Answered step by step

Verified Expert Solution

Question

1 Approved Answer

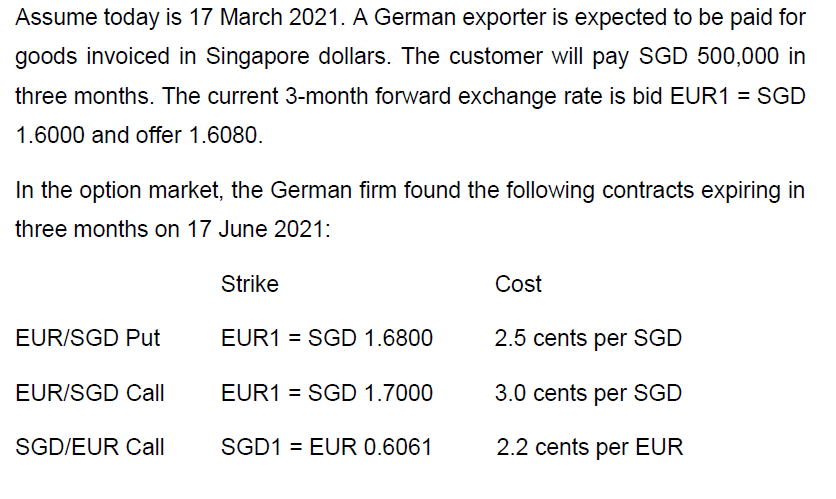

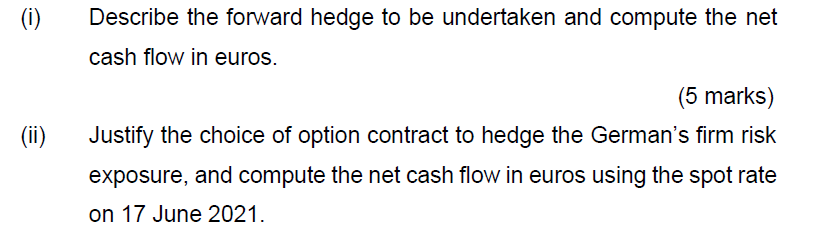

Assume today is 17 March 2021. A German exporter is expected to be paid for goods invoiced in Singapore dollars. The customer will pay SGD

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Negative Interest Rates And Financial Stability Lessons In Systemic Risk

Authors: Karol Rogowicz, Malgorzata Iwanicz Drozdowska

1st Edition

1032319496, 1000787826, 9781032319490, 9781000787825