Answered step by step

Verified Expert Solution

Question

1 Approved Answer

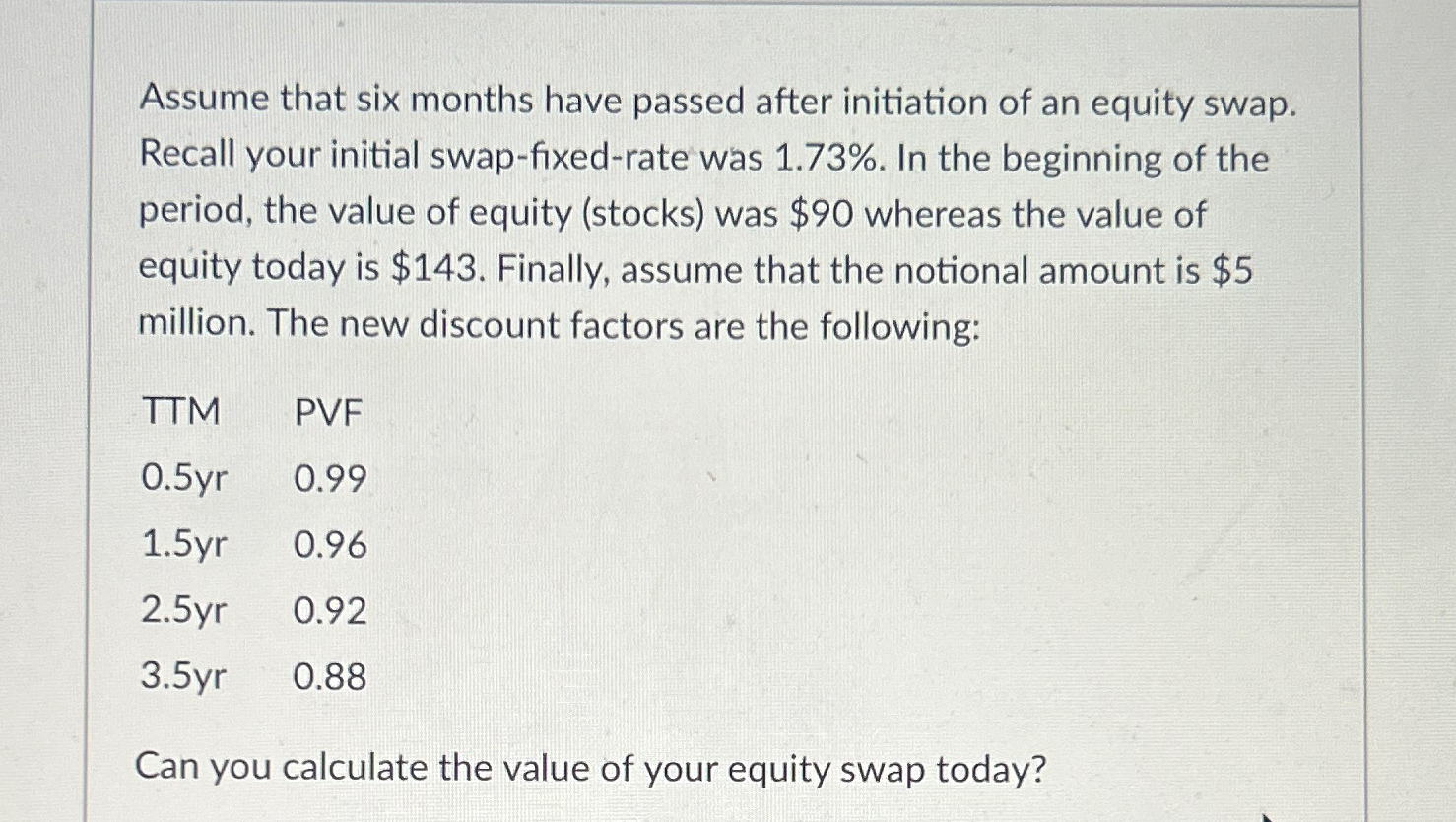

Assume that six months have passed after initiation of an equity swap. Recall your initial swap - fixed - rate was 1 . 7 3

Assume that six months have passed after initiation of an equity swap. Recall your initial swapfixedrate was In the beginning of the period, the value of equity stocks was $ whereas the value of equity today is $ Finally, assume that the notional amount is $ million. The new discount factors are the following:

tableTTMPVF

Can you calculate the value of your equity swap today?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance With Monte Carlo

Authors: Ronald W. Shonkwiler

2013th Edition

146148510X, 978-1461485100