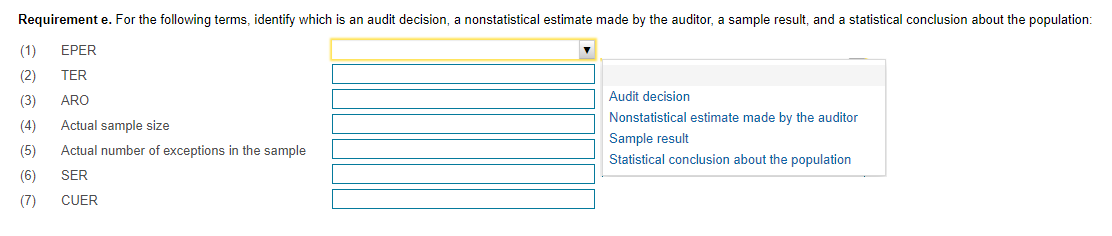

Auditing

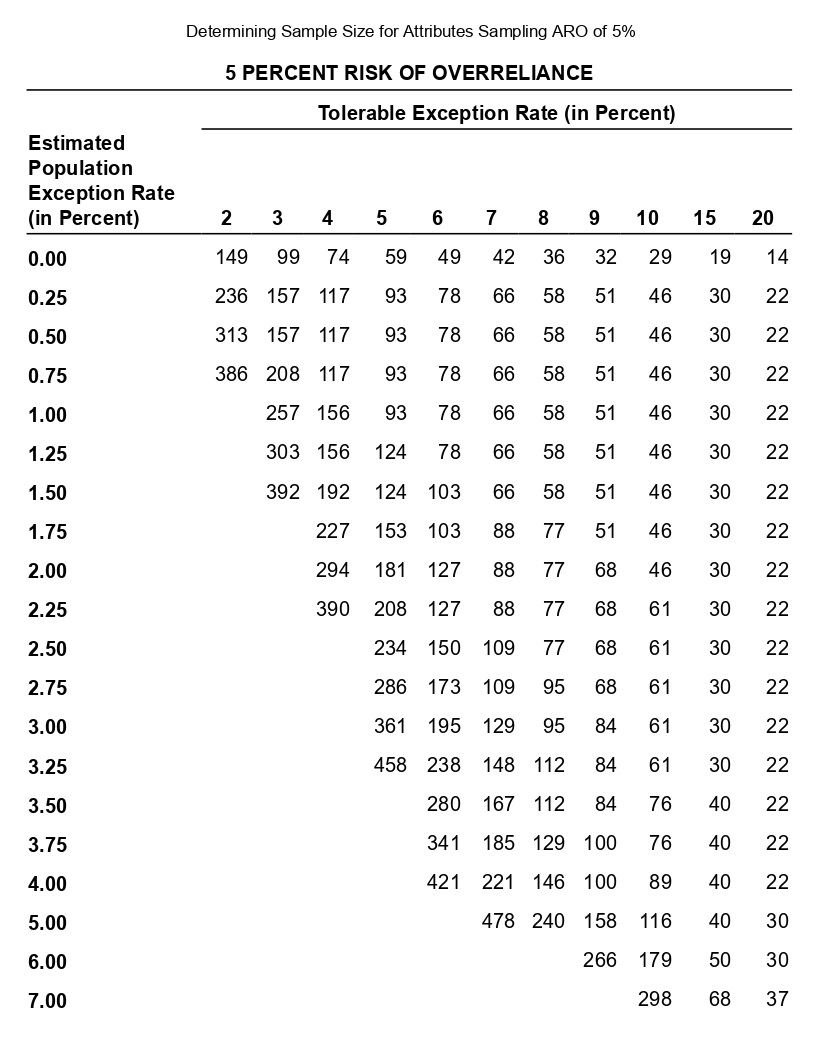

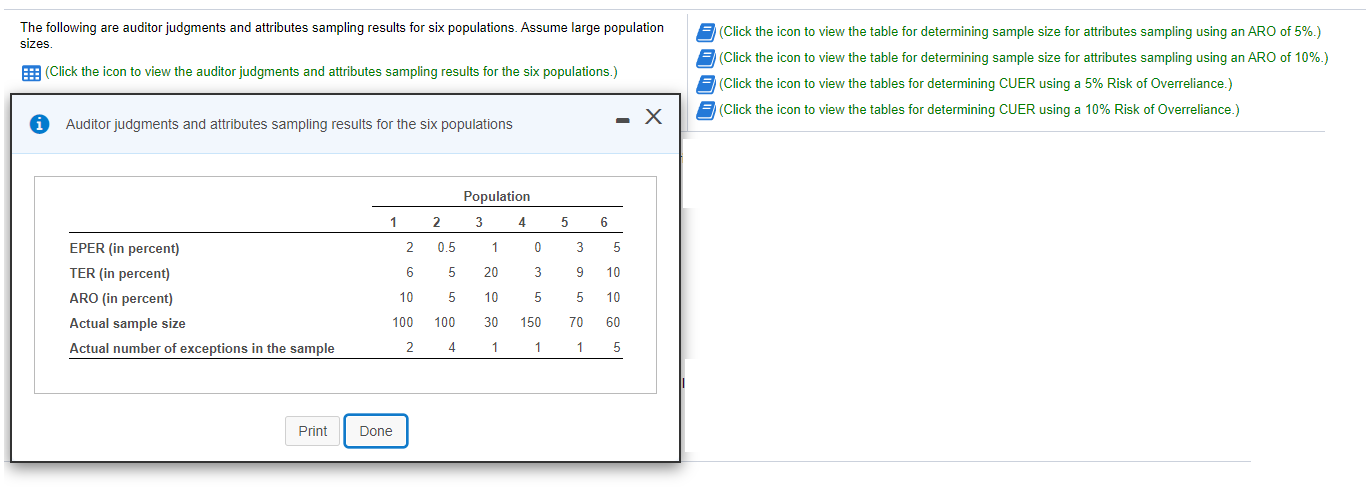

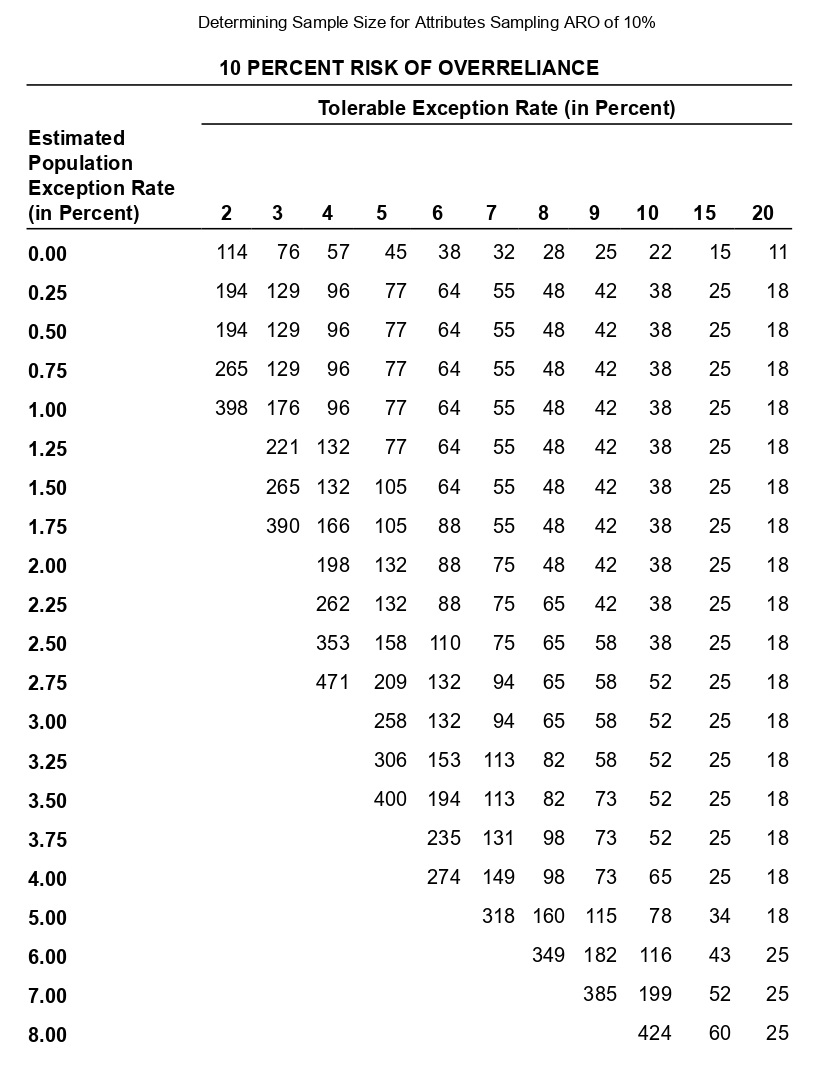

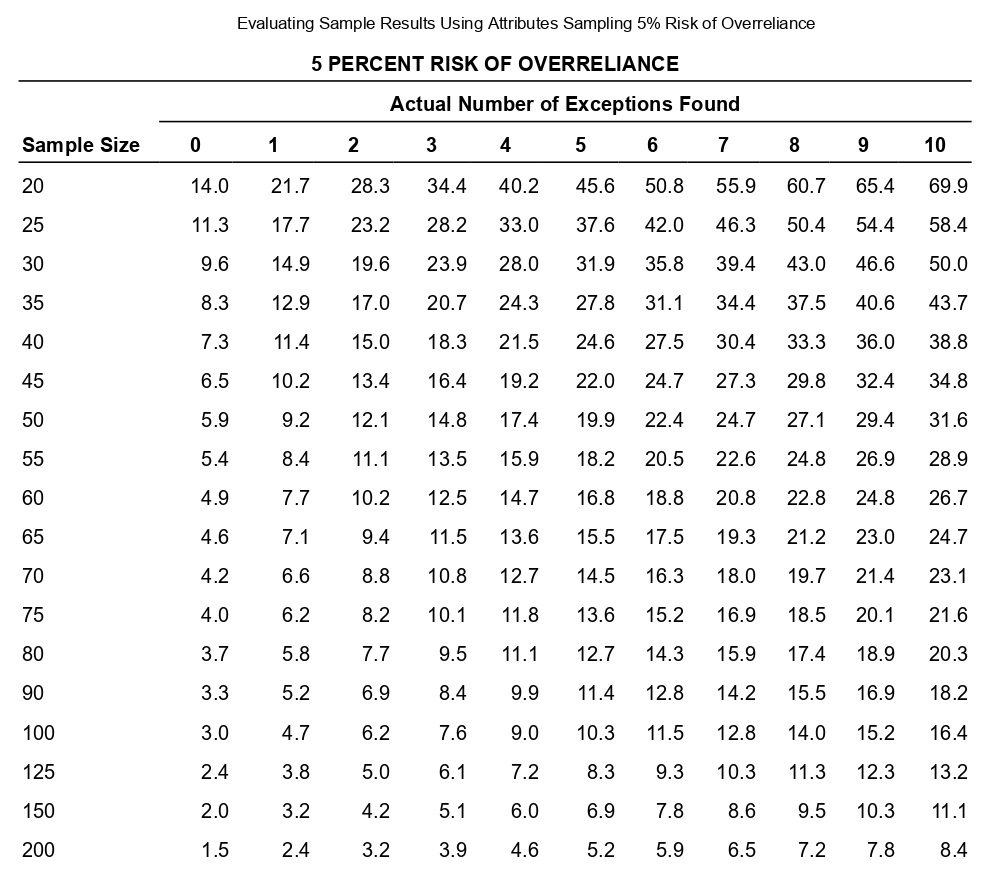

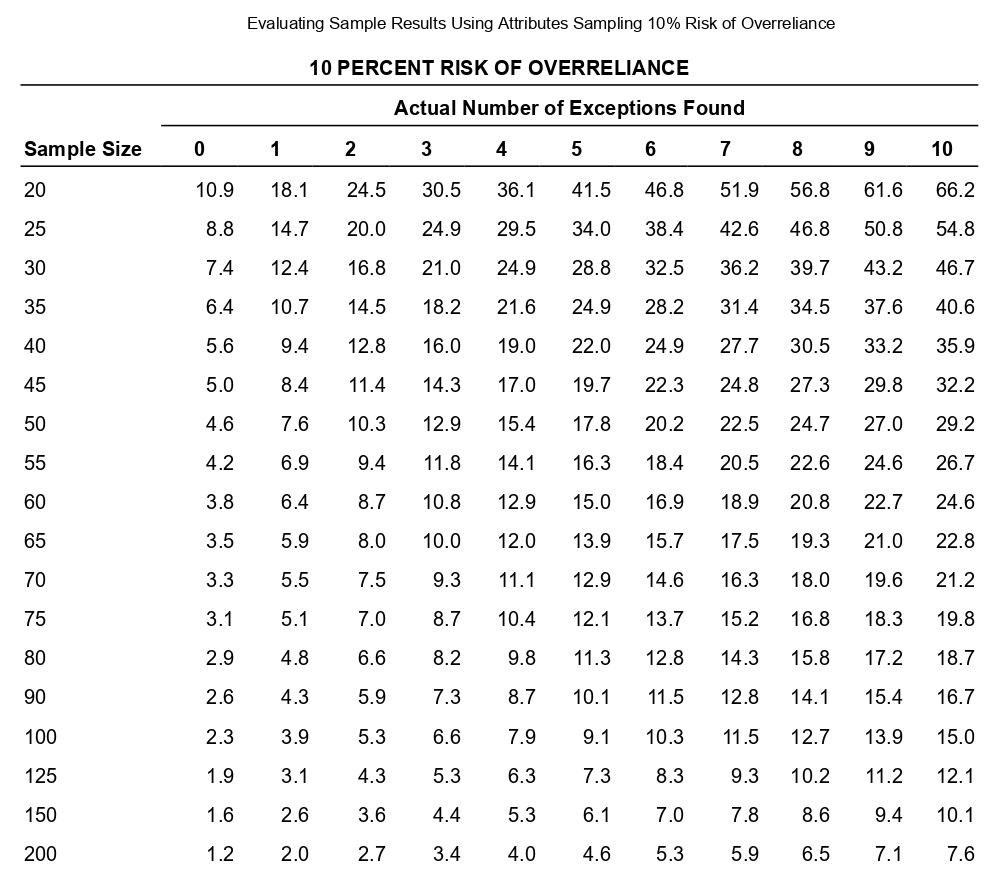

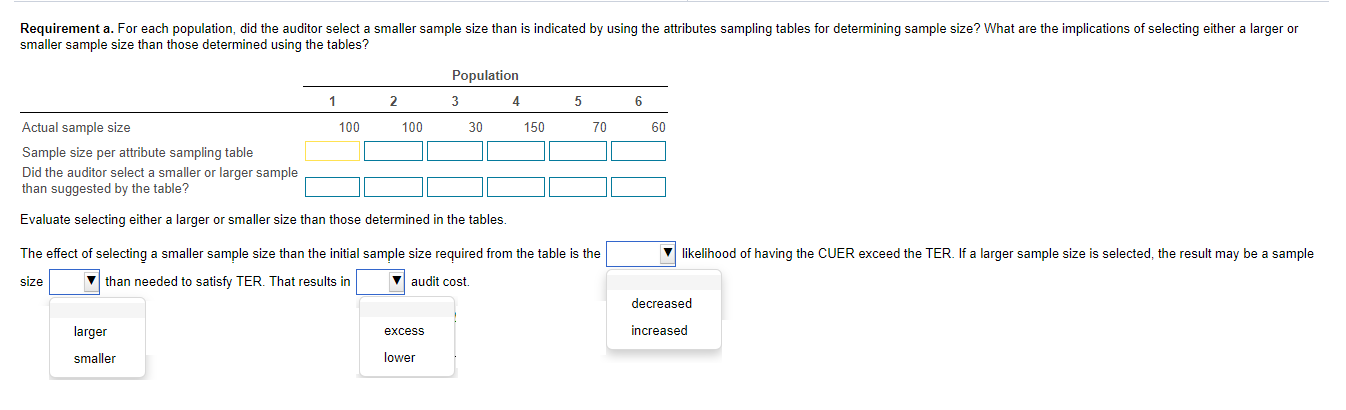

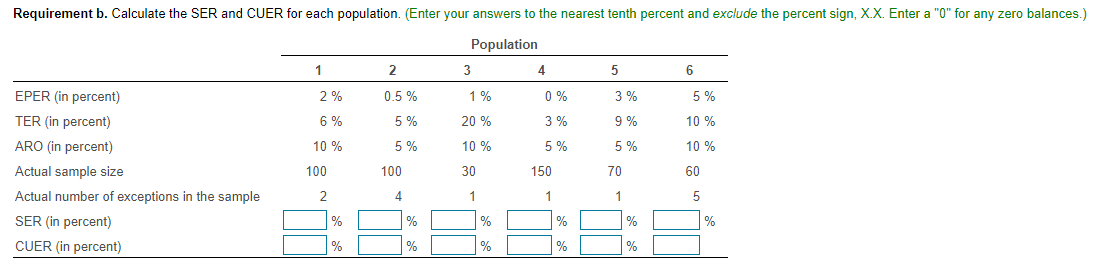

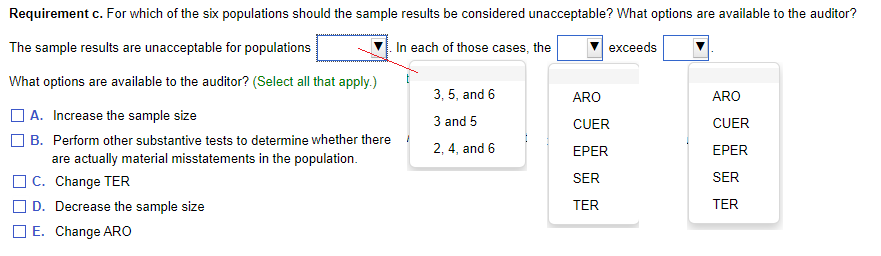

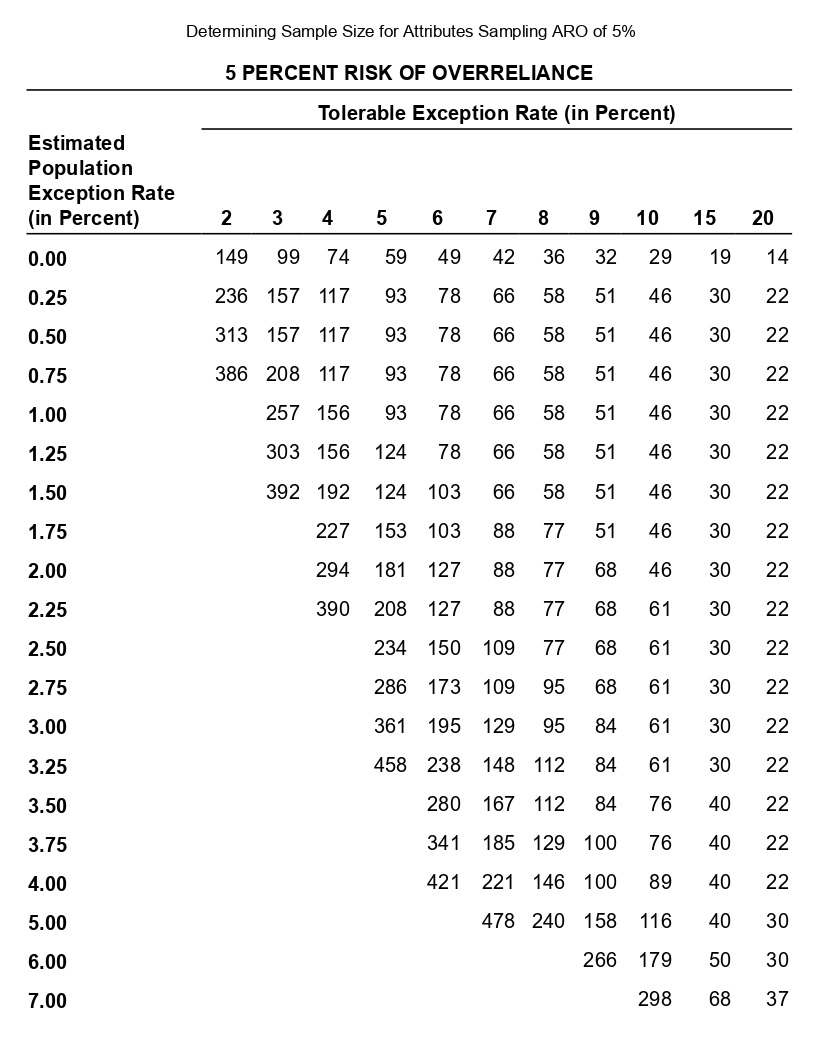

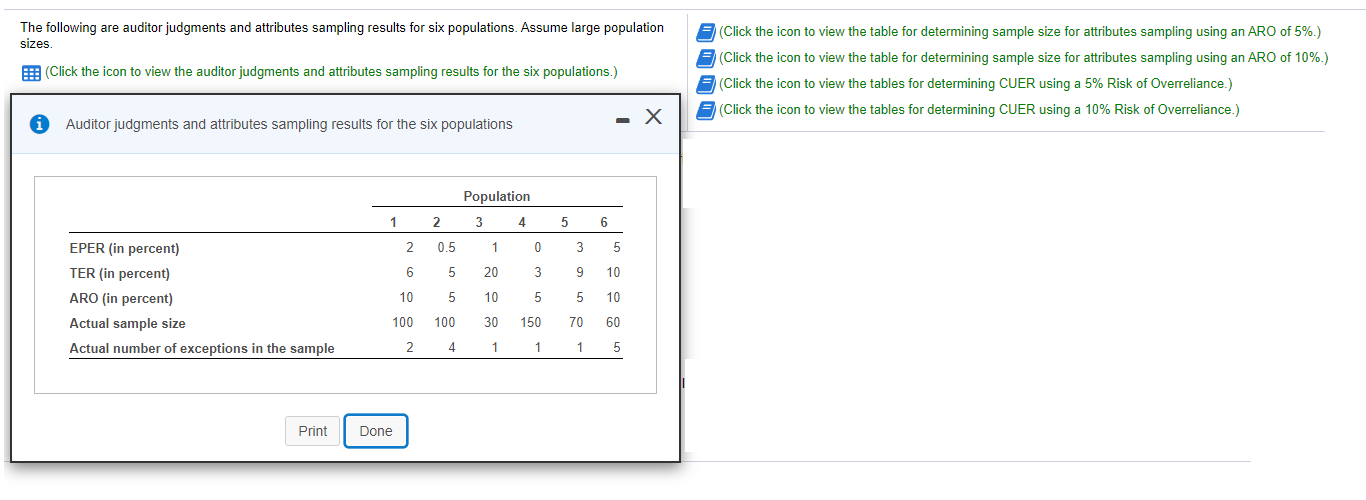

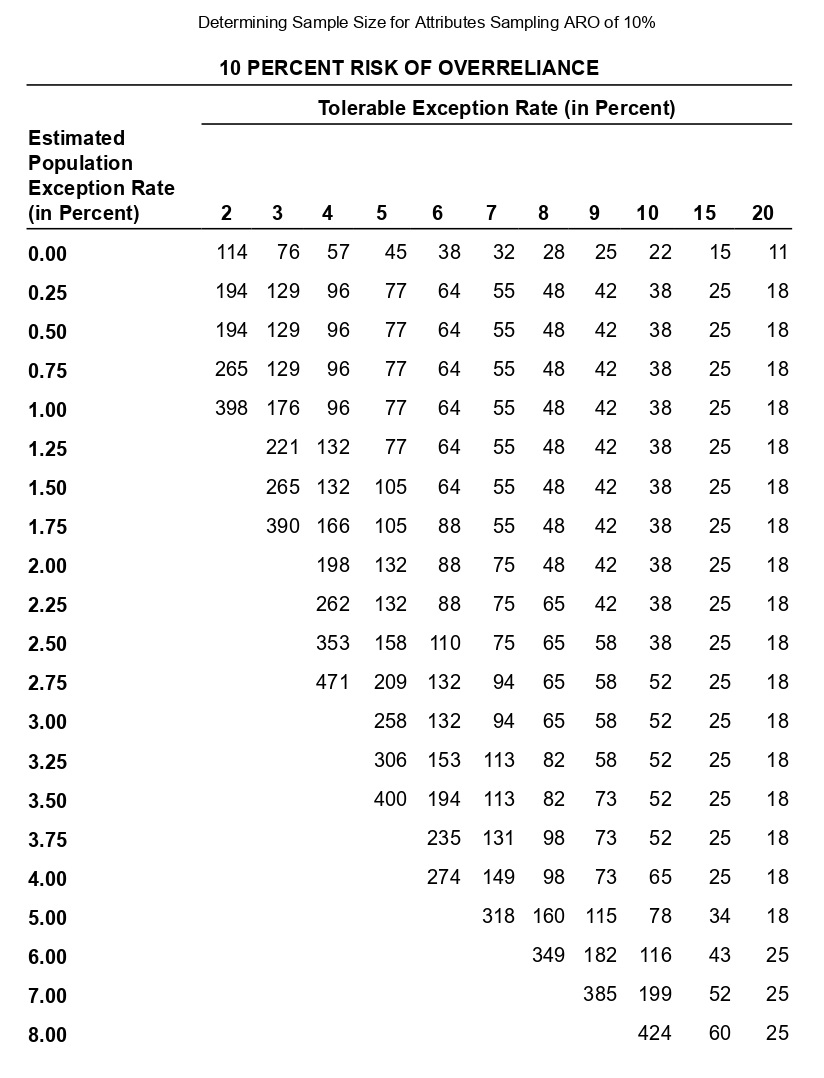

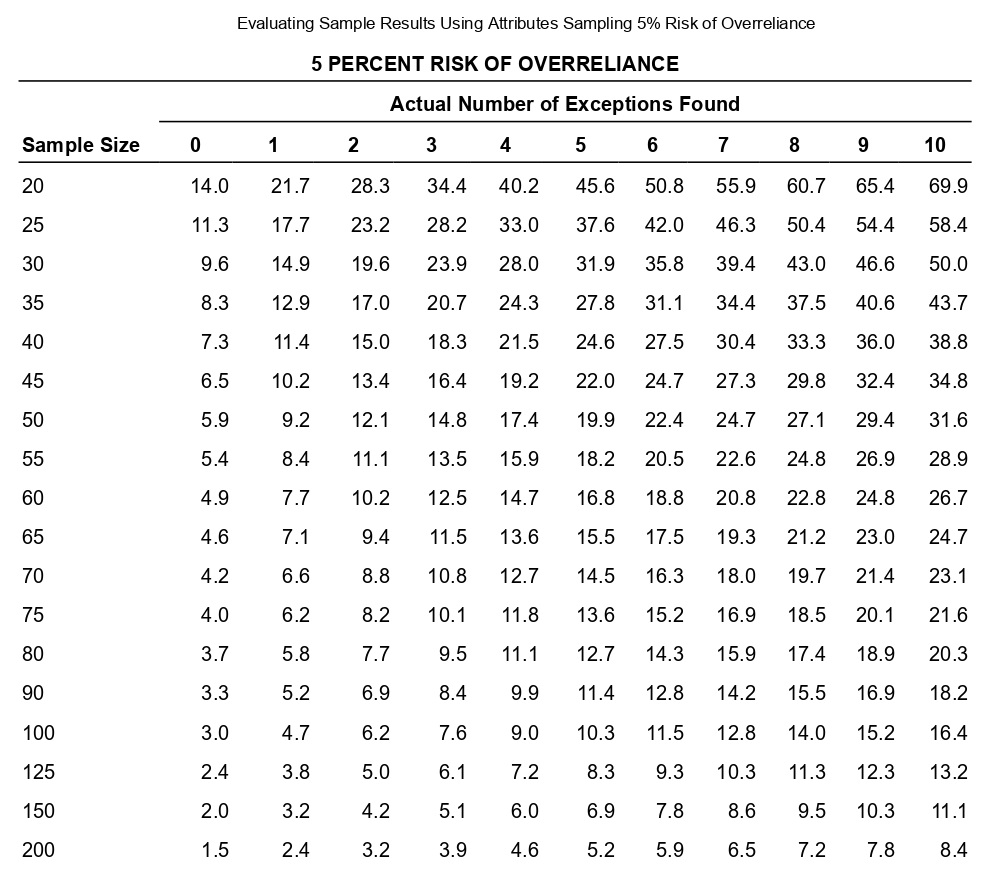

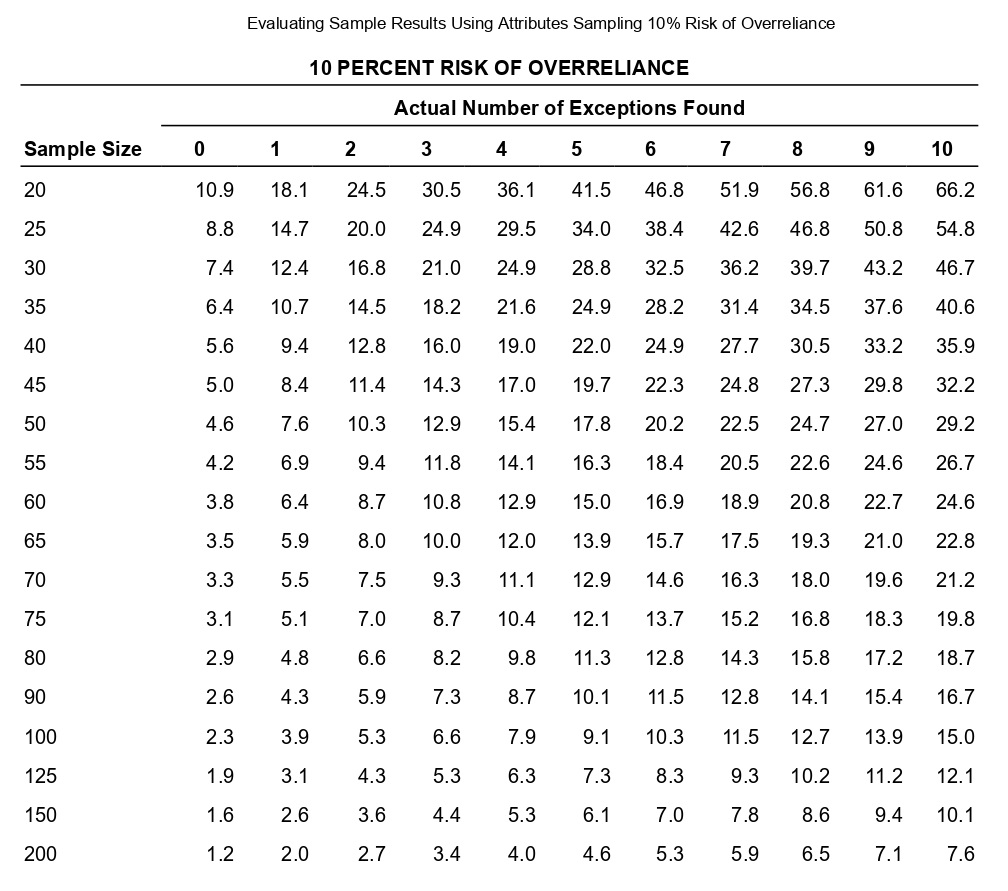

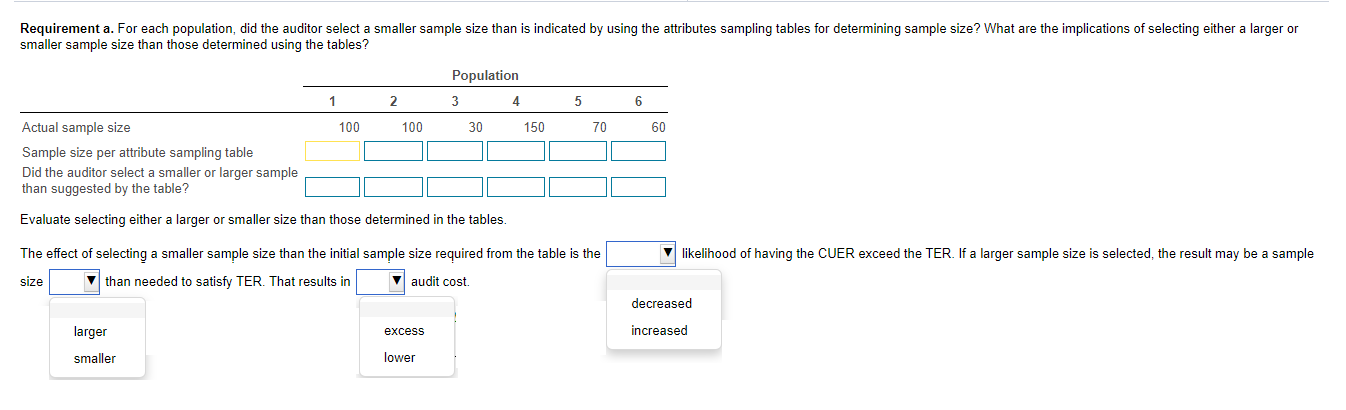

Determining Sample Size for Attributes Sampling ARO of 5% 5 PERCENT RISK OF OVERRELIANCE Tolerable Exception Rate (in Percent) Estimated Population Exception Rate (in Percent) 2 3 4 5 6 7 8 9 1 0 1 5 20 0.00 149 99 74 59 49 42 36 32 29 19 14 0.25 236 157 117 93 78 66 58 51 46 30 22 0.50 313 157 117 93 78 66 58 51 46 30 22 0.75 386 208 117 93 78 66 58 51 46 30 22 1.00 257 156 93 78 66 58 51 46 30 22 1.25 303 156 124 78 66 58 51 46 30 22 1.50 392 192 124 103 66 58 51 46 30 22 1.75 227 153 103 88 77 51 46 30 22 2.00 294 181 127 88 77 68 46 30 22 2.25 390 208 127 88 77 68 61 30 22 2.50 234 150 109 77 68 61 30 22 2.75 286 173 109 95 68 61 30 22 3.00 361 195 129 95 84 61 30 22 3.25 458 238 148 112 84 61 30 22 3.50 280 167 112 84 76 40 22 3.75 341 185 129 100 76 40 22 4.00 421 221 146 100 89 40 22 5.00 478 240 158 116 40 30 6.00 266 179 50 30 7.00 298 68 37 The following are auditor judgments and attributes sampling results for six populations. Assume large population (Click the icon to view the table for determining sample size for attributes sampling using an ARO of 5%.) sizes. (Click the icon to view the table for determining sample size for attributes sampling using an ARO of 10%.) (Click the icon to view the auditor judgments and attributes sampling results for the six populations.) (Click the icon to view the tables for determining CUER using a 5% Risk of Overreliance.) (Click the icon to view the tables for determining CUER using a 10% Risk of Overreliance.) i Auditor judgments and attributes sampling results for the six populations - X Population 1 2 3 4 5 6 EPER (in percent) 2 0.5 1 0 3 5 TER (in percent) 6 5 20 3 9 10 ARO (in percent) 10 5 10 5 5 10 Actual sample size 100 100 30 150 70 60 Actual number of exceptions in the sample 2 4 1 1 5 Print DoneDetermining Sample Size for Attributes Sampling ARO of 10% 10 PERCENT RISK OF OVERRELIANCE Tolerable Exception Rate (in Percent) Estimated Population Exception Rate (in Percent) 2 3 4 5 6 7 8 9 1 0 1 5 20 0.00 114 76 57 45 38 32 28 25 22 15 11 0.25 194 129 96 77 64 55 48 42 38 25 18 0.50 194 129 96 77 64 55 48 42 38 25 18 0.75 265 129 96 77 64 55 48 42 38 25 18 1.00 398 176 96 77 64 55 48 42 38 25 18 1.25 221 132 77 64 55 48 42 38 25 18 1.50 265 132 105 64 55 48 42 38 25 18 1.75 390 166 105 88 55 48 42 38 25 18 2.00 198 132 88 75 48 42 38 25 18 2.25 262 132 88 75 65 42 38 25 18 2.50 353 158 110 75 65 58 38 25 18 2.75 471 209 132 94 65 58 52 25 18 3.00 258 132 94 65 58 52 25 18 3.25 306 153 113 82 58 52 25 18 3.50 400 194 113 82 73 52 25 18 3.75 235 131 98 73 52 25 18 4.00 274 149 98 73 65 25 18 5.00 318 160 115 78 34 18 6.00 349 182 116 43 25 7.00 385 199 52 25 8.00 424 60 25 Evaluating Sample Results Using Attributes Sampling 5% Risk of Overrelianee 5 PERCENT RISK OF OVERRELIANCE Actual Number of Exceptions Found Sample Size 0 1 2 3 4 5 6 7 8 9 10 20 14.0 21.7 28.3 34.4 40.2 45.6 50.8 55.9 60.7 65.4 69.9 25 11.3 17.7 23.2 28.2 33.0 37.6 42.0 46.3 50.4 54.4 58.4 30 9.6 14.9 19.6 23.9 28.0 31.9 35.8 39.4 43.0 46.6 50.0 35 8.3 12.9 17.0 20.7 24.3 27.8 31.1 34.4 37.5 40.6 43.7 40 7.3 11.4 15.0 18.3 21.5 24.6 27.5 30.4 33.3 36.0 38.8 45 6.5 10.2 13.4 16.4 19.2 22.0 24.7 27.3 29.8 32.4 34.8 50 5.9 9.2 12.1 14.8 17.4 19.9 22.4 24.7 27.1 29.4 31.6 55 5.4 8.4 11.1 13.5 15.9 18.2 20.5 22.6 24.8 26.9 28.9 60 4.9 7.7 10.2 12.5 14.7 16.8 18.8 20.8 22.8 24.8 26.7 65 4.6 7.1 9.4 11.5 13.6 15.5 17.5 19.3 21.2 23.0 24.7 70 4.2 6.6 8.8 10.8 12.7 14.5 16.3 18.0 19.7 21.4 23.1 75 4.0 6.2 8.2 10.1 11.8 13.6 15.2 16.9 18.5 20.1 21.6 80 3.7 5.8 7.7 9.5 11.1 12.7 14.3 15.9 17.4 18.9 20.3 90 3.3 5.2 6.9 8.4 9.9 11.4 12.8 14.2 15.5 16.9 18.2 100 3.0 4.7 6.2 7.6 9.0 10.3 11.5 12.8 14.0 15.2 16.4 125 2.4 3.8 5.0 6.1 7.2 8.3 9.3 10.3 11.3 12.3 13.2 150 2.0 3.2 4.2 5.1 6.0 6.9 7.8 8.6 9.5 10.3 11.1 200 1.5 2.4 3.2 3.9 4.6 5.2 5.9 6.5 7.2 7.8 8.4 Evaluating Sample Results Using Attributes Sampling 10% Risk of Overreliance 10 PERCENT RISK OF OVERRELIANCE Actual Number of Exceptions Found Sample Size 0 1 2 3 4 5 6 7 8 9 10 20 10.9 18.1 24.5 30.5 36.1 41.5 46.8 51.9 56.8 61.6 66.2 25 8.8 14.7 20.0 24.9 29.5 34.0 38.4 42.6 46.8 50.8 54.8 30 7.4 12.4 16.8 21.0 24.9 28.8 32.5 36.2 39.7 43.2 46.7 35 6.4 10.7 14.5 18.2 21.6 24.9 28.2 31.4 34.5 37.6 40.6 40 5.6 9.4 12.8 16.0 19.0 22.0 24.9 27.7 30.5 33.2 35.9 45 5.0 8.4 11.4 14.3 17.0 19.7 22.3 24.8 27.3 29.8 32.2 50 4.6 7.6 10.3 12.9 15.4 17.8 20.2 22.5 24.7 27.0 29.2 55 4.2 6.9 9.4 11.8 14.1 16.3 18.4 20.5 22.6 24.6 26.7 60 3.8 6.4 8.7 10.8 12.9 15.0 16.9 18.9 20.8 22.7 24.6 65 3.5 5.9 8.0 10.0 12.0 13.9 15.7 17.5 19.3 21.0 22.8 70 3.3 5.5 7.5 9.3 11.1 12.9 14.6 16.3 18.0 19.6 21.2 75 3.1 5.1 7.0 8.7 10.4 12.1 13.7 15.2 16.8 18.3 19.8 80 2.9 4.8 5.6 3.2 9.8 11.3 12.8 14.3 15.8 17.2 18.7 90 2.6 4.3 5.9 7.3 8.7 10.1 11.5 12.8 14.1 15.4 16.7 100 2.3 3.9 5.3 6.6 7.9 9.1 10.3 11.5 12.7 13.9 15.0 125 1.9 3.1 4.3 5.3 6.3 7.3 8.3 9.3 10.2 11.2 12.1 150 1.6 2.6 3.6 4.4 5.3 6.1 7.0 7.8 8.6 9.4 10.1 200 1.2 2.0 2.7 3.4 4.0 4.6 5.3 5.9 6.5 7.1 7.6Requirement a. For each population, did the auditor select a smaller sample size than is indicated by using the attributes sampling tables for determining sample size? What are the implications of selecting either a larger or smaller sample size than those determined using the tables? Population 1 2 3 4 5 6 Actual sample size 100 100 30 150 70 60 Sample size per attribute sampling table Did the auditor select a smaller or larger sample than suggested by the table? Evaluate selecting either a larger or smaller size than those determined in the tables. The effect of selecting a smaller sample size than the initial sample size required from the table is the likelihood of having the CUER exceed the TER. If a larger sample size is selected, the result may be a sample size than needed to satisfy TER. That results in audit cost. decreased larger excess increased smaller lowerRequirement b. Calculate the SER and CUER for each population. (Enter your answers to the nearest tenth percent and exclude the percent sign, X.X. Enter a "0" for any zero balances.) Population 1 2 3 4 5 6 EPER (in percent) 2% 0.5% 1% 0 % 3% 5 % TER (in percent) 6% 5% 20 % 3% 9% 10 % ARO (in percent) 10 % 5 % 10 % 5% 5% 10 % Actual sample size 100 100 30 150 70 60 Actual number of exceptions in the sample 2 4 1 5 SER (in percent) CUER (in percent)Requirement c. For which of the six populations should the sample results be considered unacceptable? What options are available to the auditor? The sample results are unacceptable for populations In each of those cases, the exceeds What options are available to the auditor? (Select all that apply.) 3, 5, and 6 ARO ARO O]A. Increase the sample size 3 and 5 CUER CUER OB. Perform other substantive tests to determine whether there 2, 4, and 6 EPER EPER are actually material misstatements in the population. O C. Change TER SER SER O D. Decrease the sample size TER TER DE. Change ARORequirement d. Why is analysis of the exceptions necessary even when the populations are considered acceptable? Analysis of exceptions Y necessary when the population is acceptable because Y is an acceptable population will yield valid results regarding population misstatements. is not - the auditor still needs to determine the adual dollar value of misstatements in the population. the auditor wants to determine the nature and cause of all exceptions. Requirement e. For the following terms, identify which is an audit decision, a nonstatistical estimate made by the auditor, a sample result, and a statistical conclusion about the population: 1) EPER l _ 2) TER 3) ARC Audit decision ) Actual sample size Nonstatistical estimate made by the auditor Sample result 5 Actual number of exceptions in the sample 5 BER r) CUER v Statistical conclusion about the population v ( ( ( (4 ( ( (