Answered step by step

Verified Expert Solution

Question

1 Approved Answer

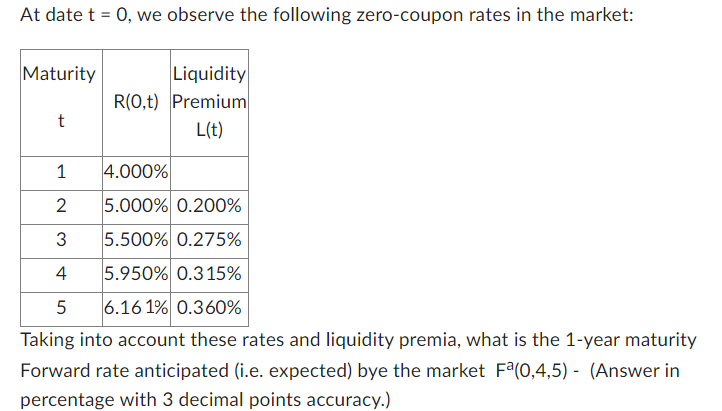

At date t = 0 , we observe the following zero - coupon rates in the market: Maturity t R ( 0 , t )

At date t we observe the following zerocoupon rates in the market:

Maturity t Rt Liquidity Premium Lt

Taking into account these rates and liquidity premia, what is the year maturity

Forward rate anticipated ie expected bye the market FaAt date we observe the following zerocoupon rates in the market:

Taking into account these rates and liquidity premia, what is the year maturity

Forward rate anticipated ie expected bye the market Answer in

percentage with decimal points accuracy.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Top Actuel Fiscalité 2022-2023

Authors: Daniel Freiss,Brigitte Monnet

1st Edition

2017182176,2017879282