Answered step by step

Verified Expert Solution

Question

1 Approved Answer

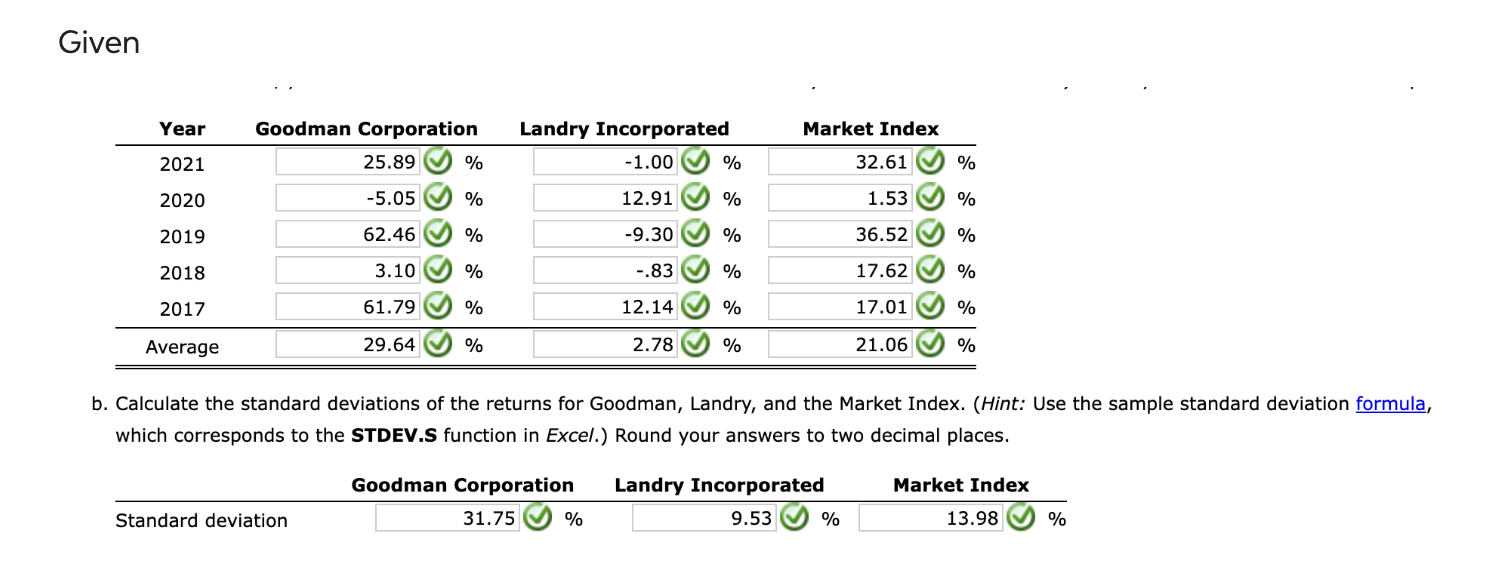

b. Calculate the standard deviations of the returns for Goodman, Landry, and the Market Index. (Hint: Use the sample standard deviation formula, which corresponds to

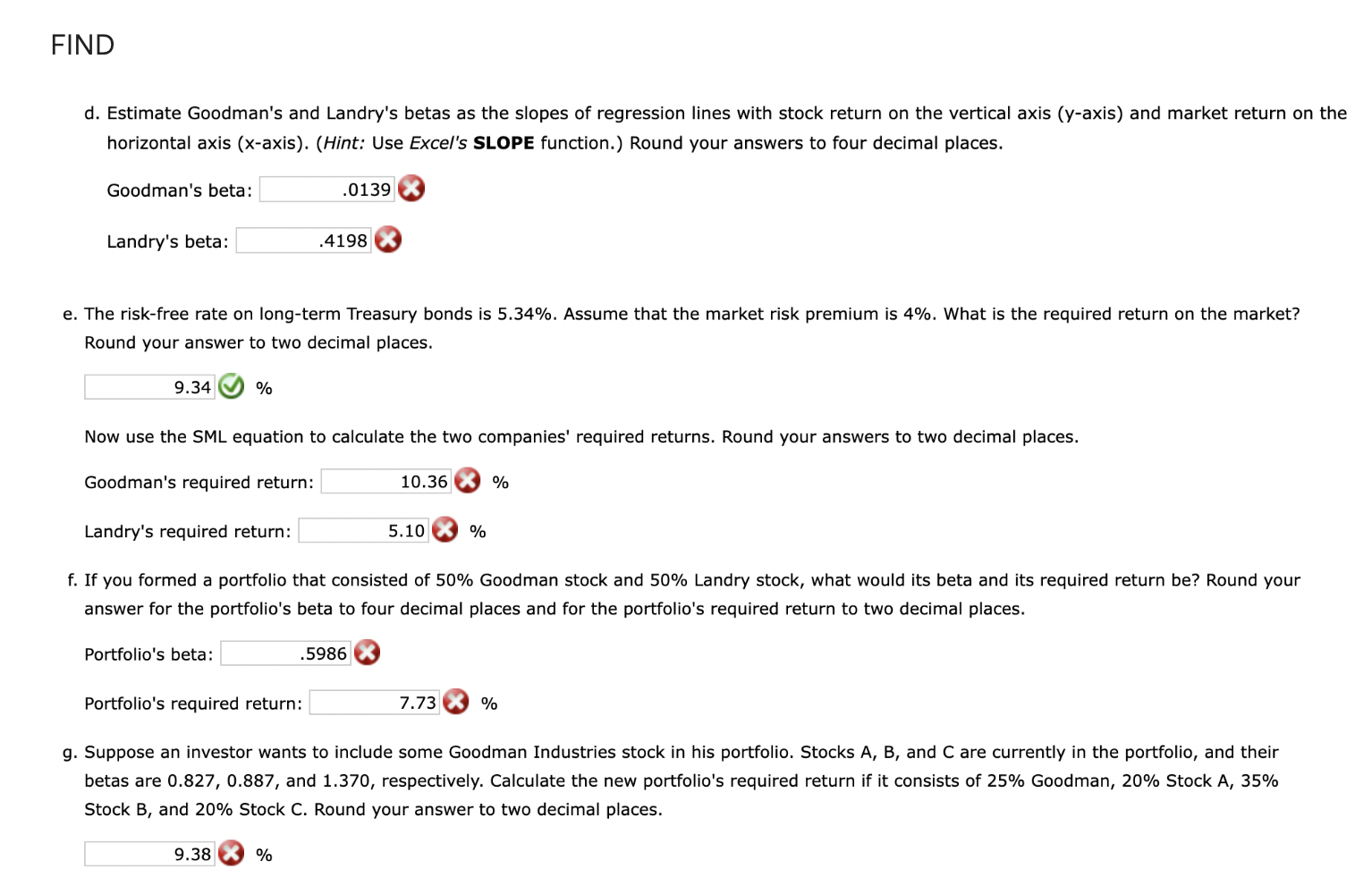

b. Calculate the standard deviations of the returns for Goodman, Landry, and the Market Index. (Hint: Use the sample standard deviation formula, which corresponds to the STDEV.S function in Excel.) Round your answers to two decimal places. FIND d. Estimate Goodman's and Landry's betas as the slopes of regression lines with stock return on the vertical axis ( y-axis) and market return on the horizontal axis (x-axis). (Hint: Use Excel's SLOPE function.) Round your answers to four decimal places. Goodman's beta: Landry's beta: e. The risk-free rate on long-term Treasury bonds is 5.34%. Assume that the market risk premium is 4%. What is the required return on the market? Round your answer to two decimal places. % Now use the SML equation to calculate the two companies' required returns. Round your answers to two decimal places. Goodman's required return: % Landry's required return: % f. If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would its beta and its required return be? Round your answer for the portfolio's beta to four decimal places and for the portfolio's required return to two decimal places. Portfolio's beta: Portfolio's required return: % g. Suppose an investor wants to include some Goodman Industries stock in his portfolio. Stocks A, B, and C are currently in the portfolio, and their betas are 0.827,0.887, and 1.370 , respectively. Calculate the new portfolio's required return if it consists of 25% Goodman, 20% Stock A, 35% Stock B, and 20% Stock C. Round your answer to two decimal places. %

b. Calculate the standard deviations of the returns for Goodman, Landry, and the Market Index. (Hint: Use the sample standard deviation formula, which corresponds to the STDEV.S function in Excel.) Round your answers to two decimal places. FIND d. Estimate Goodman's and Landry's betas as the slopes of regression lines with stock return on the vertical axis ( y-axis) and market return on the horizontal axis (x-axis). (Hint: Use Excel's SLOPE function.) Round your answers to four decimal places. Goodman's beta: Landry's beta: e. The risk-free rate on long-term Treasury bonds is 5.34%. Assume that the market risk premium is 4%. What is the required return on the market? Round your answer to two decimal places. % Now use the SML equation to calculate the two companies' required returns. Round your answers to two decimal places. Goodman's required return: % Landry's required return: % f. If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would its beta and its required return be? Round your answer for the portfolio's beta to four decimal places and for the portfolio's required return to two decimal places. Portfolio's beta: Portfolio's required return: % g. Suppose an investor wants to include some Goodman Industries stock in his portfolio. Stocks A, B, and C are currently in the portfolio, and their betas are 0.827,0.887, and 1.370 , respectively. Calculate the new portfolio's required return if it consists of 25% Goodman, 20% Stock A, 35% Stock B, and 20% Stock C. Round your answer to two decimal places. % Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: J. Chris Leach, Ronald W. Melicher

7th Edition

0357442040, 978-0357442043