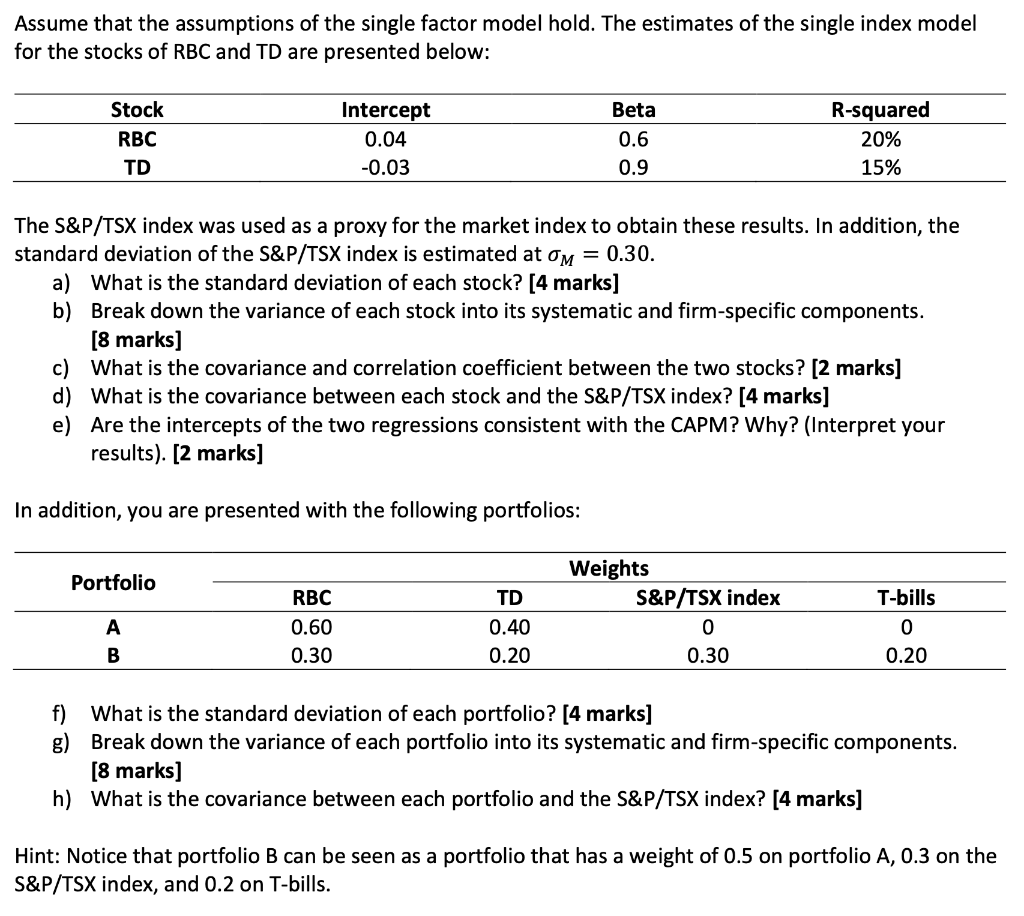

Assume that the assumptions of the single factor model hold. The estimates of the single index model for the stocks of RBC and TD are presented below: Stock RBC TD Intercept 0.04 -0.03 Beta 0.6 R-squared 20% 15% 0.9 The S&P/TSX index was used as a proxy for the market index to obtain these results. In addition, the standard deviation of the S&P/TSX index is estimated at om = 0.30. a) What is the standard deviation of each stock? (4 marks] b) Break down the variance of each stock into its systematic and firm-specific components. [8 marks] c) What is the covariance and correlation coefficient between the two stocks? [2 marks] d) What is the covariance between each stock and the S&P/TSX index? (4 marks] e) Are the intercepts of the two regressions consistent with the CAPM? Why? (Interpret your results). [2 marks] In addition, you are presented with the following portfolios: Portfolio Weights S&P/TSX index T-bills RBC 0.60 0.30 TD 0.40 0.20 O 0.30 0.20 f) What is the standard deviation of each portfolio? (4 marks] g) Break down the variance of each portfolio into its systematic and firm-specific components. [8 marks] h) What is the covariance between each portfolio and the S&P/TSX index? (4 marks) Hint: Notice that portfolio B can be seen as a portfolio that has a weight of 0.5 on portfolio A, 0.3 on the S&P/TSX index, and 0.2 on T-bills. Assume that the assumptions of the single factor model hold. The estimates of the single index model for the stocks of RBC and TD are presented below: Stock RBC TD Intercept 0.04 -0.03 Beta 0.6 R-squared 20% 15% 0.9 The S&P/TSX index was used as a proxy for the market index to obtain these results. In addition, the standard deviation of the S&P/TSX index is estimated at om = 0.30. a) What is the standard deviation of each stock? (4 marks] b) Break down the variance of each stock into its systematic and firm-specific components. [8 marks] c) What is the covariance and correlation coefficient between the two stocks? [2 marks] d) What is the covariance between each stock and the S&P/TSX index? (4 marks] e) Are the intercepts of the two regressions consistent with the CAPM? Why? (Interpret your results). [2 marks] In addition, you are presented with the following portfolios: Portfolio Weights S&P/TSX index T-bills RBC 0.60 0.30 TD 0.40 0.20 O 0.30 0.20 f) What is the standard deviation of each portfolio? (4 marks] g) Break down the variance of each portfolio into its systematic and firm-specific components. [8 marks] h) What is the covariance between each portfolio and the S&P/TSX index? (4 marks) Hint: Notice that portfolio B can be seen as a portfolio that has a weight of 0.5 on portfolio A, 0.3 on the S&P/TSX index, and 0.2 on T-bills