Question

At the snapshot below, you can see results from the second pass (cross- sectional) regression, where the estimated CAPM-beta from the first pass (time series)

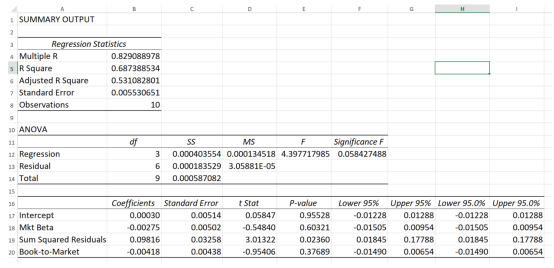

At the snapshot below, you can see results from the second pass (cross- sectional) regression, where the estimated CAPM-beta from the first pass (time series) together with book-to-market and idiosyncratic volatility are related to average stock return. Write down the regression equation that was estimated in Excel. Interpret the results and conclude (based on the results) whether CAPM holds.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Frederic S. Mishkin, Stanley G. Eakins

7th Edition

013213683X, 978-0132136839