Answered step by step

Verified Expert Solution

Question

1 Approved Answer

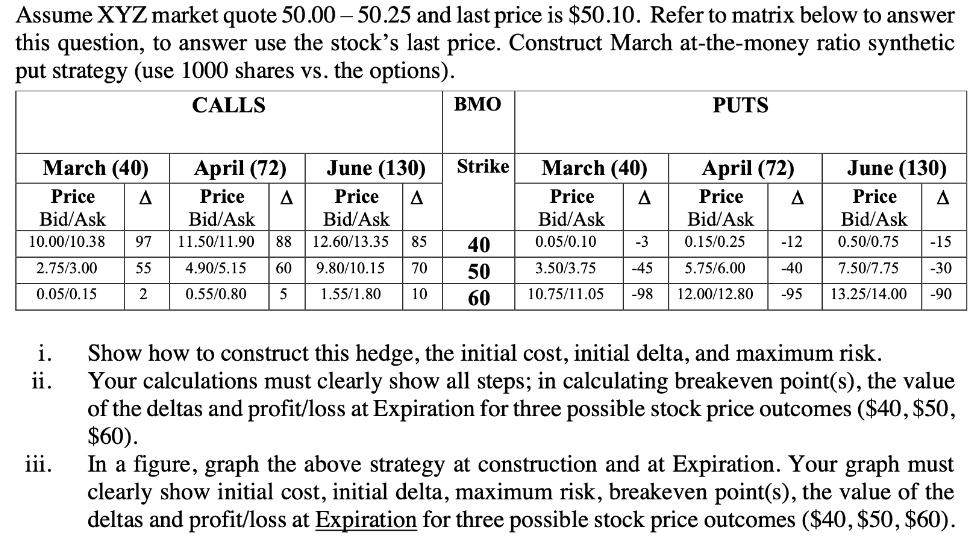

Assume XYZ market quote 50.00 50.25 and last price is $50.10. Refer to matrix below to answer this question, to answer use the stock's

Assume XYZ market quote 50.00 50.25 and last price is $50.10. Refer to matrix below to answer this question, to answer use the stock's last price. Construct March at-the-money ratio synthetic put strategy (use 1000 shares vs. the options). CALLS March (40) June (130) A Price A Price Bid/Ask Bid/Ask Bid/Ask 10.00/10.38 97 11.50/11.90 88 12.60/13.35 4.90/5.15 60 9.80/10.15 0.55/0.80 5 1.55/1.80 55 2 2.75/3.00 0.05/0.15 i. ii. iii. April (72) Price A BMO Strike 85 40 50 70 10 60 PUTS April (72) March (40) Price June (130) Price A Price A Bid/Ask Bid/Ask 0.50/0.75 -15 Bid/Ask 0.05/0.10 -3 0.15/0.25 -12 3.50/3.75 -45 5.75/6.00 -40 7.50/7.75 -30 10.75/11.05 -98 12.00/12.80 -95 13.25/14.00 -90 A Show how to construct this hedge, the initial cost, initial delta, and maximum risk. Your calculations must clearly show all steps; in calculating breakeven point(s), the value of the deltas and profit/loss at Expiration for three possible stock price outcomes ($40, $50, $60). In a figure, graph the above strategy construction and at Expiration. Your graph must clearly show initial cost, initial delta, maximum risk, breakeven point(s), the value of the deltas and profit/loss at Expiration for three possible stock price outcomes ($40, $50, $60).

Step by Step Solution

★★★★★

3.50 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

15th edition

1337671002, 978-1337395250