Question: AUDIT MANUAL EXCERPT: MATERIALITY GUIDELINES Overall Materiality and Tolerable Misstatement Overall Materiality This section provides general guidelines for determining overall materiality and tolerable misstatement for

AUDIT MANUAL EXCERPT: MATERIALITY GUIDELINES

Overall Materiality and Tolerable Misstatement

Overall Materiality

This section provides general guidelines for determining overall materiality and tolerable misstatement for audits performed by Willis & Adams. The application of these guidelines requires professional judgment and the facts and circumstances of each individual engagement must be considered.

Statement of Financial Accounting Concepts No. 2, Qualitative Characteristics of Accounting Information, defines materiality as follows:

Materiality is the magnitude of an omission or misstatement of accounting information that, in the light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the omission or misstatement.

The reasonable person, approach means that the magnitude and nature of financial statement misstatements or omissions will not have the same influence on all financial statement users. For example, a 7 percent misstatement with current assets may be more relevant for a creditor than a stockholder, while a 7 percent misstatement with net income before income taxes may be more relevant for a stockholder than a creditor.

While qualitative factors need to be considered, it is not practical to design audit procedures to detect all misstatement that potentially could be qualitatively material. Therefore, as a starting point, we typically compute a quantitative materiality determined as a percentage of the most relevant base (e.g., Income Before Taxes, Total Revenue, Total Assets). Relevant financial statement bases and presumptions on the effect of combined misstatements or omissions that would be considered immaterial and material are provided below:

Profit Oriented Entity:

- Income Before Income Taxes - combined misstatements or omissions less than 3 percent of Income Before Income Taxes are presumed to be immaterial and combined misstatements or omissions greater than 7 percent are presumed to be material. For publicly traded companies, materiality is typically set at 5 percent of income before income taxes.

If pretax income is stable, predictable, and representative[1] of the entitys size and complexity, it is typically the preferred base. However, if net income is not stable, predictable, representative, or if the entity is close to breaking even or experiencing a loss, then other bases may need to be considered. If the entity has volatile earnings, including negative or near zero earnings, it might be more appropriate to use the average of 3 to 5 years of pretax net income as the base (referred to as "normalized earnings").

Other possible bases to consider include:

- Total Revenue (less returns and discounts) combined misstatements or omissions less than 0.5 percent of Total Revenue are presumed to be immaterial, and combined misstatements or omissions greater than 3 percent are presumed to be material.

- Total Assets - combined misstatements or omissions less than 0.25 percent of Total Assets are presumed to be immaterial, and combined misstatements or omissions greater than 2 percent are presumed to be material. (Note: Total Assets may not be an appropriate base for service organizations or other organizations that have few operating assets.)

Not-for-Profit Entity

- Total Revenue (less returns and discounts) combined misstatements or omissions less than 0.5 percent of Total Revenue are presumed to be immaterial, and combined misstatements or omissions greater than 3 percent are presumed to be material.

- Total Assets combined misstatements or omissions less than .25 percent of Total Expenses are presumed to be immaterial, and combined misstatements or omissions greater than 2 percent are presumed to be material.

Mutual Fund Entity

- Net Asset Value combined misstatements or omissions less than 3 percent of Net Asset Value are presumed to be immaterial and combined misstatements or omissions greater than 5 percent are presumed to be material.

The specific value within the above ranges for a particular base is determined by considering the primary users as well as qualitative factors. For example, if the client is close to violating the minimum current ratio requirement for a loan agreement, a smaller overall materiality amount should be used. Conversely, if the client is substantially above the minimum current ratio requirement for a loan agreement, it would be reasonable to use a higher overall materiality amount.

Tolerable Misstatement

In addition to establishing overall materiality for the overall financial statements, materiality for individual financial statement accounts should be established. The materiality amount established for individual accounts is referred to as tolerable misstatement. Tolerable misstatement represents the amount an individual financial statement account can differ from its true amount without affecting the fair presentation of the financial statements taken as a whole.

Establishment of tolerable misstatement for individual accounts enables the auditor to design and execute an audit strategy for each audit cycle. It is an important input in determining the nature, timing and extent of audit procedures.

Tolerable misstatement should be established for all balance sheet accounts (except retained earnings because it is the residual account). Tolerable misstatement need not be allocated to income statement accounts because many misstatements affect both income statement and balance sheet accounts and misstatements affecting only the income statement are normally less relevant to users.

The objective in setting tolerable misstatement for individual balance sheet accounts is to provide reasonable assurance that the financial statements taken as a whole are fairly presented in all material respects at the lowest cost. Factors to consider when setting tolerable misstatement for accounts include:

- The tolerable misstatement to be allocated to an account is 50 to 75 percent of overall materiality.

- Tolerable misstatement should not exceed 25% of the account balance.

- Tolerable misstatement should not exceed an amount that would influence the decision of reasonable users.

- Tolerable misstatement normally will be higher for accounts with a higher expectation of misstatement.[2]

- Willis & Adams limits the total amount of tolerable misstatement allocated to the balance sheet accounts to about ten times materiality in order to limit aggregation risk.

[1] By stable, predictable, and representative we mean that pretax income does not wildly or dramatically change from profit to loss from year to year. If investors still view pretax income as a reliable measure of the entitys performance then pretax income should be used to determine materiality.

[2] This assumes the expected misstatements are not due to fraud. If we have an increased fraud risk, we would utilize fraud-related procedures, see fraud policy guidelines. The reason we will normally utilize a higher tolerable misstatement for accounts with higher expectation of misstatement is related to the costliness of auditing such accounts. For example, accounts like accounts receivable, inventory, or accounts payable will often have some degree of misstatement in them and they typically are large balances. Tolerable misstatement is basically a reasonable margin for error. If we set tolerable misstatement too low, sample sizes can increase dramatically. However, as noted in the policy, in no case will we allocate more tolerable misstatement to an account than a misstatement amount that would influence the decisions of reasonable users.

Data:

(balance sheet)

(balance sheet)

(income statement)

(income statement)

(cash flows)

(cash flows)

(shareholders investment)

(shareholders investment)

(5 yr financial statement)

(5 yr financial statement)

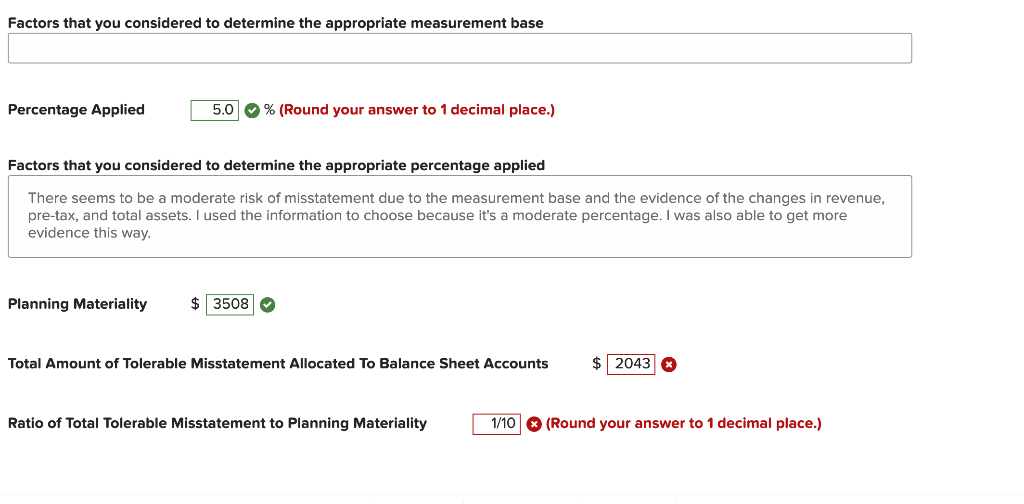

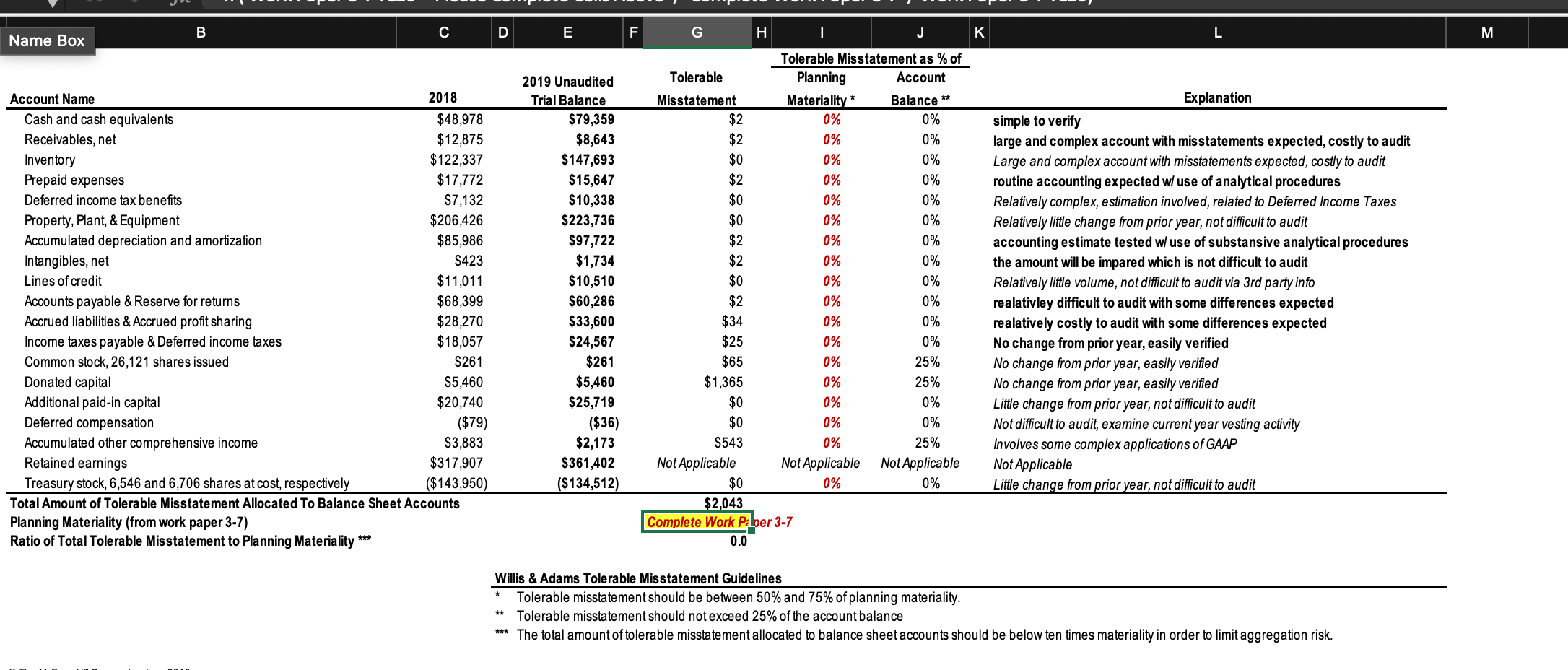

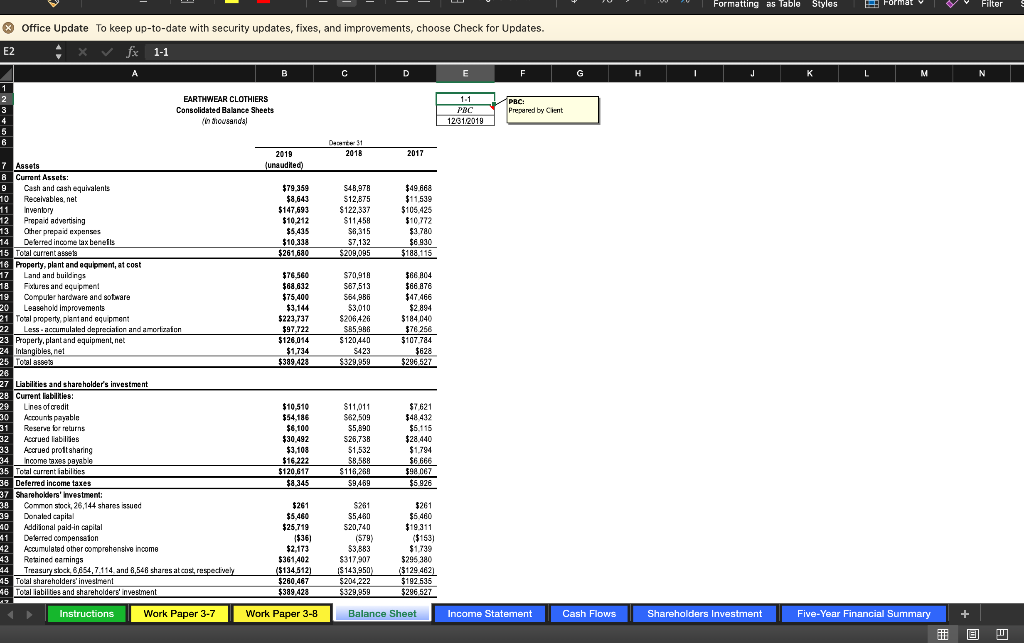

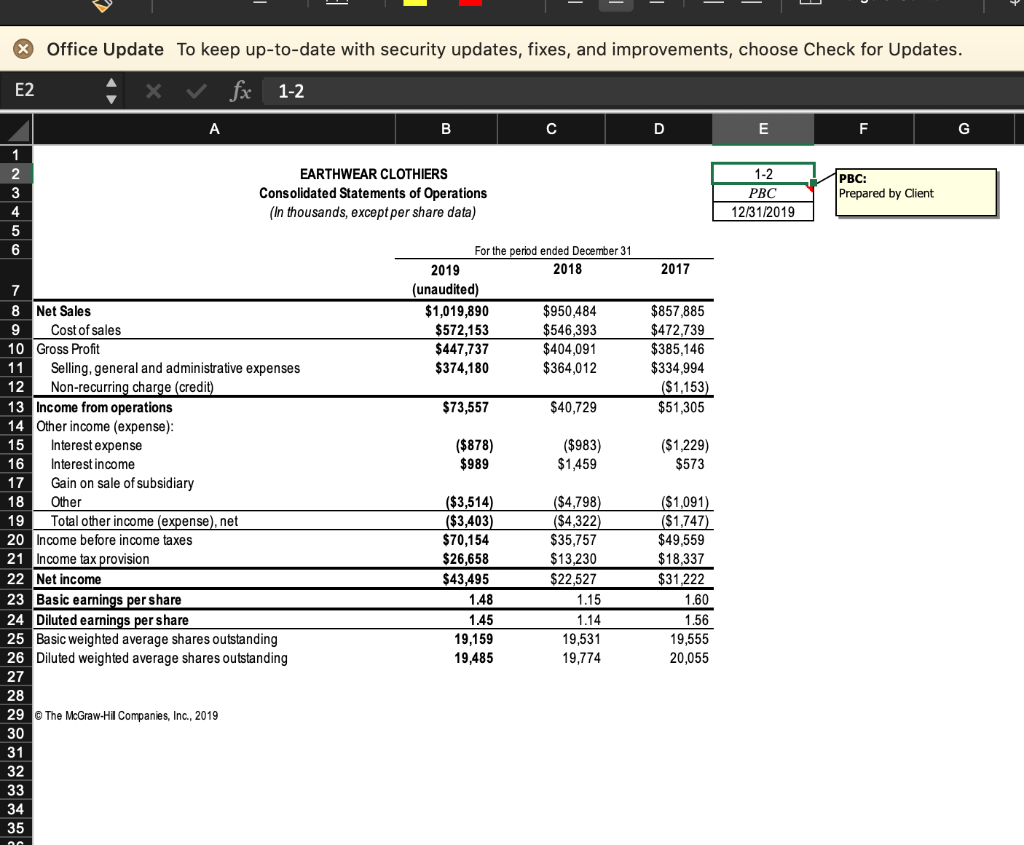

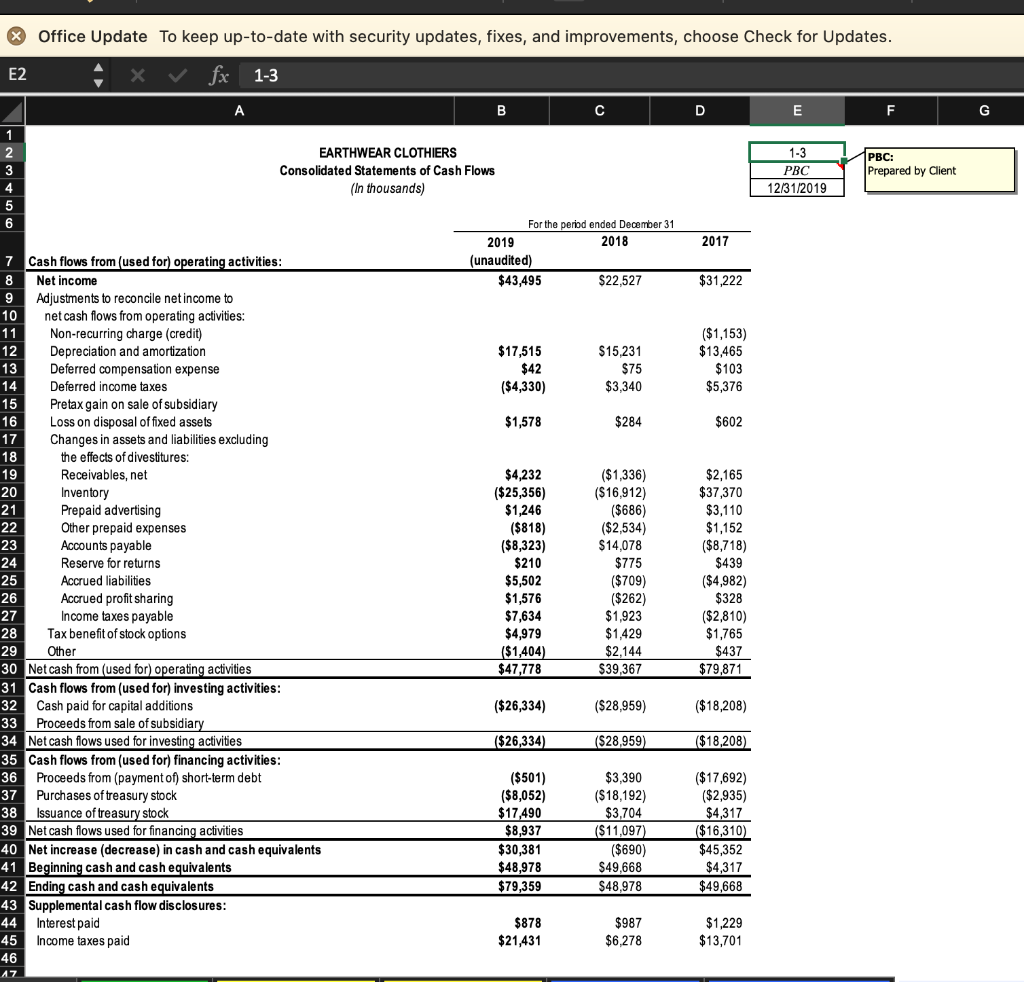

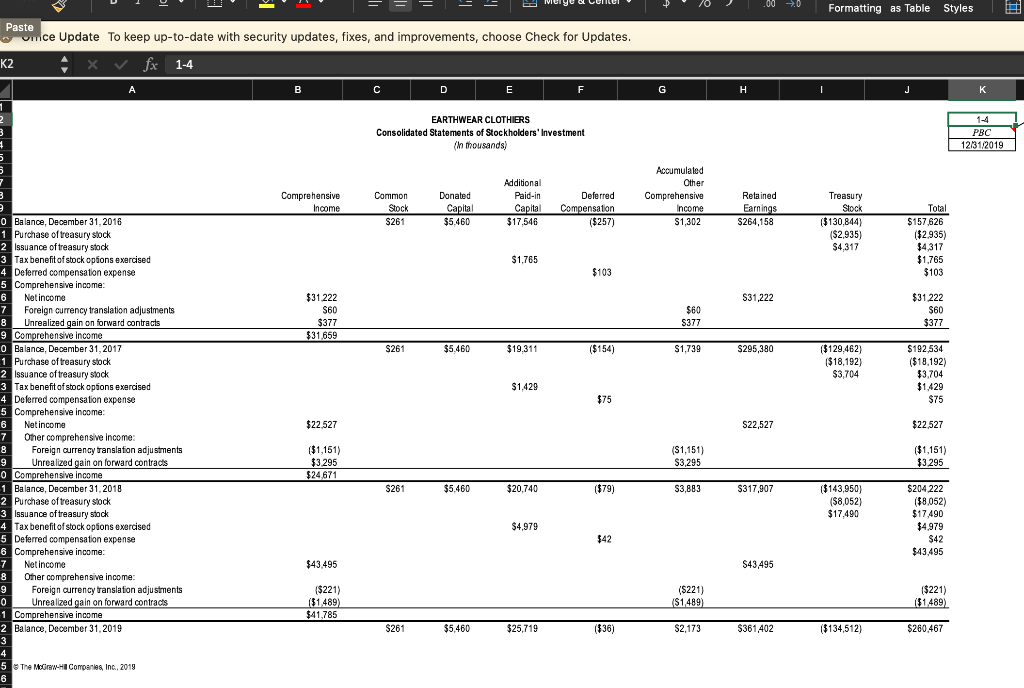

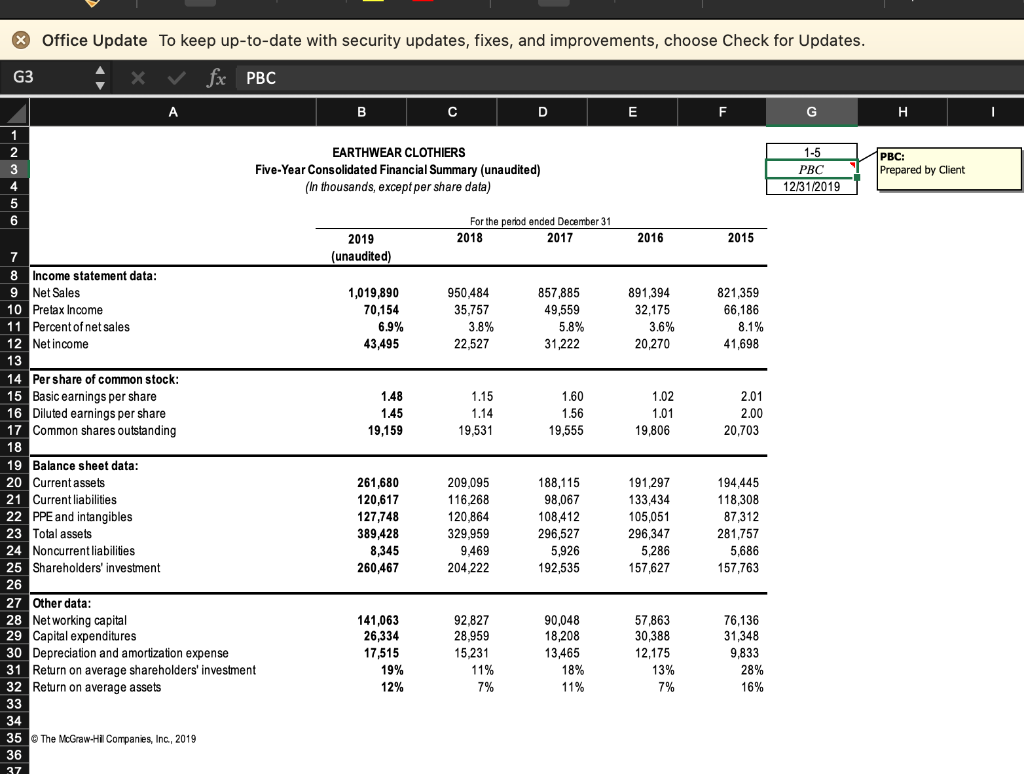

In this mini-case you will determine overall materiality as well as tolerable misstatement amounts for balance sheet accounts of EarthWear Clothiers, Inc. Most auditing firms use a simple approach for establishing planning materiality and tolerable misstatement similar to the one illustrated in your textbook. This case illustrates such an approach, with some additional guidance from Willis & Adams relating to the amount of tolerable misstatement to allocate to various balance sheet accounts based on difficulty to audit and expected misstatement, and limiting the total amount of tolerable misstatement to about ten times materiality. INSTRUCTIONS: Please download the files below to complete the audit tasks associated with this mini-case. The Excel workbook contains the instructions and workpapers you are to complete. 11e_Ch3_Mini_case_Materiality Materiality Guidelines Using your completed Excel file, answer the questions presented below. The fields below will be populated automatically as you complete the assigned workpapers. You may need to resize the rows to display your complete answer. Input your responses below into Connect. Measurement Base Factors that you considered to determine the appropriate measurement base Percentage Applied 5.0 % (Round your answer to 1 decimal place.) Factors that you considered to determine the appropriate percentage applied There seems to be a moderate risk of misstatement due to the measurement base and the evidence of the changes in revenue, pre-tax, and total assets. I used the information to choose because it's a moderate percentage. I was also able to get more evidence this way. Planning Materiality $ 3508 Total Amount of Tolerable Misstatement Allocated To Balance Sheet Accounts $ 2043 Ratio of Total Tolerable Misstatement to Planning Materiality 1/10 (Round your answer to 1 decimal place.) B E L M Name Box Account Name 2018 Cash and cash equivalents $48,978 Receivables, net $12,875 Inventory $122,337 Prepaid expenses $17,772 Deferred income tax benefits $7,132 Property, Plant, & Equipment $206,426 Accumulated depreciation and amortization $85,986 Intangibles, net $423 Lines of credit $11,011 Accounts payable & Reserve for returns $68,399 Accrued liabilities & Accrued profit sharing $28,270 Income taxes payable & Deferred income taxes $18,057 Common stock, 26,121 shares issued $261 Donated capital $5,460 Additional paid-in capital $20,740 Deferred compensation ($79) Accumulated other comprehensive income $3,883 Retained earnings $317,907 Treasury stock, 6,546 and 6,706 shares at cost, respectively ($ 143,950) Total Amount of Tolerable Mis statement Allocated To Balance Sheet Accounts Planning Materiality (from work paper 3-7) Ratio of Total Tolerable Misstatement to Planning Materiality *** 2019 Unaudited Trial Balance $79,359 $8,643 $147,693 $15,647 $10,338 $223,736 $97,722 $1,734 $10,510 $ 60,286 $33,600 $24,567 $261 $5,460 $25,719 ($36) $2,173 $361,402 ($134,512) F G H I J Tolerable Mis statement as % of Tolerable Planning Account Mis statement Materiality * Balance ** $2 0% 0% $2 0% 0% $0 0% 0% $2 0% 0% $0 0% 0% $0 0% 0% $2 0% 0% $2 0% 0% $0 0% 0% $2 0% 0% $34 0% 0% $25 0% 0% $65 0% 25% $1,365 0% 25% $0 0% 0% $0 0% 0% $543 0% 25% Not Applicable Not Applicable Not Applicable $0 0% 0% $2,043 Complete Work Paber 3-7 0.0 Explanation simple to verify large and complex account with misstatements expected, costly to audit Large and complex account with misstatements expected, costly to audit routine accounting expected w/ use of analytical procedures Relatively complex, estimation involved, related to Deferred Income Taxes Relatively little change from prior year, not difficult to audit accounting estimate tested w/ use of substansive analytical procedures the amount will be impared which is not difficult to audit Relatively little volume, not difficult to audit via 3rd party info realativley difficult to audit with some differences expected realatively costly to audit with some differences expected No change from prior year, easily verified No change from prior year, easily verified No change from prior year, easily verified Little change from prior year, not difficult to audit Not difficult to audit , examine current year vesting activity Involves some complex applications of GAAP Not Applicable Little change from prior year, not difficult to audit Willis & Adams Tolerable Mis statement Guidelines Tolerable misstatement should be between 50% and 75% of planning materiality. ** Tolerable misstatement should not exceed 25% of the account balance The total amount of tolerable misstatement allocated to balance sheet accounts should be below ten times materiality in order to limit aggregation risk. Formatting as Table Styles B Format Filter Office Update To keep up-to-date with security updates, fixes, and improvements, choose Check for Updates. X fx 1-1 E2 A D D F T J K L M N 1 1 2 3 4 5 B EARTHWEAR CLOTHIERS Consolidated Balance Sheets In diousands) ! 1-1 POC 1261.2019 PRC Prepared by Cint DATE 31 2018 2017 2019 (unaudited) $79.359 $8.643 $147,693 $10 212 $5,435 $10.338 $261 680 S48,978 $12,875 $122,337 $11,458 $8,315 57,132 $209,095 $49.668 $11.539 $105.425 $10 772 $3780 $6.930 $188,115 $ $76,560 $68.832 $75,400 $3,144 $223,737 $97,722 $126.014 $1.734 $389423 S70,918 S87,513 564,986 53,010 $206,426 S35,986 $120,440 S423 $329,959 $66 804 $66.876 $47.466 $2 $2894 $184 040 $76 256 $107.784 $628 $296 527 7 Assets 8 & Current Assets: 9 Cash and cash equivalents 10 Receivables.net 11 Inventory 12 Prepaid advertising 13 Other prepaid expenses 14 Deferred income tax benefis 15 Total current assets 16 Property, plant and equipment, at cost 17 Land and buildings 18 Fixtures and equipment 19 Computer hardware and sotware 20 Leasehold Improvements 21 Total property, plant and equipment 22 Less-accumulated depreciation and amerlaton 23 Property, plant and equipment, net 24 Intangibles net 25 Total 26 27 Liabilities and shareholder's investment 28 Current liabilities: 29 Lines of credit 30 Acounts payable 31 Reservorreburns 32 Accrued abilities 33 Accrued prottsharing 34 ncome taxes payable 35 Total current abilities 36 Deferred income taxes 37 Shareholders' Investment: 39 Common stock, 26.144 shares issued 39 Donaled capital 40 Additional paid-in capital 41 Deterred compensaton 42 Accumulated other comprehensive Income 43 Retained earnings 44 Treasury slock 6,654,7.114 and 8,548 shares at cas, respectively 45 Toul shareholders'investment 46 Totaltabiles and shareholders investment $10,510 $54,186 $ $6,100 $30.492 $3,108 $16.222 $120.617 $8345 $11,011 S62,509 $5,890 S28,738 $1,532 $8.588 $116,268 59,489 $7621 $48 432 $6.115 $28.440 $1,794 $6 666 $98 067 $5.926 $261 $5,460 $25,719 {$ $36) $2,173 $361,402 ($134,512) $260,467 $389428 $261 S5486 S20,740 (579) 53,883 $317,907 IS 143,950) $204,222 $329,959 $261 $6.460 $19.311 ($153) $1.739 $295 380 ($129.462) $192535 $296 527 Instructions Work Paper 3-7 Work Paper 3-8 Balance Sheet Income Statement Cash Flows Shareholders Investment Five-Year Financial Summary + Office Update To keep up-to-date with security updates, fixes, and improvements, choose Check for Updates. E2 fx 1-2 A B D E F G 1-2 EARTHWEAR CLOTHIERS Consolidated Statements of Operations (In thousands, except per share data) PBC: Prepared by Client 1 2 3 4 5 6 PBC 12/31/2019 2017 For the period ended December 31 2019 2018 (unaudited) $1,019,890 $950,484 $572,153 $546,393 $447,737 $404,091 $374,180 $364,012 $857,885 $472,739 $385,146 $334,994 ($1,153) $51,305 $73,557 $40,729 ($878) $989 ($983) $1,459 ($1,229) $573 7 8 Net Sales 9 Cost of sales 10 Gross Profit 11 Selling, general and administrative expenses 12 Non-recurring charge (credit) 13 Income from operations 14 Other income (expense): 15 Interest expense 16 Interest income 17 Gain on sale of subsidiary 18 Other 19 Total other income (expense), net 20 Income before income taxes 21 Income tax provision 22 Net income 23 Basic earnings per share 24 Diluted earnings per share 25 Basic weighted average shares outstanding 26 Diluted weighted average shares outstanding 27 28 29 The McGraw-Hil Companies, Inc., 2019 30 31 32 33 34 35 ($3,514) ($3,403) $70,154 $26,658 $43,495 1.48 1.45 19.159 19,485 ($4,798) ($4,322) $35,757 $13,230 $22,527 1.15 1.14 19,531 19,774 ($1,091) ($1,747) $49,559 $18,337 $31,222 1.60 1.56 19,555 20,055 Office Update To keep up-to-date with security updates, fixes, and improvements, choose Check for Updates. E2 fx 1-3 A B C D E F G 1 EARTHWEAR CLOTHIERS Consolidated Statements of Cash Flows (In thousands) 3 4 1-3 PBC 12/31/2019 PBC: Prepared by Client 6 2018 2017 For the period ended December 31 2019 (unaudited) $43,495 $22,527 $31,222 $17,515 $42 ($4,330) $15,231 $75 $3,340 ($1,153) $13,465 $103 $5,376 $1,578 $284 $602 7 Cash flows from used for operating activities: 8 Net income 9 Adjustments to reconcile net income to 10 net cash flows from operating activities: 11 Non-recurring charge (credit) 12 Depreciation and amortization 13 Deferred compensation expense 14 Deferred income taxes 15 Pretax gain on sale of subsidiary 16 Loss on disposal of fixed assets 17 Changes in assets and liabilities excluding 18 the effects of divestitures: 19 Receivables, net 20 Inventory 21 Prepaid advertising 22 Other prepaid expenses 23 Accounts payable 24 Reserve for returns 25 Accrued liabilities 26 Accrued profit sharing 27 Income taxes payable 28 Tax benefit of stock options 29 Other 30 Net cash from (used for operating activities 31 Cash flows from (used for) investing activities: 32 Cash paid for capital additions 33 Proceeds from sale of subsidiary 34 Net cash flows used for investing activities 35 Cash flows from (used for) financing activities: 36 Proceeds from (payment of short-term debt 37 Purchases of treasury stock 38 Issuance of treasury stock 39 Net cash flows used for financing activities 40 Net increase (decrease) in cash and cash equivalents 41 Beginning cash and cash equivalents 42 Ending cash and cash equivalents 43 Supplemental cash flow disclosures: 44 Interest paid 45 Income taxes paid 46 AZ $4,232 ($25,356) $1,246 ($818) ($8,323) $210 $5,502 $1,576 $7,634 $4,979 ($1,404) $47,778 ($1,336) ($16,912) ($686) ($2,534) $14,078 $775 ($709) ($262) $1,923 $1.429 $2,144 $39,367 $2,165 $37,370 $3,110 $1,152 ($8,718) $439 ($4,982) $328 ($2,810) $1,765 $437 $79,871 ($26,334) ($28,959) ($18,208) ($26,334) ($28,959) ($18,208) ($501) ($8,052) $17,490 $8,937 $30,381 $48,978 $79,359 $3,390 ($18,192) $3,704 ($11,097) ($690) $49,668 $48,978 ($17,692) ($2,935) $4,317 ($16,310) $45,352 $4,317 $49,668 $878 $21,431 $987 $6,278 $1,229 $13,701 .00 7,0 Formatting as Table Styles Paste omce Update To keep up-to-date with security updates, fixes, and improvements, choose Check for Updates. K2 x fox 1-4 B D E A C E G H J EARTHWEAR CLOTHIERS Consolidated Statements of Stockholders' Investment (In thousands) ) 1-4 PBC 12/31/2019 Comprehensive Income Common Stock S261 Donated Capital $5.460 $ Additional Paid-in Capital $17,546 Deferred Compensation ($257) Accumulated Other Comprehensive Income S1,302 Retained Earnings $264,158 Treasury Stock ($130,844) ($2,935) $4.317 Total $157,626 ($2.935) $4,317 $1,765 $103 $1.765 $103 $31,222 $31.222 $60 $377 $31659 $60 $377 $31222 $60 $377 S261 $5,460 $19.311 ($154) S1,739 $295,380 ($129,462) ($18,192) $3,704 $192,534 ($18,192) $3,704 $1,429 $75 $1.429 $75 $22.527 S22,527 $22.527 3 0 Balance, December 31, 2016 1 Purchase of treasury stock Issuance of treasury stock Tax benefit of stock options exercised 4 Deferred compensation expense 5 Comprehensive income: 6 Net income 7 Foreign currency translation adjustments 8 Unrealized gain on forward contracts 9 Comprehensive income 0 Balance, December 31, 2017 1 Purchase of treasury stock 2 Issuance of treasury stock Tax benefit of stock options exercised 4 Deferred compensation expense 5 Comprehensive income: 6 Net income 7 Other comprehensive Income 8 Foreign currency translation adjustments 9 Unrealized gain on forward contracts 0 Comprehensive income Balance, December 31, 2018 Purchase of treasury stock 3 Issuance of treasury stock 4 Tax benefit of stock options exercised Deferred compensation expense 6 Comprehensive income: 7 Net income 8 Other comprehensive income: 9 Foreign currency translation adjustments 0 Unrealized gain on forward contracts 1 Comprehensive income 2 Balance, December 31, 2019 3 4 4 5 The M Grew-H Companies, Inc, 2019 6 ($1,151) $3295 $24671 (S1,151) $3,295 ($1,151) $3295 $261 $5,460 $20,740 ($79) $3,883 $317.907 ($143.950) ($8,052) $17.490 $204 222 ($8,052) $17,490 $4.979 $42 $43,495 $4,979 $42 $43,495 $43.495 ($221) ($1.489) $41.785 ($221) ($1,489) ($221) ($1.489) $261 $5,460 $25,719 ($36) $2,173 $361 402 ($134,512) $260,467 Office Update To keep up-to-date with security updates, fixes, and improvements, choose Check for Updates. G3 x fx PBC A B B D E F G G H I 1 2 2 3 4 5 6 EARTHWEAR CLOTHIERS Five-Year Consolidated Financial Summary (unaudited) (In thousands, except per share data) 1-5 PBC 12/31/2019 PBC: Prepared by Client For the period ended December 31 2018 2017 2016 2015 2019 (unaudited) 1,019,890 70,154 6.9% 43,495 950,484 35,757 3.8% 22,527 857,885 49,559 5.8% 31,222 891,394 32,175 3.6% 20,270 821,359 66,186 8.1% 41,698 1.48 1.45 19,159 1.15 1.14 19,531 1.60 1.56 19,555 1.02 1.01 19,806 2.01 2.00 20,703 7 8 Income statement data: 9 Net Sales 10 Pretax Income 11 Percent of net sales 12 Net income 13 14 Per share of common stock: : 15 Basic earnings per share 16 Diluted earnings per share 17 Common shares outstanding 18 19 Balance sheet data: 20 Current assets 21 Current liabilities 22 PPE and intangibles 23 Total assets 24 Noncurrent liabilities 25 Shareholders' investment ' 26 27 Other data: 28 Networking capital 29 Capital expenditures 30 Depreciation and amortization expense 31 Return on average shareholders' investment 32 Return on average assets 33 34 35 The McGraw-Hill Companies, Inc., 2019 36 37 261,680 120,617 127,748 389,428 8,345 260,467 209.095 116,268 120,864 329,959 9,469 204,222 188,115 98,067 108,412 296,527 5,926 192,535 191,297 133,434 105,051 296,347 5.286 157,627 194,445 118,308 87,312 281,757 5,686 157,763 141,063 26,334 17,515 19% 12% 92,827 28,959 15.231 11% 7% 90,048 18,208 13,465 18% 11% 57,863 30,388 12,175 13% 7% 76,136 31,348 9,833 28% 16%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts