Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Assume the following data for a stock, and 2-factor APT model: Risk-free rate = 3.06 % Factor-1 beta = 1.16 Factor-2 beta=0 Factor-1 risk-premium

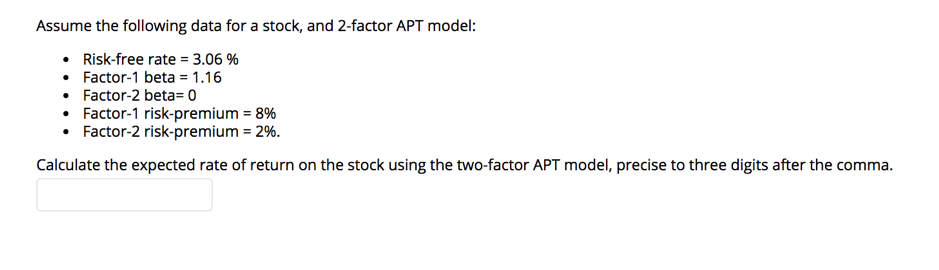

Assume the following data for a stock, and 2-factor APT model: Risk-free rate = 3.06 % Factor-1 beta = 1.16 Factor-2 beta=0 Factor-1 risk-premium = 8% Factor-2 risk-premium = 2%. Calculate the expected rate of return on the stock using the two-factor APT model, precise to three digits after the comma.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111