Answered step by step

Verified Expert Solution

Question

1 Approved Answer

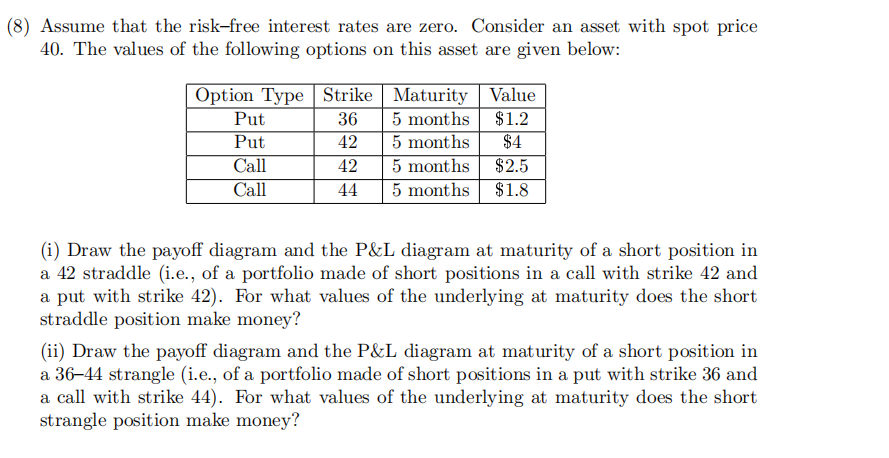

Assume that the risk-free interest rates are zero. Consider an asset with spot price 40. The values of the following options on this asset are

Assume that the risk-free interest rates are zero. Consider an asset with spot price 40. The values of the following options on this asset are given below: (i) Draw the payoff diagram and the P\&L diagram at maturity of a short position in a 42 straddle (i.e., of a portfolio made of short positions in a call with strike 42 and a put with strike 42). For what values of the underlying at maturity does the short straddle position make money? (ii) Draw the payoff diagram and the P\&L diagram at maturity of a short position in a 36-44 strangle (i.e., of a portfolio made of short positions in a put with strike 36 and a call with strike 44). For what values of the underlying at maturity does the short strangle position make money

Assume that the risk-free interest rates are zero. Consider an asset with spot price 40. The values of the following options on this asset are given below: (i) Draw the payoff diagram and the P\&L diagram at maturity of a short position in a 42 straddle (i.e., of a portfolio made of short positions in a call with strike 42 and a put with strike 42). For what values of the underlying at maturity does the short straddle position make money? (ii) Draw the payoff diagram and the P\&L diagram at maturity of a short position in a 36-44 strangle (i.e., of a portfolio made of short positions in a put with strike 36 and a call with strike 44). For what values of the underlying at maturity does the short strangle position make money Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Numerical Techniques In Finance

Authors: Simon Benninga

1st Edition

0262022869, 978-0262022866