Answered step by step

Verified Expert Solution

Question

1 Approved Answer

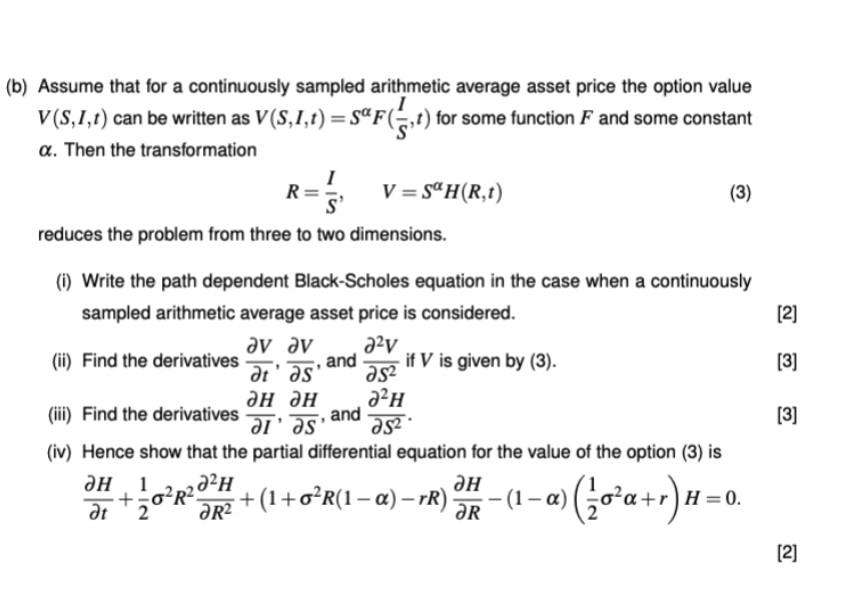

(b) Assume that for a continuously sampled arithmetic average asset price the option value I V(S,1,1) can be written as V(S,1,1) = sF (r) for

(b) Assume that for a continuously sampled arithmetic average asset price the option value I V(S,1,1) can be written as V(S,1,1) = sF (r) for some function F and some constant V=sH(R,1) a. Then the transformation R= (3) reduces the problem from three to two dimensions. [ [2] [3] . (1) Write the path dependent Black-Scholes equation in the case when a continuously sampled arithmetic average asset price is considered. av av 22v (ii) Find the derivatives and if V is given by (3). t'as as2 aHaH ? (iii) Find the derivatives and al' as' 232 (iv) Hence show that the partial differential equation for the value of the option (3) is aH 1 22H aH +-o at (1-a) R2 + (1+0-R(1 a) rR) 2 IR H. [3] 1 OR JR? (jo+a+r)h=0 [2]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis For Financial Management

Authors: Robert C. Higgins

10th International Edition

007108648X, 9780071086486