Answered step by step

Verified Expert Solution

Question

1 Approved Answer

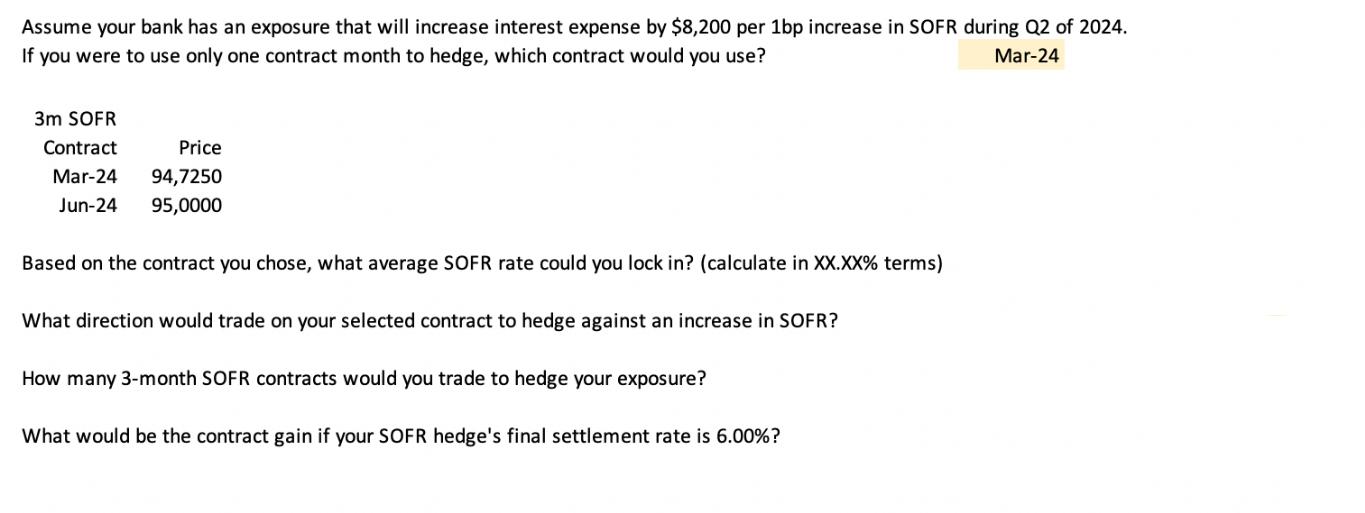

Assume your bank has an exposure that will increase interest expense by $8,200 per 1bp increase in SOFR during Q2 of 2024. If you

Assume your bank has an exposure that will increase interest expense by $8,200 per 1bp increase in SOFR during Q2 of 2024. If you were to use only one contract month to hedge, which contract would you use? Mar-24 3m SOFR Contract Price Mar-24 94,7250 Jun-24 95,0000 Based on the contract you chose, what average SOFR rate could you lock in? (calculate in XX.XX% terms) What direction would trade on your selected contract to hedge against an increase in SOFR? How many 3-month SOFR contracts would you trade to hedge your exposure? What would be the contract gain if your SOFR hedge's final settlement rate is 6.00%?

Step by Step Solution

★★★★★

3.51 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

1 Calculate the implied SOFR rate for both Mar24 and Jun24 contracts Mar24 contract Implied rate 100 ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

9th Edition

1337614689, 1337614688, 9781337668262, 978-1337614689