Question

AUDITING AND ASSURANCE SERVICES - QUESTION 8, 9 & 10 - PLEASE AND THANK YOU! (ALL QUESTION ANSWERS MUST BE 100-200 WORDS LONG) In Ch.

AUDITING AND ASSURANCE SERVICES - QUESTION 8, 9 & 10 - PLEASE AND THANK YOU! (ALL QUESTION ANSWERS MUST BE 100-200 WORDS LONG)

In Ch. 4 lecture, I give two examples about the relevance of ethics to auditing. The following 3 questions are related to these two examples.

Example 1. After you have performed all required and planned audit procedures, and based on your professional expertise and your knowledge about your client, you concluded, in your mind, that the current level of the company's allowance for bad debt expense was lower than the level it should be at. This is your professional judgment. As we discussed in previous chapters, your judgment could be wrong. Neither the auditing standards nor your knowledge of common practice provide clear guidance as to what further actions you need to take. You have not committed any negligence. Therefore, you should not get sued if you do nothing. In other words, you are legally safe if you go along with your client on this. However, your professional conscience tells you that you perhaps need to do more, even though your further action could upset your client, which may cost you and your firm this client.

Example 2. You work alone checking purchase authorizations as part of a planned test of internal control. The work has to be completed today according to the audit plan and budget. The work is time-consuming. It is getting late and you have an important date tonight. You have been auditing this client for several years and you know the company always had good internal controls over accounting procedures. You also know that internal controls have only indirect relationship with the quality of financial statements, as we discussed in this class earlier. Now, do you want to skip examining a couple of purchase orders and sign off your work prematurely? Premature signing off is as bad as fraud (it is the case that you know you did not do the required audit work but you say you did it), but you work alone and apparently no one would know that you signed off your work without doing it completely.

QUESTION 8. Using these two examples, explain why in this class we need to discuss both professional ethics and legal liabilities for auditors. (100-200 WORDS)

QUESTION 9. Is the "dying-man" story, on p. 80 of the book, similar to Example 1, or to Example 2? Why? (100-200 WORDS)

(DYING-MAN CASE BELOW)

QUESTION 10. Is Example 1 a case of auditor independence in fact and Example 2 a case of auditor independence in appearance? Why or why not? How are independence in fact and independence in appearance related? (100-200 WORDS)

HERE ARE CHAPTER 4 CONCEPTS AS REFERENCE FROM THE BOOK.

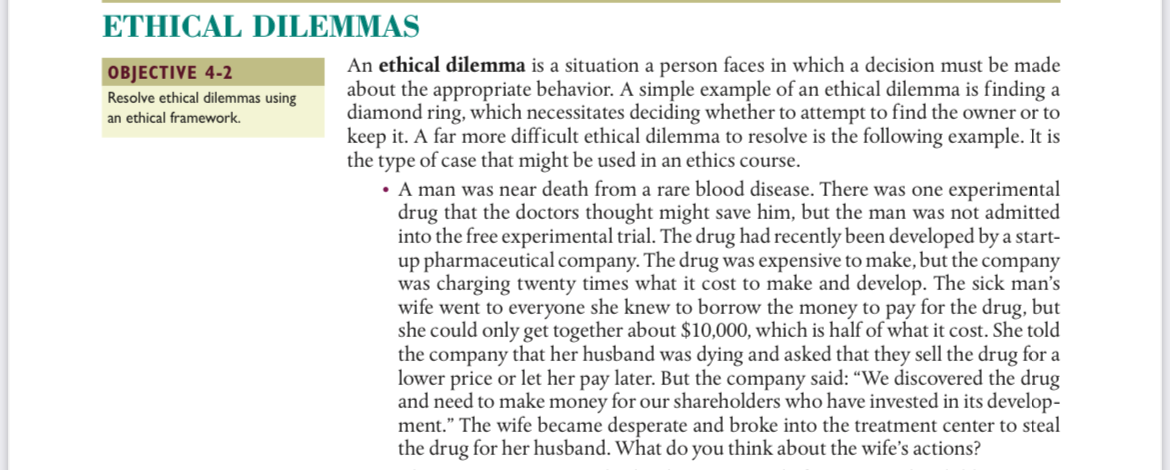

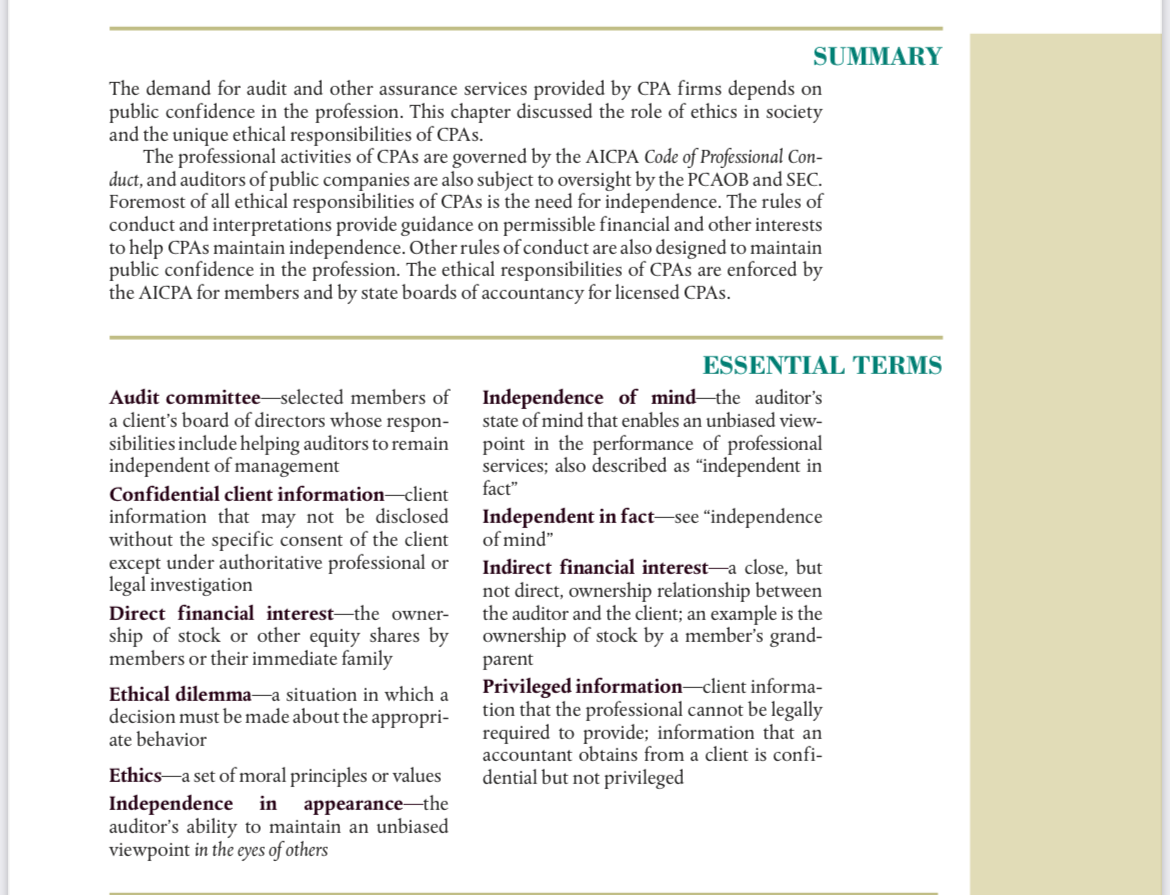

an ethical framework. ETHICAL DILEMMAS OBJECTIVE 4-2 An ethical dilemma is a situation a person faces in which a decision must be made Resolve ethical dilemmas using about the appropriate behavior. A simple example of an ethical dilemma is finding a diamond ring, which necessitates deciding whether to attempt to find the owner or to keep it. A far more difficult ethical dilemma to resolve is the following example. It is the type of case that might be used in an ethics course. A man was near death from a rare blood disease. There was one experimental drug that the doctors thought might save him, but the man was not admitted into the free experimental trial. The drug had recently been developed by a start- up pharmaceutical company. The drug was expensive to make, but the company was charging twenty times what it cost to make and develop. The sick man's wife went to everyone she knew to borrow the money to pay for the drug, but she could only get together about $10,000, which is half of what it cost. She told the company that her husband was dying and asked that they sell the drug for a lower price or let her pay later. But the company said: We discovered the drug and need to make money for our shareholders who have invested in its develop- ment. The wife became desperate and broke into the treatment center to steal the drug for her husband. What do you think about the wife's actions? SUMMARY The demand for audit and other assurance services provided by CPA firms depends on public confidence in the profession. This chapter discussed the role of ethics in society and the unique ethical responsibilities of CPAs. The professional activities of CPAs are governed by the AICPA Code of Professional Con- duct, and auditors of public companies are also subject to oversight by the PCAOB and SEC. Foremost of all ethical responsibilities of CPAs is the need for independence. The rules of conduct and interpretations provide guidance on permissible financial and other interests to help CPAs maintain independence. Other rules of conduct are also designed to maintain public confidence in the profession. The ethical responsibilities of CPAs are enforced by the AICPA for members and by state boards of accountancy for licensed CPAs. Audit committeeselected members of a client's board of directors whose respon- sibilities include helping auditors to remain independent of management Confidential client information client information that may not be disclosed without the specific consent of the client except under authoritative professional or legal investigation Direct financial interestthe owner- ship of stock or other equity shares by members or their immediate family Ethical dilemma-a situation in which a decision must be made about the appropri- ate behavior Ethicsa set of moral principles or values Independence in appearancethe auditor's ability to maintain an unbiased viewpoint in the eyes of others ESSENTIAL TERMS Independence of mindthe auditor's state of mind that enables an unbiased view- point in the performance of professional services; also described as independent in fact" Independent in fact-see independence of mind" Indirect financial interesta close, but not direct, ownership relationship between the auditor and the client; an example is the ownership of stock by a member's grand- parent Privileged information client informa- tion that the professional cannot be legally required to provide; information that an accountant obtains from a client is confi- dential but not privileged

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Innovation Commercialization And Start Ups In Life Sciences

Authors: James F. Jordan

1st Edition

1482210126, 978-1482210125