Answered step by step

Verified Expert Solution

Question

1 Approved Answer

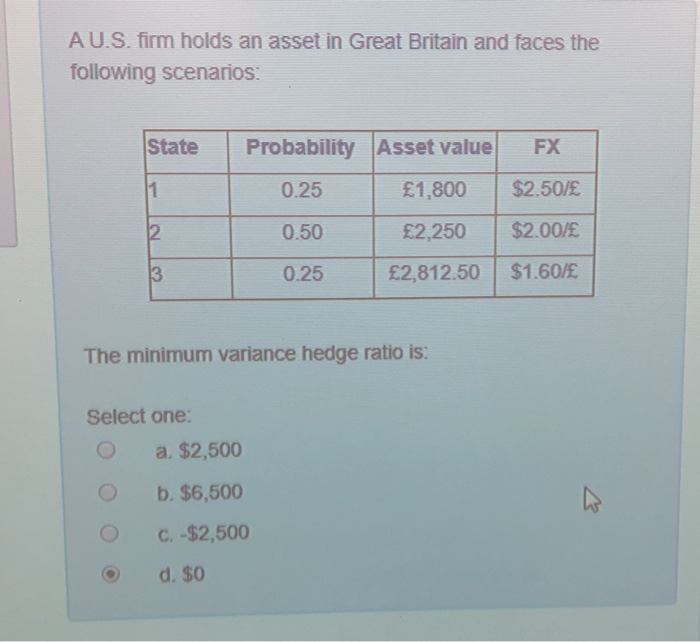

AU.S. firm holds an asset in Great Britain and faces the following scenarios: State Probability Asset value FX 0.25 1,800 $2.50/ 0.50 2,250 $2.00/ 0.25

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Grow Faster Angel Investors And Real Estate

Authors: Benjamin Stone

1st Edition

979-8856612638