Question

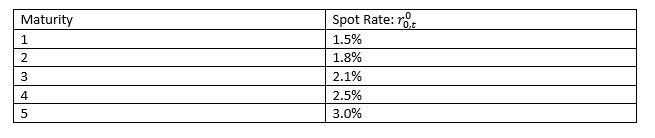

Assume the spot curve is the same as in problem 5 above (reproduced below). Answer the following questions regarding a swap contract. a. Calculate the

Assume the spot curve is the same as in problem 5 above (reproduced below). Answer the following questions regarding a swap contract.

a. Calculate the swap rate for all maturities assuming the floating payer pays the 1 year spot rate for each year. (ie. What is the Swap rate that would apply for a 2 year Swap? What is the rate for a 3 year Swap? Etc.)

Use the 3 year swap for the next set of questions.

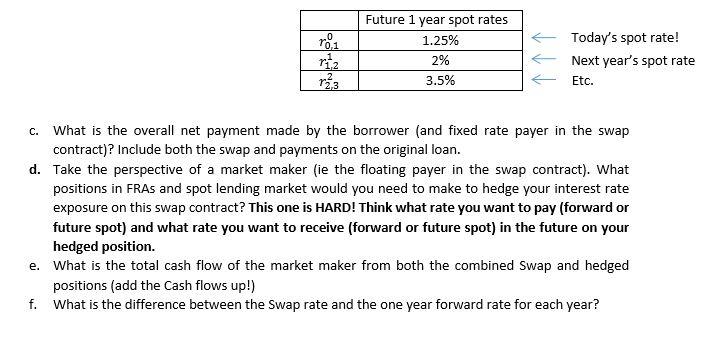

b. A borrower of floating rate debt has a loan amount of $100M and pays the 1 year T-Bill rate on the loan. The borrower wants to convert this floating rate debt to fixed rate debt with the 3 year swap contract. What is the actual swap payment that will change hands in each year for future one year spot rates given below? Take the perspective of the floating rate borrower who wants to pay a fixed rate.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mortgage Ripoffs And Money Savers

Authors: Carolyn Warren

1st Edition

0470097833, 978-0470097830