Question

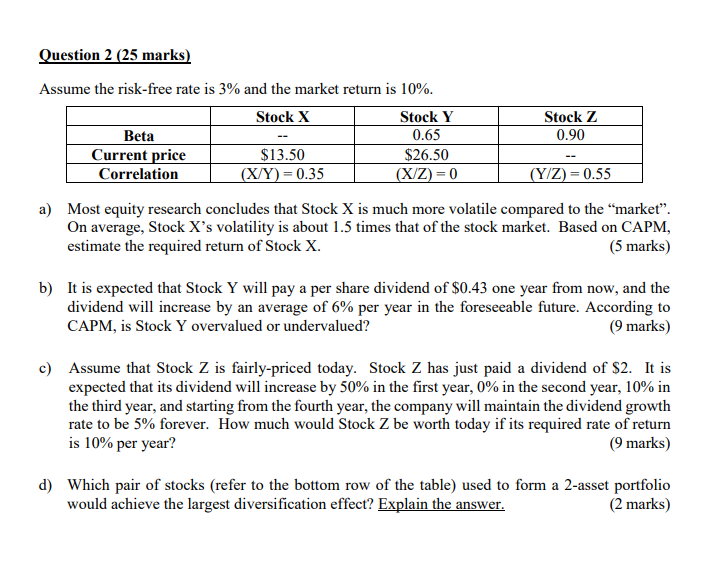

Assume the risk-free rate is 3% and the market return is 10%. Stock X Stock Y Stock Z Beta -- 0.65 0.90 Current price $13.50

Assume the risk-free rate is 3% and the market return is 10%. Stock X Stock Y Stock Z Beta -- 0.65 0.90 Current price $13.50 $26.50 -- Correlation (X/Y) = 0.35 (X/Z) = 0 (Y/Z) = 0.55 a) Most equity research concludes that Stock X is much more volatile compared to the market. On average, Stock Xs volatility is about 1.5 times that of the stock market. Based on CAPM, estimate the required return of Stock X.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation Measuring and managing the values of companies

Authors: Mckinsey, Tim Koller, Marc Goedhart, David Wessel

5th edition

978-0470424650, 9780470889930, 470424656, 470889934, 978-047042470