Answered step by step

Verified Expert Solution

Question

1 Approved Answer

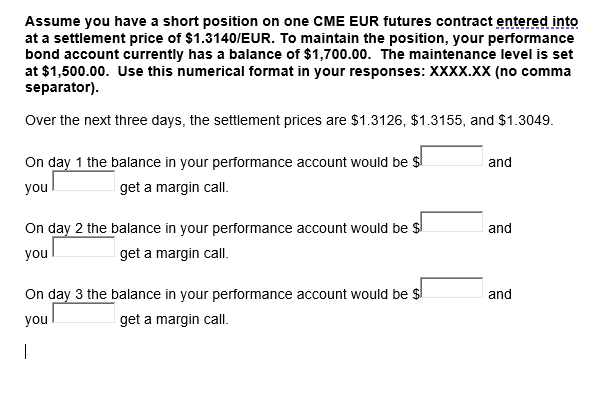

Assume you have a short position on one CME EUR futures contract entered into at a settlement price of $1.3140/EUR. To maintain the position, your

Assume you have a short position on one CME EUR futures contract entered into at a settlement price of $1.3140/EUR. To maintain the position, your performance bond account currently has a balance of $1,700.00. The maintenance level is set at $1,500.00. Use this numerical format in your responses: XXXX.XX (no comma separator). Over the next three days, the settlement prices are $1.3126,$1.3155, and $1.3049. On day 1 the balance in your performance account would be $ and you get a margin call. On day 2 the balance in your performance account would be $ and you get a margin call. On day 3 the balance in your performance account would be $ and you get a margin call

Assume you have a short position on one CME EUR futures contract entered into at a settlement price of $1.3140/EUR. To maintain the position, your performance bond account currently has a balance of $1,700.00. The maintenance level is set at $1,500.00. Use this numerical format in your responses: XXXX.XX (no comma separator). Over the next three days, the settlement prices are $1.3126,$1.3155, and $1.3049. On day 1 the balance in your performance account would be $ and you get a margin call. On day 2 the balance in your performance account would be $ and you get a margin call. On day 3 the balance in your performance account would be $ and you get a margin call Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

17th Edition

126001391X, 978-1260013917