Answered step by step

Verified Expert Solution

Question

1 Approved Answer

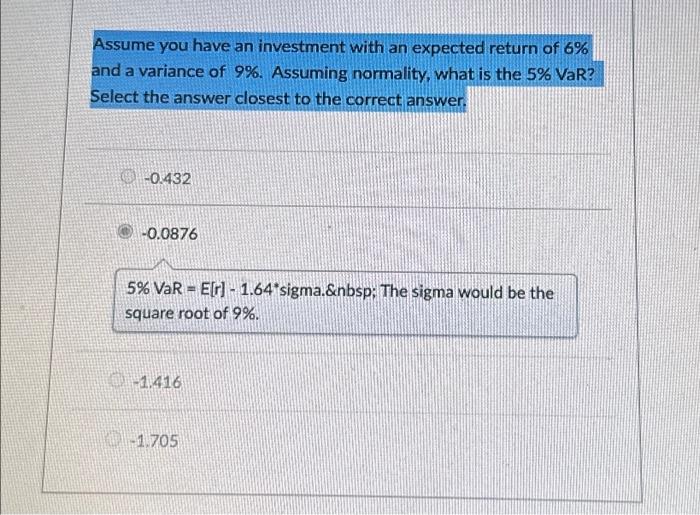

Assume you have an investment with an expected return of 6% and a variance of 9%. Assuming normality, what is the 5% VaR? Select the

Assume you have an investment with an expected return of 6% and a variance of 9%. Assuming normality, what is the 5% VaR? Select the answer closest to the correct answer. -0.432 -0.0876 5% VaR E[r] - 1.64 sigma. The sigma would be the square root of 9%. -1.416 -1.705

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Interest Rate Swaps And Their Derivatives A Practitioners Guide

Authors: Amir Sadr

1st Edition

0470443944, 978-0470443941