Answered step by step

Verified Expert Solution

Question

1 Approved Answer

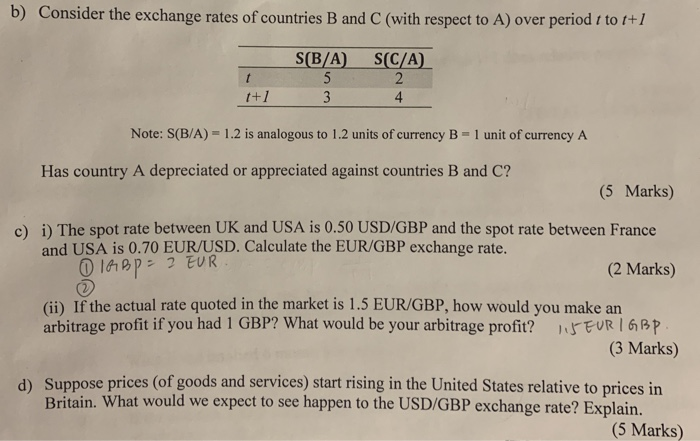

b) Consider the exchange rates of countries B and C (with respect to A) over period t to +1 S(B/A) S(CC/A) t+1 4 Note: S(B/A)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mathematical And Statistical Methods For Actuarial Sciences And Finance

Authors: Marco Corazza , Claudio Pizzi

1st Edition

3319024981, 331902499X, 9783319024998