Answered step by step

Verified Expert Solution

Question

1 Approved Answer

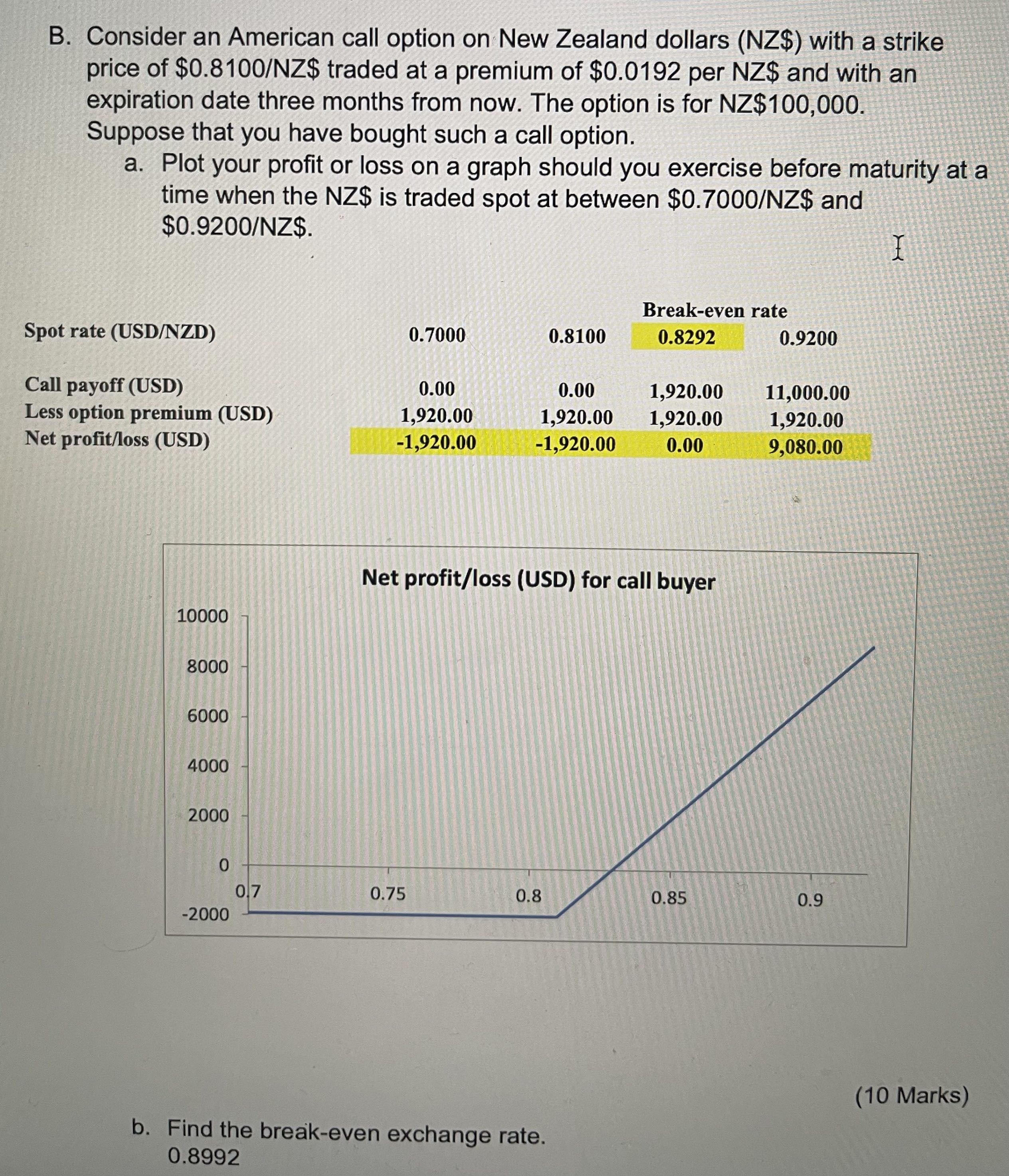

B. Consider an American call option on New Zealand dollars (NZ$) with a strike price of ( $ 0.8100 / N Z $ ) traded

B. Consider an American call option on New Zealand dollars (NZ\\$) with a strike price of \\( \\$ 0.8100 / N Z \\$ \\) traded at a premium of \\( \\$ 0.0192 \\) per \\( N Z \\$ \\) and with an expiration date three months from now. The option is for \\( \\mathrm{NZ} \\$ 100,000 \\). Suppose that you have bought such a call option. a. Plot your profit or loss on a graph should you exercise before maturity at a time when the NZ\\$ is traded spot at between \\( \\$ 0.7000 / \\mathrm{NZ} \\$ \\) and \\( \\$ 0.9200 / \\mathrm{NZ} \\). (10 Marks) b. Find the break-even exchange rate. 0.8992

B. Consider an American call option on New Zealand dollars (NZ\\$) with a strike price of \\( \\$ 0.8100 / N Z \\$ \\) traded at a premium of \\( \\$ 0.0192 \\) per \\( N Z \\$ \\) and with an expiration date three months from now. The option is for \\( \\mathrm{NZ} \\$ 100,000 \\). Suppose that you have bought such a call option. a. Plot your profit or loss on a graph should you exercise before maturity at a time when the NZ\\$ is traded spot at between \\( \\$ 0.7000 / \\mathrm{NZ} \\$ \\) and \\( \\$ 0.9200 / \\mathrm{NZ} \\). (10 Marks) b. Find the break-even exchange rate. 0.8992 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Political Economy Of Trade Finance Export Credit Agencies The Paris Club And The IMF

Authors: Pamela Blackmon

1st Edition

1138780561,1317672917