Answered step by step

Verified Expert Solution

Question

1 Approved Answer

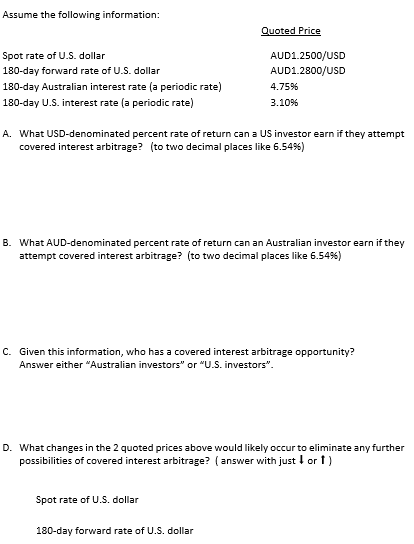

Assume the following information: Quoted Price Spot rate of U . S . dollar AUD 1 . 2 5 0 0 / USD 1 8

Assume the following information:

Quoted Price

Spot rate of US dollar

AUDUSD

day forward rate of US dollar

AUDUSD

day Australian interest rate a periodic rate

day US interest rate a periodic rate

A What USDdenominated percent rate of return can a US investor earn if they attempt

covered interest arbitrage? to two decimal places like

B What AUDdenominated percent rate of return can an Australian investor earn if they

attempt covered interest arbitrage? to two decimal places like

C Given this information, who has a covered interest arbitrage opportunity?

Answer either "Australian investors" or US investors".

D What changes in the quoted prices above would likely occur to eliminate any further

possibilities of covered interest arbitrage? answer with just darr or

Spot rate of US dollar

day forward rate of US dollar

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Water Finance

Authors: Michael Curley

1st Edition

1498734170, 978-1498734172