Answered step by step

Verified Expert Solution

Question

1 Approved Answer

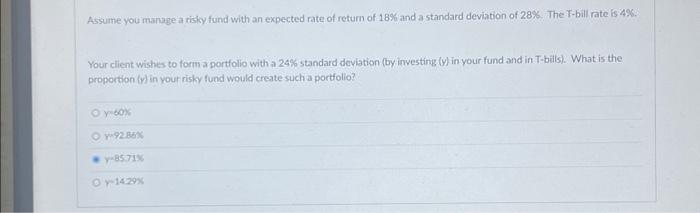

Assume you manage a risky fund with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 4%.

Assume you manage a risky fund with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 4%. Your client wishes to form a portfolio with a 24% standard deviation (by investing (y) in your fund and in T-bills).

What is the proportion (y) in your risky fund would create such a portfolio?

y=60% y=92.86% y=85.71% y=14.29%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Get Rich With Dividends

Authors: Marc Lichtenfeld

3rd Edition

1119985552, 978-1119985556