Answered step by step

Verified Expert Solution

Question

1 Approved Answer

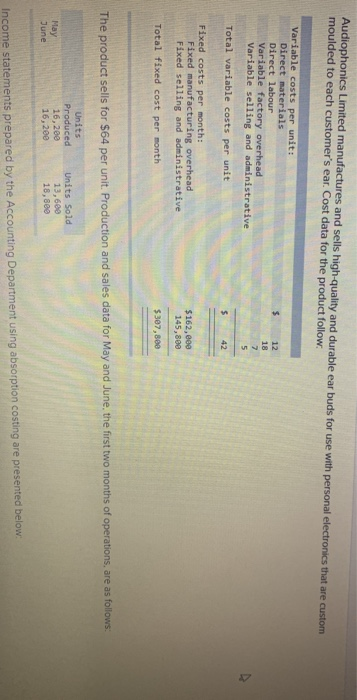

Audiophonics Limited manufactures and sells high-quality and durable ear buds for use with personal electronics that are custom moulded to each customer's ear. Cost data

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

GCP Auditing Methods And Experiences

Authors: Editio

1st Edition

3871932841, 978-3871932847