Answered step by step

Verified Expert Solution

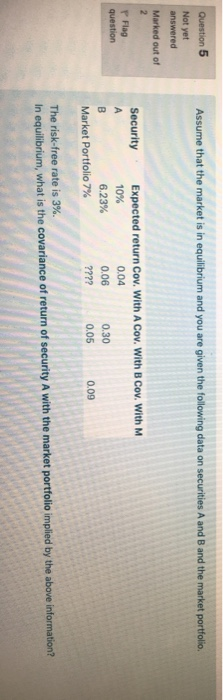

Question

1 Approved Answer

b. based on the given information in the previous question, assume that you have OMR10,000 available to invest. if you sell short OMR6,000 of security

b. based on the given information in the previous question, assume that you have OMR10,000 available to invest. if you sell short OMR6,000 of security A, and invest all the available funds in security B, what is the beta of stock A and B, respectively?

c. based on the previous question, assume that you have OMR10,000 available to invest. if you sell short OMR6,000 of security A and invest all the available funds in security B, what is the portfolios beta?

d. based on the information provided in the previous question, suppose you can form any portfolio from stocks A and B, with short selling and no leverage. You want expected returns of 15%. what will the standard deviation of your portfolio be closet to?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Algorithms Understanding Algorithmic Systems From The Outside In Foundations And Trends

Authors: Danaë Metaxa, Joon Sung Park, Ronald E Robertson, Karrie Karahalios, Christo Wilson, Jeff Hancock, Christian Sandvig

1st Edition

1680839160, 978-1680839166