Question

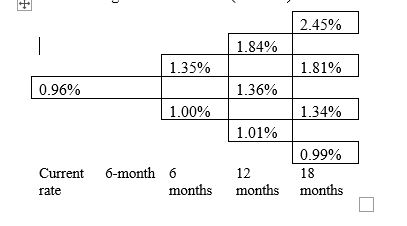

Assume the following interest rate tree a)Calculate value of the (option-free) bond using binomial model (note that interest rates in the tree above are presented

Assume the following interest rate tree

a)Calculate value of the (option-free) bond using binomial model (note that interest rates in the tree above are presented in the annualised form).

b)Assume the bond is callable on 30 Sep 2017 and 30 Mar 2018 at $100.50, calculate the value of the bond.

c) Calculate value of the call option and comment on who bears the cost of the call option.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

DeFi And The Future Of Finance

Authors: Campbell R. Harvey, Ashwin Ramachandran, Joey Santoro, Vitalik Buterin, Fred Ehrsam

1st Edition

1119836018, 978-1119836018