Answered step by step

Verified Expert Solution

Question

1 Approved Answer

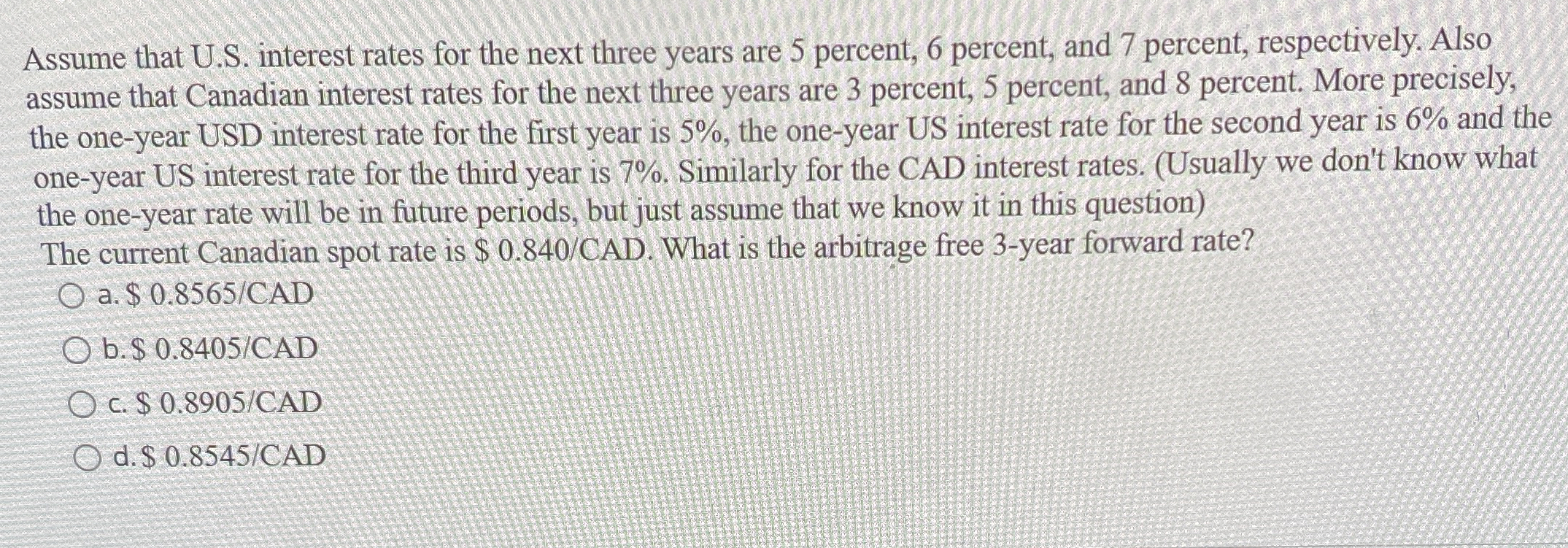

Assume that U . S . interest rates for the next three years are 5 percent, 6 percent, and 7 percent, respectively. Also assume that

Assume that US interest rates for the next three years are percent, percent, and percent, respectively. Also

assume that Canadian interest rates for the next three years are percent, percent, and percent. More precisely,

the oneyear USD interest rate for the first year is the oneyear US interest rate for the second year is and the

oneyear US interest rate for the third year is Similarly for the CAD interest rates. Usually we don't know what

the oneyear rate will be in future periods, but just assume that we know it in this question

The current Canadian spot rate is $ What is the arbitrage free year forward rate?

a $

b $

c $

d $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoinvest Or Not Answers To Crucial Questions

Authors: Mr Panayotis Vasileios Sofianopoulos

1st Edition

1713251752, 978-1713251750