Answered step by step

Verified Expert Solution

Question

1 Approved Answer

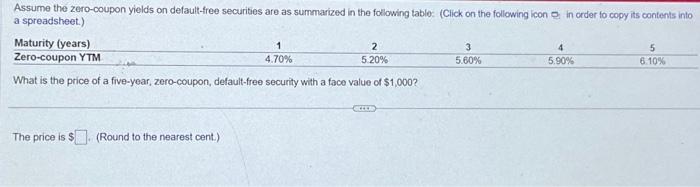

Assume the zero-coupon yields on default-free securities are as summarized in the following table: (Click on the following icon in order to copy its contents

Assume the zero-coupon yields on default-free securities are as summarized in the following table: (Click on the following icon in order to copy its contents into a spreadsheet.) Maturity (years) 1 4.70% 2 5.20% Zero-coupon YTM What is the price of a five-year, zero-coupon, default-free security with a face value of $1,000? The price is $. (Round to the nearest cent.) 3 5.60% 4 5.90% 5 6.10%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The FinTech Book The Financial Technology Handbook For Investors Entrepreneurs And Visionaries

Authors: Susanne Chishti, Janos Barberis

1st Edition

111921887X, 9781119218876