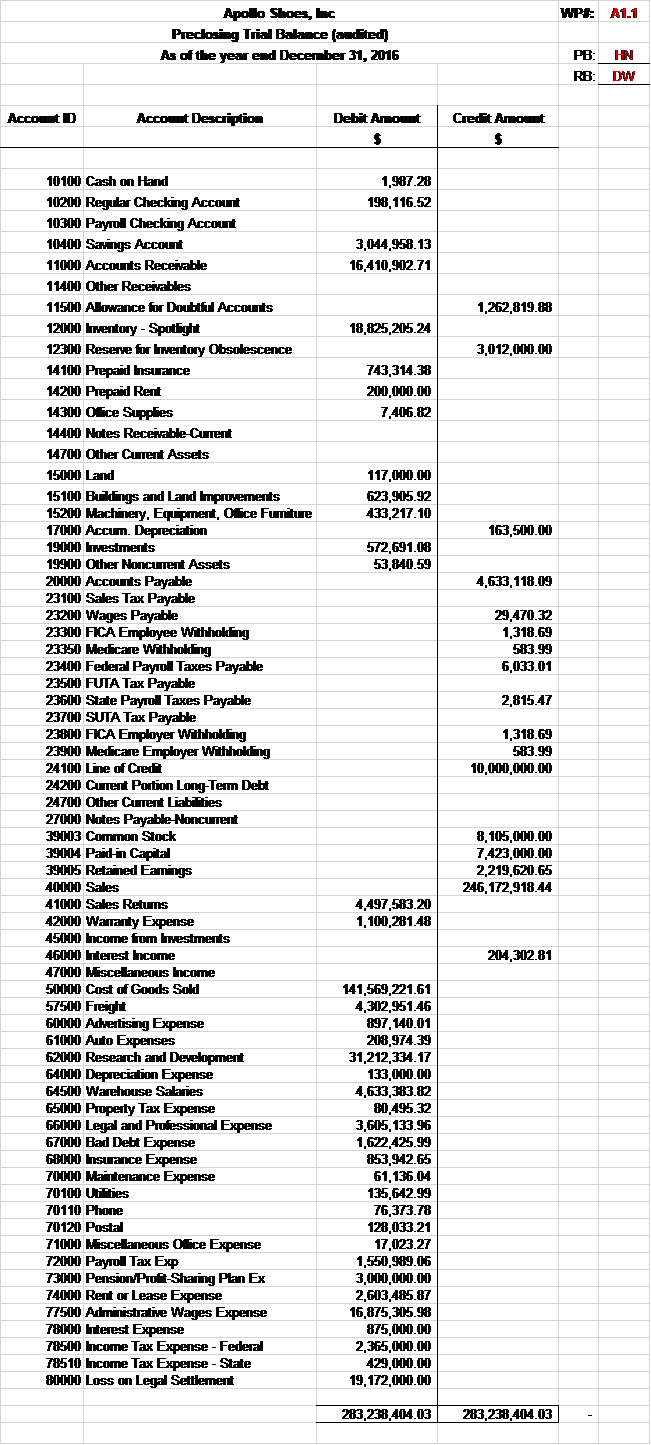

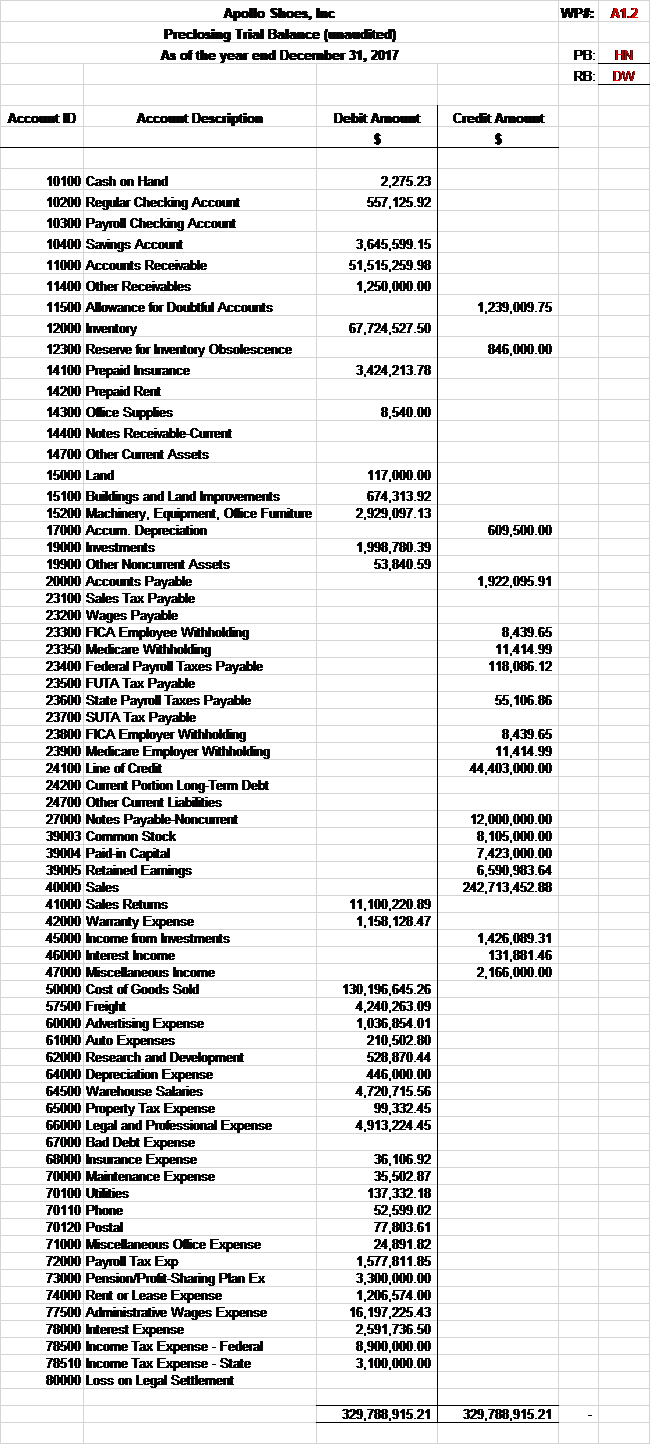

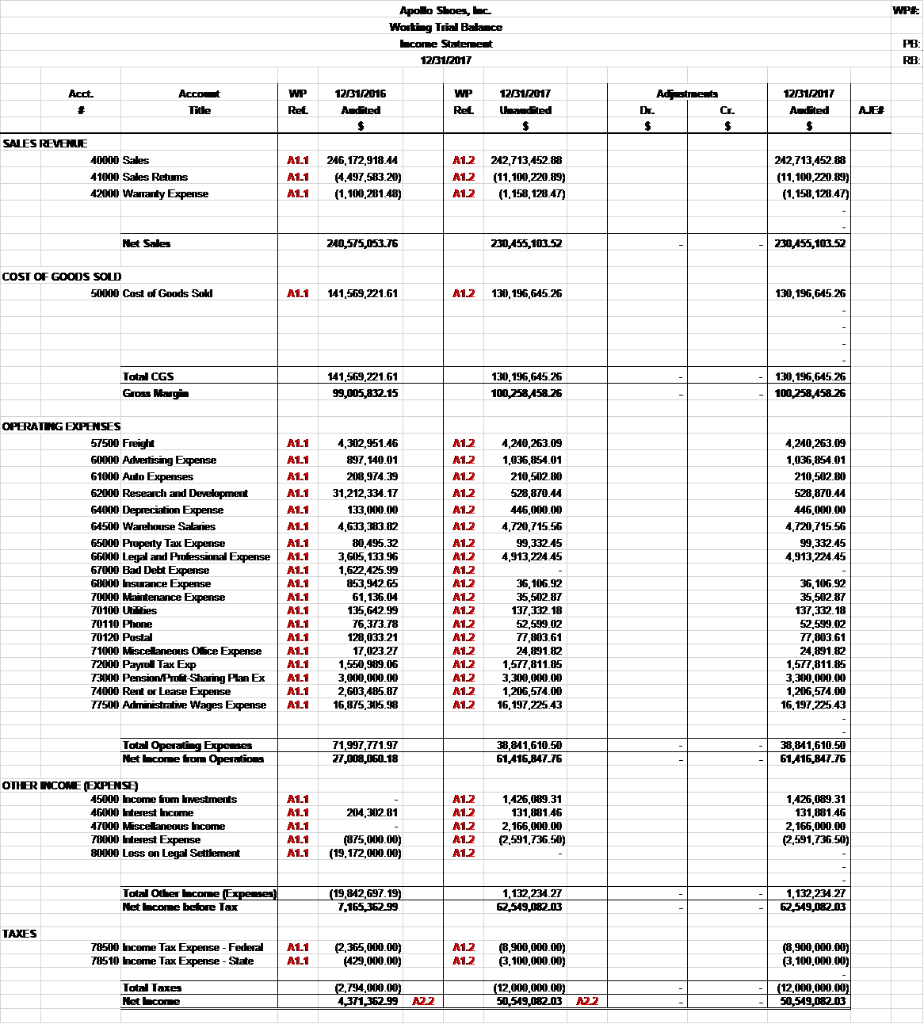

Auditing

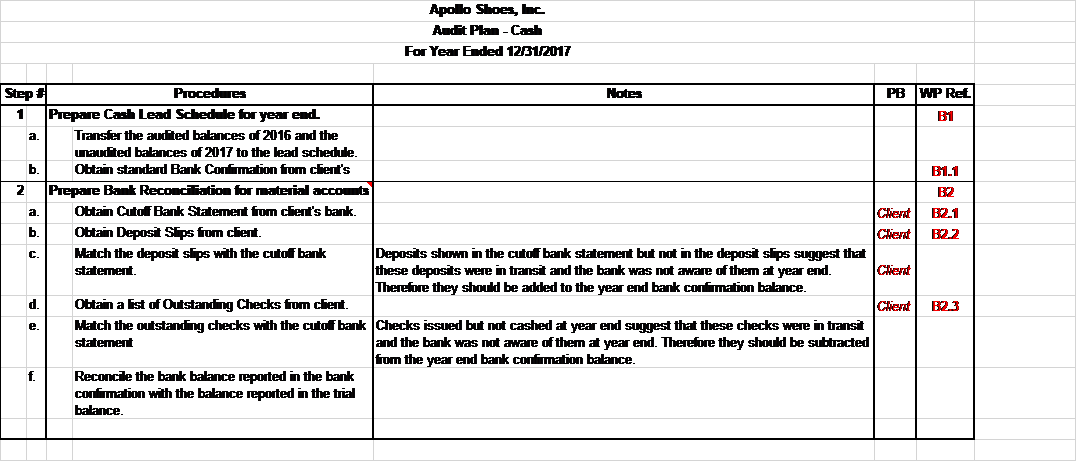

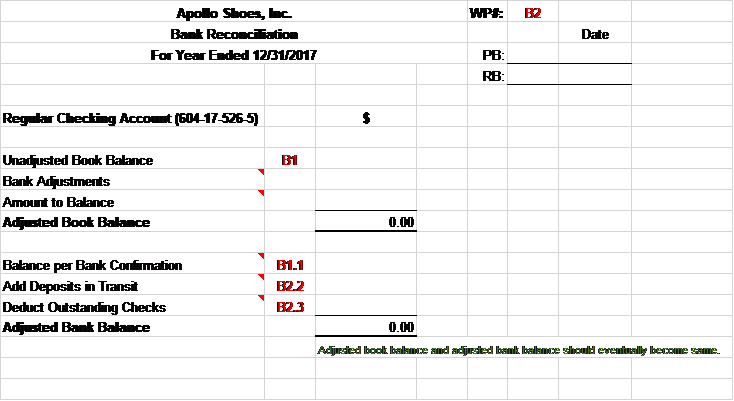

Apollo Shoes, Inc. is an audit case designed to introduce you to the entire audit process, from planning the engagement to drafting the final report. You are to assume the role of a staff auditor at Anderson, Olds, and Watershed (AOW) CPAs and work on the financial audit of a client, Apollo Shoes, Inc. This assignment focuses on the planning process of the audit. This assignment contains various communications from the Darlene Wardlaw, Engagement Manager at AOW CPAs. Each communication contains certain assignment requirements highlighted in bold. The documents mentioned in the Attachments section of a communication are available in the Content area of D2L in Apollo Shoes module. The information in this assignment is sequential in nature. In other words, pay close attention to information disclosed early in the audit (for example, in the Board of Directors' meeting minutes) as it may play a role in subsequent audit work contained in other assignments. Limitations of the case: While the case is as realistic as possible, you are unable to follow up directly with client personnel. Therefore, you will have to rely on evidence provided to you through D2L. In an actual audit, you would be able to inquire, observe, and otherwise follow-up on any questions that you have until you feel comfortable relying on the evidence. Also, to make sure that the case can be completed in a reasonable amount of time, most of the audit sampling is already done for you. Understand that audit sampling plays a large role in actual audit practice and you might have to be directly involved with the sampling procedures. Cash Audit You are to conduct a cash audit of Apollo Shoes, Inc. The cash audit is designated with the B series. So, any document starting with B is a primary document for cash audit You will be working on the following workpapers during your audit of cash: B Cash - Audit Plan B1 Cash - Lead Schedule B1.1 Bank Confirmation B2 Bank Reconciliation B2.1 Cutoff Bank Statement B2.2 Deposit slips B2.3 Outstanding checks The Assignment 3 - TEMPLATE.xlsx posted on D2L includes an audit plan for cash (worksheet B). An actual audit plan for cash is a lot more detailed. However, for the sake of simplicity, we will be using a much basic audit plan. This assignment will introduce you to examining evidence so pay close attention to detail. Mastery of bank reconciliation will prove to be very beneficial in this assignment You will also be making one adjusting journal entry in this assignment. Use the Assignment 3 - TEMPLATE to record your audit work and submit it to the dropbox by the due date. Date: 19 JAN 2018 15:37:42 +0000 From: "Darlene Wardlay" Subject: Audit of Cash Attachments: >, >, >, > I want you to start with the cash audit. We have received the Bank Confirmation (WP ref# B1.1) and the January 2018 cutoff bank statement (WP ref# B2.1) directly from Apollo's bank. We have also received the deposits slips for deposits made immediately after the year end (WP ref# B2.2) and list of outstanding checks at the year end (WP ref# 2.3) from the client. These documents should be sufficient for creating Bank Reconciliation (WP ref# B2). Begin by preparing a cash lead schedule so that we know which accounts are significant and therefore while need to be audited. After completing the cash lead schedule, start auditing the regular checking account by comparing the book balance in the lead schedule with the balance provided in the bank confirmation. Obviously there will be differences due to deposits in transit and outstanding checks. So prepare a bank reconciliation to adjust the book balance with any deposits or withdrawals the client might not have known at year end, and adjust the bank balance with any deposits or withdrawals the bank might not have known at year end. FYI, while auditing the accounts payable, I came across an account that was paid but not recorded in the books. This means that the cash might be overstated. See if you can find any check in the 2018 cutoff bank statement that was not recorded as an outstanding check at the 2017 year end. If you find a missing outstanding check, please post an adjusting entry accordingly in workpaper AJE and make adjustments in the cash lead schedule (B1) as well as the working trial balance (A2.1 & A2.2) Your ability to properly reference your workpapers is critical for me to understand where you got the information from and to which other workpapers did the information go to. The way workpapers are referenced in auditing is based on the concepts of tracing and vouching. Preceding workpapers are referenced towards the left and succeeding workpapers are referenced towards the right. Basically, a reference on the left shows where the information is coming from and a reference on the right shows where the information is going. For example, when preparing the Bank Reconciliation, the Balance per Bank Confirmation should have B1.1 referenced towards the left of the amount to show other auditors that the information is coming from the Bank Confirmation, in the Bank Confirmation, the same amount should have B2 referenced towards the right to show other auditors that the amount is going to the Bank Reconciliation Talk to you soon. DW WPE A11 Apollo Shoes, hec Preclosing Trial Balance (audited) As of the year end December 31, 2016 PB: HN RB: DW AccoD Account Description Debit Amoet Credit Amoet 1,987.28 198,116.52 3,44,958.13 16,410,902.71 1,262,819.88 18,825,205.24 3,012,000.00 743,314.38 200.000.00 7,406.82 117,000.00 623,915.92 433,217.10 163,500.00 572,691.18 53,840.59 4,633,118.09 29,470.32 1,318.69 583.99 6,033.01 2,815.47 1,318.69 583.99 10,000,000.00 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alowance for Doubtft Accounts 12000 Inventory - Spotlight 12300 Reserve for hventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Cument 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Ofice Fumiture 17000 Accum. Depreciation 19000 Westments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholfing 23400 Federal Payroll Taxes Payable 2300 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23900 FICA Employer Withholfing 239.00 Medicare Employer Withholding 24100 Line of Credi 24200 Cument Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurrent 39003 Common Stock 39014 Paid in Capital 39005 Retained Eamings 40000 Sales 41000 Sales Retums 42000 Warranty Expense 45000 Income from Investments 46000 hterest Income 47000 Miscellaneous Income 50100 Cost of Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 7200 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 809Loss on Legal Settlement 8,105,000.00 7,423,000.00 2,219,620.65 246,172,918.44 4,497,583.20 1,100,281.48 214,312.81 141,569,221.61 4,312,951.46 897,140.01 218,974.39 31,212,334.17 133,000.00 4,633,383.82 80,495.32 3,615, 133.96 1,622,425.99 853,942.65 61,136.14 135.642.99 76,373.78 128,033.21 17.023.27 1,550,989.06 3,000,000.00 2,603,485.87 16,875,315.98 875,000.00 2,365,000.00 429,000.00 19,172,000.00 283,238,404.03 2 83,238,404.03 WP A12 Apollo Shoes, ac Preclosing Trial Balance ( dited) As of the year end December 31, 2017 PB: HN RB: DW AccoD Account Description Debit Amount Credit Amoet 2,275.23 557,125.92 3,645,599.15 51,515,259.98 1,250,000.00 1,239,019.75 67,724,527.50 846,000.00 3,424,213.78 8,540.00 117,000.00 674,313.92 2,929,097.13 619,500.00 1,948,780.39 53,840.59 1,922,095.91 8,439.65 11,414.99 118,686.12 55,106.86 8,439.65 11,414.99 44,403,000.00 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts 12000 nentory 12300 Reserve for hventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Cument 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Ofice Fumiture 17000 Accum. Depreciation 19000 Westments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholfing 23400 Federal Payroll Taxes Payable 2300 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23900 FICA Employer Withholfing 239.00 Medicare Employer Withholding 24100 Line of Credi 24200 Cument Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurrent 39003 Common Stock 39014 Paid in Capital 39005 Retained Eamings 40000 Sales 41000 Sales Retums 42000 Warranty Expense 45000 Income from Investments 46000 hterest Income 47000 Miscellaneous Income 50100 Cost of Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 7200 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 809Loss on Legal Settlement 12,000,000.00 8,105,000.00 7,423,000.00 6,590,983.64 242,713,452.88 11,100,220.89 1,158,128.47 1,426,089.31 131,881.46 2,165,000.00 130.196,645.26 4,240,263.09 1,036,854.01 210.502.80 528.870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 36,106.92 35,512.87 137,332.18 52,599.02 77.813.61 24,891.82 1,577,811.85 3,300,000.00 1,216,574.00 16, 197,225.43 2,591,736.50 8,900,000.00 3,100,000.00 329,788,915.21 329,788,915.21 WPE Apollo Shoes, Inc. Working Til Bakance Income Statement 12/31/2017 RB Acct. Adestruents Account Title WP Ret 12/01/2016 Audited WP Ret 1231/2017 Uudited 12/31/2017 Audited AE SALES REVENLE 40000 Sales 41000 Sales Retums 42000 Warranty Expense A11 A11 AL1 246,172,918.44 (4,497,583.20) (1,100,281.48) M12 A12 A12 242,713,452.88 (11,100,220.89) (1,158,128.47) 242,713,452.88 (11,100.220.89) (1,158,128 47 Net Sales 240,575,053.76 230,455, 103.52 230,455,103.52 COST OF GOODS SOLD 50000 Cast of Goods Sold A11 141,569,221.61 | A1.2 130, 196,645.26 130, 196,645.26 Total CGS Gross Mary 141,569,221.61 99,005,832.15 130, 196,645.26 100,258,458.26 130, 196,645 26 100,258,458.26 A11 A11 A11 A11 A1.1 A11 AL1 AL1 A1.1 AL1 A11 AL1 4,240,263.09 1,036,854.01 210,502.80 528,870.14 446,000.00 4,720,715.56 99,332.45 4,913,224.45 OPERATING EXPENSES 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Prufessional Expense 67000 Bad Debt Expense GOOD Insurance Expense 70000 Maintenance Expense 70100 Uhies 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 73000 Pension Profit Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 4,240,263.09 1,036,854.01 210,502.80 528.870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 4,302,951.46 897.140.01 208,974.39 31,212,331.17 133,000.00 4,633, 23.02 80,495.32 3,605,133.96 1,622,425.99 853,942.65 61,136.04 135,642.99 76,373.78 128,033.21 17.023 27 1,550,989.06 3,000,000.00 2,603,485.87 16,875,305.98 A12 A12 A12 A12 A12 A12 A12 A1.2 A12 A12 A12 A1.2 A12 M12 A12 A12 A12 M12 A12 36,106.92 35,502.87 137 132.18 52,599.02 77,803.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16, 197,225.43 36,106.92 35,502.87 137,332.18 52,599.02 77,803.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16,197,225.43 A11 AL1 AL1 Total Operating Expenses Net lacome from Operations 71,997,771.97 27,008,060.18 38,811,610.50 61,416,847.76 38,841,610.50 61,416,847.76 204, 302.81 OTHER NCOME EXPENSE) 45000 Income from investments 46000 Interest Income 47000 Miscellaneous Income 78000 Interest Expense 80000 Loss on Legal Settlement AL1 A1.1 AL1 AL1 A11 A1.2 A12 A12 A1.2 A1.2 1,426,089.31 131,881.46 2,166,000.00 (2,591,736.50) 1,426,089.31 131,881.46 2,166,000.00 (2,591,736.50) (875,000.00) (19,172,000.00) Total Other Lacome Expenses) Net Lecome before Tax (19,842,697.19 7,165, 162.99 1,132,234.27 2,549,082.03 1,132,231.27 62,549,082.03 TAXES 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State AL1 AL1 (2,365,000.00) (429,000.00) A1.2 A12 (8,900,000.00) (3.100,000.00) (8,900,000.00) (3.100.000.00) Total Taxes Net lecome (2.744,000.00) 4,371, 362.99 (12,000,000.00) 50,549,082.03 A22 (12,000,000.00) 50,519,082.03 22 WPE Apollo Shoes, hec Working Trial Balance Bakance Sheet 1231/2017 PB: RB Acc. A stments Account Title WP Ret 1231/2016 Audited WP Ret 12/31/2017 audited 12/31/2017 Audited ASSETS 1,987.28 198,116.52 2,275.23 557,125.92 2,275.23 557,125.92 3,041,958.13 16,410,902.71 A1.1 A1.1 A1.1 A1.1 A1.1 A11 A1.1 A1.1 A1.1 A1.1 A1.1 A11 A11 AL1 A1.1 A1.1 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10000 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alkuwance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for entory Obsolescence 14100 Prepaid insurance 14200 Prepaid Rent 14300 Ofice Supplies 14400 Nates Receivable Current 1700 Other Current Assets 15000 Land 15100 Buklings and Land Improvements 15200 Machinery, Equipment, Olice Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets (1,262,819.88) 18.825,205 24 (3.012,000.00) 743,314.338 200,000.00 7,406.82 A12 A1.2 A1.2 A12 A1.2 A12 A1.2 A12 A12 A12 A1.2 A12 A12 A1.2 A12 3,615,599.15 51,515,259.90 1,250,000.00 (1,239,009.75) 67.724,527.50 (816,000.00) 3,424,213.78 3,615,599.15 51,515,259,98 1,250,000.00 (1,229,009.75) 67.724,527.50 (846,000.00) 3,424,213.78 8,540.00 8,510.00 117.000.00 623,905.92 413,217.10 (163,500.00) 572,691.08 53,840.59 A12 117,000.00 674,313.92 2,929,097.13 (609,500.00 1,998,780.39 53,840.59 117,000.00 674,313.92 2,929,097.13 (609,500.00 1,998,780.39 53,840.59 Total Assets 36,794,7%.89 15794 TX 99 131,206,063.84 131.206.053.84 LRT 4,633, 118.09 1,922,095.91 1,922,095.91 29,470.32 1,318.69 583.99 6,033.01 8.439.65 11.411.99 118,086.12 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withoking 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23500 State Payroll Takes Payable 23700 SUTA Tax Payable 2000 FICA Employer Withholding 23900 Medicare Employer Withholing 24100 Line of Cred 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable Noncurent A1.2 A1.2 A12 A12 A1.2 A12 A12 A1.2 A12 8.439.65 11.414.99 118,006.12 A1.1 A1.1 A1.1 A1.1 A1.1 A1.1 AL1 A1.1 A11 A1.1 A1.1 A1.1 A1.1 A1.1 A1.1 2,815.47 55,106.86 55,106.86 1,318.69 583.99 10,000,000.00 A12 8,439.65 11.414.99 41,403,000.00 8,439.65 11.414.99 14.403,000.00 A12 A12 A1.2 A12 12,000,000.00 12,000,000.00 Total liberties 14,675,24225 58,537,998.17 58.3799817 OWNER'S EQLITY 39003 Common Stock 390114 Paidin Capital 39005 Retained Eamings A1.11 A1.1 A1.1 8,105,000.00 7,423,000.00 2.219,620.65 A1.2 A1.2 A1.2 8,105,000.00 7,423,000.00 6,590,983.64 8,105,000.00 7.423,000.00 6.590,533.64 121 A2.1 Net Income Total Ormer's Equity 4,371,362.99 22,118,983.64 50,549,082.03 72,668,065.67 50,549,082.03 22,668,065.67 Total Liberties & Equity 36,794225.89 131,205,063.81 - 131,206,063.84 WPE Apollo Shoes, hac Analytical Procedures Common Size come Statement 1281/2017 PB: RB: Acct Account Inge Significant WP Ret 12/31/2016 Audited 12/31/2017 haudited Title SALES REVENUE 40000 Sales 41000 Sales Retums 42000 Warranty Expense A2.1 A2.1 N21 246,172,918.44 14,497,583.20) (1,100,281.48) 102% 2% 0% 242,713,452.88 (11,100,220.89) (1,158,128.47) 105% 5% 1% (3,459,465.56) (6,602,637.69) (57.846.99) 0% 0% 0% 100% Het Sales 240_575,053.76 220,455,103.72 100% (10,119,950.24) COST OF GOODS SOLD 50000 Cost of Goods Sold N21 141,569,221.61 59% 130, 196,645.26 56% (11,372,576.35) ox 2x 0% 0% Total CGS Gross Maryi 0% 0% 2% 2% 0% 59% 41% 141,569,221.61 99,005,832.15 OX 56% 44% 130, 196,645.26 100,258,458.26 (11,372,576.35 1,252,626.11 2x 0% 2% 0% 0% 13% 02 2x 0% 0% 0% 0% -13% X 4,240,263.09 1,036,854.01 210,502.80 528,870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 0% 2% 0% X OPERATING EXPENSES 57500 Freight 60.000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 680.00 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 73000 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense A2.1 A2.1 A2.1 A2.1 A2.1 A21 A21 A2.1 A2.1 A21 AZ1 A2.1 A2.1 A2.1 A2.1 A2.1 A2.1 A21 A21 X 4,312,951.46 897,140.01 218,974.39 31,212,334.17 133,000.00 4,633,33.82 80,495.32 3,605,133.96 1,622,425.99 853,942.65 61,136.04 135,642.99 76,373.78 128,033.21 17,023.27 1,550,989.06 3,000,000.00 2.613,485.87 16,875,315.98 1% 1% 0% (62,688.37) 139,714.00 1,528.41 (30,683,463.73) 313,000.00 87,331.74 18,837.13 1,308,090.49 (1,622,425.99) (817,835.73) (25,633.17) 1,689.19 (23,774.76) (50,229.60) 7.868.55 26,822.79 300,000.00 (1,396,911.87) (678,680.55) -1% 0% 0% 0% ox 0% 0% ox 0% 0% 0% OX 1% 36,106.92 35,562.87 137.332.18 52,599.02 77.813.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16,197,225.43 1% 1% 1% 0% 0% 1% 7% 0% 0% 17% 27% 0% Total Operating Expenses Net Lacome fron Operations 71,997,771.97 27,008,060.18 30% 11% 38.841,610.50 61,416,847.76 (33,156,161.47) 34,408,787.58 -13% 15% 1% 1% 0% 0% 214,312.81 OTHER NCOHE EXPENSE) 45000 Income from Investments 46000 Interest come 47000 Miscellaneous Income 78000 Interest Expense 80000 Loss on Legal Settlement A21 AZ1 A21 A21 N21 1,426,089.31 131,881.46 2,165,000.00 (2,591,736.50) 0% 0% 1% 1% 1,426.689.31 (12,421.35 2,165,000.00 (1,716,736.50) 19,172,000.00 (875,000.00 (19,172,000.00 1% 8 8% 0X 0% 8% O 0X 0% 0% 27% 83 Total Other come Expenses) Het hcome before Tax (19.842,697.19) 7,165, 162.99 1,132,234.27 62,519,082.03 20,974,931.46 55-383.719.04 TAXES 12.11 3% 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State (8,900,000.00) (3,100,000.00 A2.1 (6,515,000.00 (2,671,000.00) (2,365,000.00) 429,000.00) - (2,794,000.00 4371, 162.99 1% 0% 0% 1% 22 4% 1% 1 5% 22 Total Taxes Netcome (12,000,000.00) 50,549,082.03 19,215,000.00 46,177,719.04 0% 4% 20% WPE Apollo Shoes, loc Worting Trial Balance Common Size Balance Sheet 1281/2017 PB: RB: Acct Siglicant Account Title WP Ret 1281/2016 Audited 12/31/2017 Lhandited ASSETS 0% X 1,987.28 198,116.52 0% 1x 2,275.23 557,125.92 287.95 359,0-19.40 X X 0% 3% 39% 3,644,958.13 16,410,902.71 X X X 1% X 3,645,599.15 51,515,259.98 1,250,000.00 (1,239,019.75) 67,724,527.50 (846,000.00) 3,424,213.78 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 45% 0% 3% 51% 8% 2x X (1,262,819.88) 18,825,215.24 (3,012,000.00) 743,314.38 200,000.00 7,406.82 600,641.02 35,104,357.27 1,250,000.00 23,810.13 48,899,322.26 2,165,000.00 2,680,899.40 (200,000.00) 1,133.18 X 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alowance for Doubtful Accounts 12000 Hrventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Cument Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Olice Furniture 17000 Accum. Depreciation 19000 livestments 19900 Other Noncurrent Assets 1% 3% X 1% X 8,540.00 0% 117.000.00 ox 2x 2x 117,000.00 623,915.92 433,217.10 (163,500.00) 572,691.18 53,840.59 674,313.92 2,929,097.13 (619,500.00) 1,998,780.39 53,840.59 50,408.00 2,495,890.03 (446,000.00 1,426,189.31 A22 A22 2* A22 0 0% 2x ox 0% 0% 0% 100% 0% 02 0% 100% Total Assets 3,794, 225.89 131,206,063.84 94,411,837.95 LABUTES 4,633, 118.09 1,922,095.91 1% 0% (2,711,022. 18) 13% 0% -11% 0% 0% 29,470.32 1,318.69 583.99 6,033.01 (29,470.32) 7.120.96 10,831.00 112,653.11 8,439.65 11,414.99 118,196.12 0% OS 0% 0% 0% OX 0% 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withhoking 23:50 Medicare Withhoking 23400 Federal Payroll Taxes Payable 2200 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholing 239.00 Medicare Employer Withholding 24100 Line of Cheit 24200 Current Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurent A22 A22 A22 N22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 2,815.47 55,106.86 0% 52,291.39 0% 0% 0% 0% 1,318.69 583.99 10,000,000.00 8,439.65 11,414.99 44,403,000.00 0% 0% 34% 0X 7,120.96 10,831.00 34,403,000.00 0% 27% 0% 0X 0% 12,000,000.00 12,000,000.00 0% 9% 0% 0% 9% 0% 0% 0X 0 0% 0 0% 45% Total Liabilities 14,675 24225 40% 58,537,998.17 43.862,755.92 -16% OWNER'S EQUTY 39013 Common Stock 39.014 Paid in Capital 39005 Retained Eamings A22 A22 A22 8,105,000.00 7,423,000.00 2,219,620.65 22% 20% 6% 8,105,000.00 7,423,000.00 6,590,983.64 6% 6% -15% -1% 4,371,362.99 5% 0% xxxx 0% 02 A22 27% Net Income Total Owner's Equity 4,371,362.99 22,118,983.64 12 6 0% 50.549.082.03 72,668,065.67 39% 55% 46,177,719.14 50,519,082.03 Total Liabities & Equity 36,794 225.89 100% 131,206,063.84 100% 94,411,837.95 0% WP# A33 Apollo Shoes, hoc Analytical Procedures Selected Ratios 1281/2017 PB: HN RB: DW Date 923/2018 9/24/2018 Audited 1281/2016 Theaudited 12/31/2017 Percentage Change Asset Tumover Current Ratio Days Sales in AR Days Salles in hventory Debt Ratio Debt Equity Ratio Liability Tumover 6.54 2.40 24.90 48.54 0.40 0.66 16.39 1.76 2.71 81.59 189.86 0.45 0.81 3.94 -73.14% 13.05% 227.69% 291.18% 11.86% 21.42% -75.98% Net Working Capital 20,481,828.95 79,514,533.64 288.17% WPE Apollo Shoes, hec Adresting Journal Entries For the Year Ended 1281/2017 PB: RB: AE Acct. Acco Debits Credits 0.00 0.00 Apollo Shoes, ac Audit Plan -Cash For Year Ended 12/31/2017 PB WP Ret 11.1 Chert B21 B22 Chert Step 5 Procedures Notes Prepare Cash Lead Schedule for year end Transfer the audited balances of 2016 and the unaudited balances of 2017 to the lead schedule. Obtain standard Bank Confirmation from client's Prepare Bank Reconciliation for material accounts Obtain Cutof Bank Statement from client's bank Obtain Deposit Sips from client. Match the deposit slips with the cutof bank Deposits shown in the cutof bank statement but not in the deposit saps suggest that statement these deposits were in transit and the bank was not aware of them at year end. Therefore they should be added to the year end bank confirmation balance. Obtain a list of Outstanding Checks from client. Match the outstanding checks with the cutof bank Checks issued but not cashed a year end suggest that these checks were in transit statement and the bank was not aware of them at year end. Therefore they should be subtracted from the year end bank confirmation balance. Reconcile the bank balance reported in the bank confirmation with the balance reported in the trial balance. Client Client B23 WPE Apollo Shoes, hac Cash Lead Schedule For Year Ended 12/31/2017 PB: RB: Acements Audited Bakance 12/31/2016 audited Bakance 12/31/2017 Audited Bakancel WP 1281/2017 Ref Acott Accot Title Debit Credit ALE 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account A1.1 A1.1 A11 A1.1 A12 A12 A12 A12 0.00 0.00 0.00 0.00 0.00 0.0.0 0.00 Legend Column footed Colum and row footed Agreed with Trial Balance IB WP B2 Apollo Shoes, hec Bart Recondition For Year Ended 1281/2017 Date PB: RB: Regalar Checting Account (604-17-526-5) Unadjusted Book Balance Bank Adjustments Amount to Balance Adssted Book Bakance 0.00 Balance per Bank Confirmation Add Deposits in Transit Deduct Outstanding Checks Adested Bank Balance B1.1 B22 B23 0.00 Adjuredited boolt, bake and adjusted bam balkmce should really become me Apollo Shoes, Inc. is an audit case designed to introduce you to the entire audit process, from planning the engagement to drafting the final report. You are to assume the role of a staff auditor at Anderson, Olds, and Watershed (AOW) CPAs and work on the financial audit of a client, Apollo Shoes, Inc. This assignment focuses on the planning process of the audit. This assignment contains various communications from the Darlene Wardlaw, Engagement Manager at AOW CPAs. Each communication contains certain assignment requirements highlighted in bold. The documents mentioned in the Attachments section of a communication are available in the Content area of D2L in Apollo Shoes module. The information in this assignment is sequential in nature. In other words, pay close attention to information disclosed early in the audit (for example, in the Board of Directors' meeting minutes) as it may play a role in subsequent audit work contained in other assignments. Limitations of the case: While the case is as realistic as possible, you are unable to follow up directly with client personnel. Therefore, you will have to rely on evidence provided to you through D2L. In an actual audit, you would be able to inquire, observe, and otherwise follow-up on any questions that you have until you feel comfortable relying on the evidence. Also, to make sure that the case can be completed in a reasonable amount of time, most of the audit sampling is already done for you. Understand that audit sampling plays a large role in actual audit practice and you might have to be directly involved with the sampling procedures. Cash Audit You are to conduct a cash audit of Apollo Shoes, Inc. The cash audit is designated with the B series. So, any document starting with B is a primary document for cash audit You will be working on the following workpapers during your audit of cash: B Cash - Audit Plan B1 Cash - Lead Schedule B1.1 Bank Confirmation B2 Bank Reconciliation B2.1 Cutoff Bank Statement B2.2 Deposit slips B2.3 Outstanding checks The Assignment 3 - TEMPLATE.xlsx posted on D2L includes an audit plan for cash (worksheet B). An actual audit plan for cash is a lot more detailed. However, for the sake of simplicity, we will be using a much basic audit plan. This assignment will introduce you to examining evidence so pay close attention to detail. Mastery of bank reconciliation will prove to be very beneficial in this assignment You will also be making one adjusting journal entry in this assignment. Use the Assignment 3 - TEMPLATE to record your audit work and submit it to the dropbox by the due date. Date: 19 JAN 2018 15:37:42 +0000 From: "Darlene Wardlay" Subject: Audit of Cash Attachments: >, >, >, > I want you to start with the cash audit. We have received the Bank Confirmation (WP ref# B1.1) and the January 2018 cutoff bank statement (WP ref# B2.1) directly from Apollo's bank. We have also received the deposits slips for deposits made immediately after the year end (WP ref# B2.2) and list of outstanding checks at the year end (WP ref# 2.3) from the client. These documents should be sufficient for creating Bank Reconciliation (WP ref# B2). Begin by preparing a cash lead schedule so that we know which accounts are significant and therefore while need to be audited. After completing the cash lead schedule, start auditing the regular checking account by comparing the book balance in the lead schedule with the balance provided in the bank confirmation. Obviously there will be differences due to deposits in transit and outstanding checks. So prepare a bank reconciliation to adjust the book balance with any deposits or withdrawals the client might not have known at year end, and adjust the bank balance with any deposits or withdrawals the bank might not have known at year end. FYI, while auditing the accounts payable, I came across an account that was paid but not recorded in the books. This means that the cash might be overstated. See if you can find any check in the 2018 cutoff bank statement that was not recorded as an outstanding check at the 2017 year end. If you find a missing outstanding check, please post an adjusting entry accordingly in workpaper AJE and make adjustments in the cash lead schedule (B1) as well as the working trial balance (A2.1 & A2.2) Your ability to properly reference your workpapers is critical for me to understand where you got the information from and to which other workpapers did the information go to. The way workpapers are referenced in auditing is based on the concepts of tracing and vouching. Preceding workpapers are referenced towards the left and succeeding workpapers are referenced towards the right. Basically, a reference on the left shows where the information is coming from and a reference on the right shows where the information is going. For example, when preparing the Bank Reconciliation, the Balance per Bank Confirmation should have B1.1 referenced towards the left of the amount to show other auditors that the information is coming from the Bank Confirmation, in the Bank Confirmation, the same amount should have B2 referenced towards the right to show other auditors that the amount is going to the Bank Reconciliation Talk to you soon. DW WPE A11 Apollo Shoes, hec Preclosing Trial Balance (audited) As of the year end December 31, 2016 PB: HN RB: DW AccoD Account Description Debit Amoet Credit Amoet 1,987.28 198,116.52 3,44,958.13 16,410,902.71 1,262,819.88 18,825,205.24 3,012,000.00 743,314.38 200.000.00 7,406.82 117,000.00 623,915.92 433,217.10 163,500.00 572,691.18 53,840.59 4,633,118.09 29,470.32 1,318.69 583.99 6,033.01 2,815.47 1,318.69 583.99 10,000,000.00 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alowance for Doubtft Accounts 12000 Inventory - Spotlight 12300 Reserve for hventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Cument 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Ofice Fumiture 17000 Accum. Depreciation 19000 Westments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholfing 23400 Federal Payroll Taxes Payable 2300 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23900 FICA Employer Withholfing 239.00 Medicare Employer Withholding 24100 Line of Credi 24200 Cument Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurrent 39003 Common Stock 39014 Paid in Capital 39005 Retained Eamings 40000 Sales 41000 Sales Retums 42000 Warranty Expense 45000 Income from Investments 46000 hterest Income 47000 Miscellaneous Income 50100 Cost of Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 7200 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 809Loss on Legal Settlement 8,105,000.00 7,423,000.00 2,219,620.65 246,172,918.44 4,497,583.20 1,100,281.48 214,312.81 141,569,221.61 4,312,951.46 897,140.01 218,974.39 31,212,334.17 133,000.00 4,633,383.82 80,495.32 3,615, 133.96 1,622,425.99 853,942.65 61,136.14 135.642.99 76,373.78 128,033.21 17.023.27 1,550,989.06 3,000,000.00 2,603,485.87 16,875,315.98 875,000.00 2,365,000.00 429,000.00 19,172,000.00 283,238,404.03 2 83,238,404.03 WP A12 Apollo Shoes, ac Preclosing Trial Balance ( dited) As of the year end December 31, 2017 PB: HN RB: DW AccoD Account Description Debit Amount Credit Amoet 2,275.23 557,125.92 3,645,599.15 51,515,259.98 1,250,000.00 1,239,019.75 67,724,527.50 846,000.00 3,424,213.78 8,540.00 117,000.00 674,313.92 2,929,097.13 619,500.00 1,948,780.39 53,840.59 1,922,095.91 8,439.65 11,414.99 118,686.12 55,106.86 8,439.65 11,414.99 44,403,000.00 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts 12000 nentory 12300 Reserve for hventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Cument 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Ofice Fumiture 17000 Accum. Depreciation 19000 Westments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholfing 23400 Federal Payroll Taxes Payable 2300 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23900 FICA Employer Withholfing 239.00 Medicare Employer Withholding 24100 Line of Credi 24200 Cument Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurrent 39003 Common Stock 39014 Paid in Capital 39005 Retained Eamings 40000 Sales 41000 Sales Retums 42000 Warranty Expense 45000 Income from Investments 46000 hterest Income 47000 Miscellaneous Income 50100 Cost of Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 7200 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 809Loss on Legal Settlement 12,000,000.00 8,105,000.00 7,423,000.00 6,590,983.64 242,713,452.88 11,100,220.89 1,158,128.47 1,426,089.31 131,881.46 2,165,000.00 130.196,645.26 4,240,263.09 1,036,854.01 210.502.80 528.870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 36,106.92 35,512.87 137,332.18 52,599.02 77.813.61 24,891.82 1,577,811.85 3,300,000.00 1,216,574.00 16, 197,225.43 2,591,736.50 8,900,000.00 3,100,000.00 329,788,915.21 329,788,915.21 WPE Apollo Shoes, Inc. Working Til Bakance Income Statement 12/31/2017 RB Acct. Adestruents Account Title WP Ret 12/01/2016 Audited WP Ret 1231/2017 Uudited 12/31/2017 Audited AE SALES REVENLE 40000 Sales 41000 Sales Retums 42000 Warranty Expense A11 A11 AL1 246,172,918.44 (4,497,583.20) (1,100,281.48) M12 A12 A12 242,713,452.88 (11,100,220.89) (1,158,128.47) 242,713,452.88 (11,100.220.89) (1,158,128 47 Net Sales 240,575,053.76 230,455, 103.52 230,455,103.52 COST OF GOODS SOLD 50000 Cast of Goods Sold A11 141,569,221.61 | A1.2 130, 196,645.26 130, 196,645.26 Total CGS Gross Mary 141,569,221.61 99,005,832.15 130, 196,645.26 100,258,458.26 130, 196,645 26 100,258,458.26 A11 A11 A11 A11 A1.1 A11 AL1 AL1 A1.1 AL1 A11 AL1 4,240,263.09 1,036,854.01 210,502.80 528,870.14 446,000.00 4,720,715.56 99,332.45 4,913,224.45 OPERATING EXPENSES 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Prufessional Expense 67000 Bad Debt Expense GOOD Insurance Expense 70000 Maintenance Expense 70100 Uhies 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 73000 Pension Profit Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense 4,240,263.09 1,036,854.01 210,502.80 528.870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 4,302,951.46 897.140.01 208,974.39 31,212,331.17 133,000.00 4,633, 23.02 80,495.32 3,605,133.96 1,622,425.99 853,942.65 61,136.04 135,642.99 76,373.78 128,033.21 17.023 27 1,550,989.06 3,000,000.00 2,603,485.87 16,875,305.98 A12 A12 A12 A12 A12 A12 A12 A1.2 A12 A12 A12 A1.2 A12 M12 A12 A12 A12 M12 A12 36,106.92 35,502.87 137 132.18 52,599.02 77,803.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16, 197,225.43 36,106.92 35,502.87 137,332.18 52,599.02 77,803.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16,197,225.43 A11 AL1 AL1 Total Operating Expenses Net lacome from Operations 71,997,771.97 27,008,060.18 38,811,610.50 61,416,847.76 38,841,610.50 61,416,847.76 204, 302.81 OTHER NCOME EXPENSE) 45000 Income from investments 46000 Interest Income 47000 Miscellaneous Income 78000 Interest Expense 80000 Loss on Legal Settlement AL1 A1.1 AL1 AL1 A11 A1.2 A12 A12 A1.2 A1.2 1,426,089.31 131,881.46 2,166,000.00 (2,591,736.50) 1,426,089.31 131,881.46 2,166,000.00 (2,591,736.50) (875,000.00) (19,172,000.00) Total Other Lacome Expenses) Net Lecome before Tax (19,842,697.19 7,165, 162.99 1,132,234.27 2,549,082.03 1,132,231.27 62,549,082.03 TAXES 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State AL1 AL1 (2,365,000.00) (429,000.00) A1.2 A12 (8,900,000.00) (3.100,000.00) (8,900,000.00) (3.100.000.00) Total Taxes Net lecome (2.744,000.00) 4,371, 362.99 (12,000,000.00) 50,549,082.03 A22 (12,000,000.00) 50,519,082.03 22 WPE Apollo Shoes, hec Working Trial Balance Bakance Sheet 1231/2017 PB: RB Acc. A stments Account Title WP Ret 1231/2016 Audited WP Ret 12/31/2017 audited 12/31/2017 Audited ASSETS 1,987.28 198,116.52 2,275.23 557,125.92 2,275.23 557,125.92 3,041,958.13 16,410,902.71 A1.1 A1.1 A1.1 A1.1 A1.1 A11 A1.1 A1.1 A1.1 A1.1 A1.1 A11 A11 AL1 A1.1 A1.1 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10000 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alkuwance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for entory Obsolescence 14100 Prepaid insurance 14200 Prepaid Rent 14300 Ofice Supplies 14400 Nates Receivable Current 1700 Other Current Assets 15000 Land 15100 Buklings and Land Improvements 15200 Machinery, Equipment, Olice Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets (1,262,819.88) 18.825,205 24 (3.012,000.00) 743,314.338 200,000.00 7,406.82 A12 A1.2 A1.2 A12 A1.2 A12 A1.2 A12 A12 A12 A1.2 A12 A12 A1.2 A12 3,615,599.15 51,515,259.90 1,250,000.00 (1,239,009.75) 67.724,527.50 (816,000.00) 3,424,213.78 3,615,599.15 51,515,259,98 1,250,000.00 (1,229,009.75) 67.724,527.50 (846,000.00) 3,424,213.78 8,540.00 8,510.00 117.000.00 623,905.92 413,217.10 (163,500.00) 572,691.08 53,840.59 A12 117,000.00 674,313.92 2,929,097.13 (609,500.00 1,998,780.39 53,840.59 117,000.00 674,313.92 2,929,097.13 (609,500.00 1,998,780.39 53,840.59 Total Assets 36,794,7%.89 15794 TX 99 131,206,063.84 131.206.053.84 LRT 4,633, 118.09 1,922,095.91 1,922,095.91 29,470.32 1,318.69 583.99 6,033.01 8.439.65 11.411.99 118,086.12 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withoking 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23500 State Payroll Takes Payable 23700 SUTA Tax Payable 2000 FICA Employer Withholding 23900 Medicare Employer Withholing 24100 Line of Cred 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable Noncurent A1.2 A1.2 A12 A12 A1.2 A12 A12 A1.2 A12 8.439.65 11.414.99 118,006.12 A1.1 A1.1 A1.1 A1.1 A1.1 A1.1 AL1 A1.1 A11 A1.1 A1.1 A1.1 A1.1 A1.1 A1.1 2,815.47 55,106.86 55,106.86 1,318.69 583.99 10,000,000.00 A12 8,439.65 11.414.99 41,403,000.00 8,439.65 11.414.99 14.403,000.00 A12 A12 A1.2 A12 12,000,000.00 12,000,000.00 Total liberties 14,675,24225 58,537,998.17 58.3799817 OWNER'S EQLITY 39003 Common Stock 390114 Paidin Capital 39005 Retained Eamings A1.11 A1.1 A1.1 8,105,000.00 7,423,000.00 2.219,620.65 A1.2 A1.2 A1.2 8,105,000.00 7,423,000.00 6,590,983.64 8,105,000.00 7.423,000.00 6.590,533.64 121 A2.1 Net Income Total Ormer's Equity 4,371,362.99 22,118,983.64 50,549,082.03 72,668,065.67 50,549,082.03 22,668,065.67 Total Liberties & Equity 36,794225.89 131,205,063.81 - 131,206,063.84 WPE Apollo Shoes, hac Analytical Procedures Common Size come Statement 1281/2017 PB: RB: Acct Account Inge Significant WP Ret 12/31/2016 Audited 12/31/2017 haudited Title SALES REVENUE 40000 Sales 41000 Sales Retums 42000 Warranty Expense A2.1 A2.1 N21 246,172,918.44 14,497,583.20) (1,100,281.48) 102% 2% 0% 242,713,452.88 (11,100,220.89) (1,158,128.47) 105% 5% 1% (3,459,465.56) (6,602,637.69) (57.846.99) 0% 0% 0% 100% Het Sales 240_575,053.76 220,455,103.72 100% (10,119,950.24) COST OF GOODS SOLD 50000 Cost of Goods Sold N21 141,569,221.61 59% 130, 196,645.26 56% (11,372,576.35) ox 2x 0% 0% Total CGS Gross Maryi 0% 0% 2% 2% 0% 59% 41% 141,569,221.61 99,005,832.15 OX 56% 44% 130, 196,645.26 100,258,458.26 (11,372,576.35 1,252,626.11 2x 0% 2% 0% 0% 13% 02 2x 0% 0% 0% 0% -13% X 4,240,263.09 1,036,854.01 210,502.80 528,870.44 446,000.00 4,720,715.56 99,332.45 4,913,224.45 0% 2% 0% X OPERATING EXPENSES 57500 Freight 60.000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 680.00 Insurance Expense 700.00 Maintenance Expense 70100 Urties 70110 Phone 70120 Postal 71000 Miscellaneous Ofice Expense 72000 Payroll Tax Exp 73000 Pension Profi-Sharing Plan Ex 74000 Rent or Lease Expense 77500 Administrative Wages Expense A2.1 A2.1 A2.1 A2.1 A2.1 A21 A21 A2.1 A2.1 A21 AZ1 A2.1 A2.1 A2.1 A2.1 A2.1 A2.1 A21 A21 X 4,312,951.46 897,140.01 218,974.39 31,212,334.17 133,000.00 4,633,33.82 80,495.32 3,605,133.96 1,622,425.99 853,942.65 61,136.04 135,642.99 76,373.78 128,033.21 17,023.27 1,550,989.06 3,000,000.00 2.613,485.87 16,875,315.98 1% 1% 0% (62,688.37) 139,714.00 1,528.41 (30,683,463.73) 313,000.00 87,331.74 18,837.13 1,308,090.49 (1,622,425.99) (817,835.73) (25,633.17) 1,689.19 (23,774.76) (50,229.60) 7.868.55 26,822.79 300,000.00 (1,396,911.87) (678,680.55) -1% 0% 0% 0% ox 0% 0% ox 0% 0% 0% OX 1% 36,106.92 35,562.87 137.332.18 52,599.02 77.813.61 24,891.82 1,577,811.85 3,300,000.00 1,206,574.00 16,197,225.43 1% 1% 1% 0% 0% 1% 7% 0% 0% 17% 27% 0% Total Operating Expenses Net Lacome fron Operations 71,997,771.97 27,008,060.18 30% 11% 38.841,610.50 61,416,847.76 (33,156,161.47) 34,408,787.58 -13% 15% 1% 1% 0% 0% 214,312.81 OTHER NCOHE EXPENSE) 45000 Income from Investments 46000 Interest come 47000 Miscellaneous Income 78000 Interest Expense 80000 Loss on Legal Settlement A21 AZ1 A21 A21 N21 1,426,089.31 131,881.46 2,165,000.00 (2,591,736.50) 0% 0% 1% 1% 1,426.689.31 (12,421.35 2,165,000.00 (1,716,736.50) 19,172,000.00 (875,000.00 (19,172,000.00 1% 8 8% 0X 0% 8% O 0X 0% 0% 27% 83 Total Other come Expenses) Het hcome before Tax (19.842,697.19) 7,165, 162.99 1,132,234.27 62,519,082.03 20,974,931.46 55-383.719.04 TAXES 12.11 3% 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State (8,900,000.00) (3,100,000.00 A2.1 (6,515,000.00 (2,671,000.00) (2,365,000.00) 429,000.00) - (2,794,000.00 4371, 162.99 1% 0% 0% 1% 22 4% 1% 1 5% 22 Total Taxes Netcome (12,000,000.00) 50,549,082.03 19,215,000.00 46,177,719.04 0% 4% 20% WPE Apollo Shoes, loc Worting Trial Balance Common Size Balance Sheet 1281/2017 PB: RB: Acct Siglicant Account Title WP Ret 1281/2016 Audited 12/31/2017 Lhandited ASSETS 0% X 1,987.28 198,116.52 0% 1x 2,275.23 557,125.92 287.95 359,0-19.40 X X 0% 3% 39% 3,644,958.13 16,410,902.71 X X X 1% X 3,645,599.15 51,515,259.98 1,250,000.00 (1,239,019.75) 67,724,527.50 (846,000.00) 3,424,213.78 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 45% 0% 3% 51% 8% 2x X (1,262,819.88) 18,825,215.24 (3,012,000.00) 743,314.38 200,000.00 7,406.82 600,641.02 35,104,357.27 1,250,000.00 23,810.13 48,899,322.26 2,165,000.00 2,680,899.40 (200,000.00) 1,133.18 X 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Alowance for Doubtful Accounts 12000 Hrventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Cument Assets 15000 Land 15100 Buildings and Land Improvements 15200 Machinery, Equipment, Olice Furniture 17000 Accum. Depreciation 19000 livestments 19900 Other Noncurrent Assets 1% 3% X 1% X 8,540.00 0% 117.000.00 ox 2x 2x 117,000.00 623,915.92 433,217.10 (163,500.00) 572,691.18 53,840.59 674,313.92 2,929,097.13 (619,500.00) 1,998,780.39 53,840.59 50,408.00 2,495,890.03 (446,000.00 1,426,189.31 A22 A22 2* A22 0 0% 2x ox 0% 0% 0% 100% 0% 02 0% 100% Total Assets 3,794, 225.89 131,206,063.84 94,411,837.95 LABUTES 4,633, 118.09 1,922,095.91 1% 0% (2,711,022. 18) 13% 0% -11% 0% 0% 29,470.32 1,318.69 583.99 6,033.01 (29,470.32) 7.120.96 10,831.00 112,653.11 8,439.65 11,414.99 118,196.12 0% OS 0% 0% 0% OX 0% 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withhoking 23:50 Medicare Withhoking 23400 Federal Payroll Taxes Payable 2200 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholing 239.00 Medicare Employer Withholding 24100 Line of Cheit 24200 Current Portion Long-Term Debt 24700 Other Cument Liabities 27000 Notes Payable Noncurent A22 A22 A22 N22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 A22 2,815.47 55,106.86 0% 52,291.39 0% 0% 0% 0% 1,318.69 583.99 10,000,000.00 8,439.65 11,414.99 44,403,000.00 0% 0% 34% 0X 7,120.96 10,831.00 34,403,000.00 0% 27% 0% 0X 0% 12,000,000.00 12,000,000.00 0% 9% 0% 0% 9% 0% 0% 0X 0 0% 0 0% 45% Total Liabilities 14,675 24225 40% 58,537,998.17 43.862,755.92 -16% OWNER'S EQUTY 39013 Common Stock 39.014 Paid in Capital 39005 Retained Eamings A22 A22 A22 8,105,000.00 7,423,000.00 2,219,620.65 22% 20% 6% 8,105,000.00 7,423,000.00 6,590,983.64 6% 6% -15% -1% 4,371,362.99 5% 0% xxxx 0% 02 A22 27% Net Income Total Owner's Equity 4,371,362.99 22,118,983.64 12 6 0% 50.549.082.03 72,668,065.67 39% 55% 46,177,719.14 50,519,082.03 Total Liabities & Equity 36,794 225.89 100% 131,206,063.84 100% 94,411,837.95 0% WP# A33 Apollo Shoes, hoc Analytical Procedures Selected Ratios 1281/2017 PB: HN RB: DW Date 923/2018 9/24/2018 Audited 1281/2016 Theaudited 12/31/2017 Percentage Change Asset Tumover Current Ratio Days Sales in AR Days Salles in hventory Debt Ratio Debt Equity Ratio Liability Tumover 6.54 2.40 24.90 48.54 0.40 0.66 16.39 1.76 2.71 81.59 189.86 0.45 0.81 3.94 -73.14% 13.05% 227.69% 291.18% 11.86% 21.42% -75.98% Net Working Capital 20,481,828.95 79,514,533.64 288.17% WPE Apollo Shoes, hec Adresting Journal Entries For the Year Ended 1281/2017 PB: RB: AE Acct. Acco Debits Credits 0.00 0.00 Apollo Shoes, ac Audit Plan -Cash For Year Ended 12/31/2017 PB WP Ret 11.1 Chert B21 B22 Chert Step 5 Procedures Notes Prepare Cash Lead Schedule for year end Transfer the audited balances of 2016 and the unaudited balances of 2017 to the lead schedule. Obtain standard Bank Confirmation from client's Prepare Bank Reconciliation for material accounts Obtain Cutof Bank Statement from client's bank Obtain Deposit Sips from client. Match the deposit slips with the cutof bank Deposits shown in the cutof bank statement but not in the deposit saps suggest that statement these deposits were in transit and the bank was not aware of them at year end. Therefore they should be added to the year end bank confirmation balance. Obtain a list of Outstanding Checks from client. Match the outstanding checks with the cutof bank Checks issued but not cashed a year end suggest that these checks were in transit statement and the bank was not aware of them at year end. Therefore they should be subtracted from the year end bank confirmation balance. Reconcile the bank balance reported in the bank confirmation with the balance reported in the trial balance. Client Client B23 WPE Apollo Shoes, hac Cash Lead Schedule For Year Ended 12/31/2017 PB: RB: Acements Audited Bakance 12/31/2016 audited Bakance 12/31/2017 Audited Bakancel WP 1281/2017 Ref Acott Accot Title Debit Credit ALE 10100 Cash on Hand 10200 Regular Checking Account 10300 Payrol Checking Account 10400 Savings Account A1.1 A1.1 A11 A1.1 A12 A12 A12 A12 0.00 0.00 0.00 0.00 0.00 0.0.0 0.00 Legend Column footed Colum and row footed Agreed with Trial Balance IB WP B2 Apollo Shoes, hec Bart Recondition For Year Ended 1281/2017 Date PB: RB: Regalar Checting Account (604-17-526-5) Unadjusted Book Balance Bank Adjustments Amount to Balance Adssted Book Bakance 0.00 Balance per Bank Confirmation Add Deposits in Transit Deduct Outstanding Checks Adested Bank Balance B1.1 B22 B23 0.00 Adjuredited boolt, bake and adjusted bam balkmce should really become me