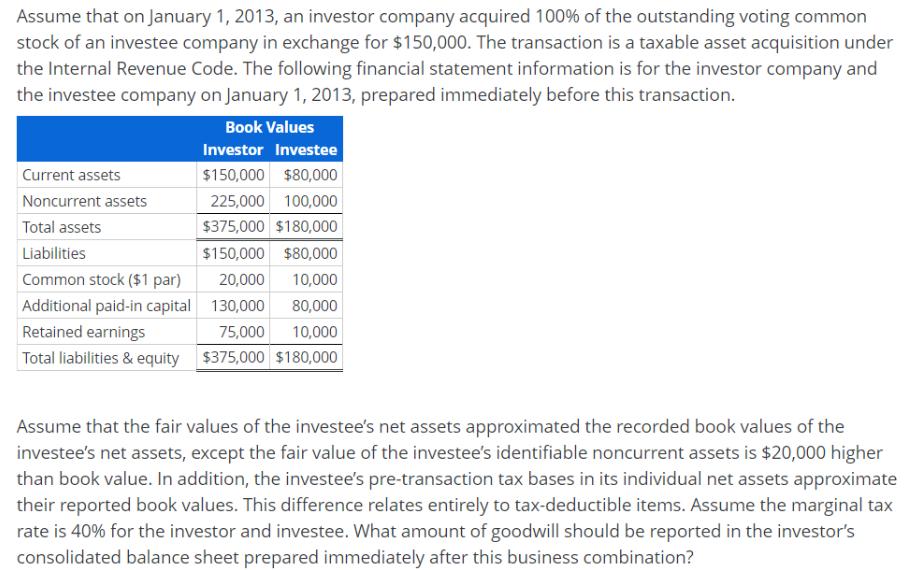

Assume that on January 1, 2013, the investor company issued 4,000 new shares of the investor company's common stock in exchange for all of the individually identifiable assets and liabilities of the investee company. The investee company qualifies as a business. Fair value approximates book value for all of the investee's identifiable net assets. The transaction resulted in no goodwill or bargain purchase gain. The following financial statement information is for an investor company and an investee company on January 1, 2013, prepared immediately before this transaction. Book Values Investor investee Receivables & inventories $80,000 $40,000 160,000 80,000 180,000 80,000 $420,000 $200,000 $120,000 $64,000 16,000 8,000 224,000 120,000 60,000 8,000 $420,000 $200,000 $300,000 $136,000 Land Property & equipment Total assets Liabilities Common stock ($1 par) Additional paid-in capital Retained earnings Total liabilities & equity Net assets Provide the investor company's balance (i.e., on the investor's books, before consolidation) for an "Investment in Investee" account immediately following the acquisition of the investee's net assets: Assume that on January 1, 2013, an investor company acquired 100% of the outstanding voting common stock of an investee company in exchange for $150,000. The transaction is a taxable asset acquisition under the Internal Revenue Code. The following financial statement information is for the investor company and the investee company on January 1, 2013, prepared immediately before this transaction. Book Values Investor Investee $150,000 $80,000 Current assets Noncurrent assets 225,000 100,000 Total assets $375,000 $180,000 Liabilities $150,000 $80,000 Common stock ($1 par) 20,000 10,000 Additional paid-in capital 130,000 80,000 Retained earnings 75,000 10,000 Total liabilities & equity $375,000 $180,000 Assume that the fair values of the investee's net assets approximated the recorded book values of the investee's net assets, except the fair value of the investee's identifiable noncurrent assets is $20,000 higher than book value. In addition, the investee's pre-transaction tax bases in its individual net assets approximate their reported book values. This difference relates entirely to tax-deductible items. Assume the marginal tax rate is 40% for the investor and investee. What amount of goodwill should be reported in the investor's consolidated balance sheet prepared immediately after this business combination?

Step by Step Solution

3.41 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

To solve this problem we need to combine the financial information given for both investor and investee companies and make the required adjustments after the business combination However it seems you ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Flawrence Revsine, Daniel Collins, Bruce, Mittelstaedt, Leon

6th edition

9780077632182, 78025672, 77632184, 978-0078025679