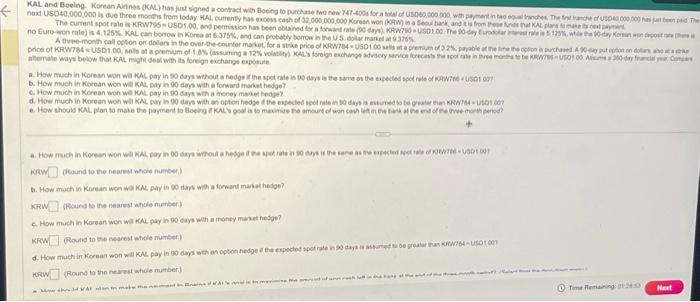

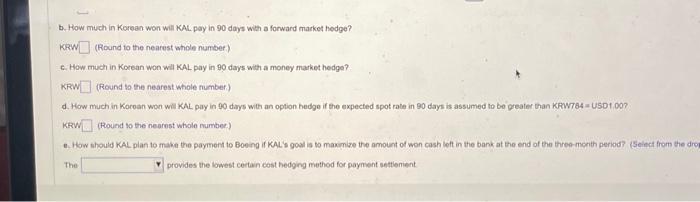

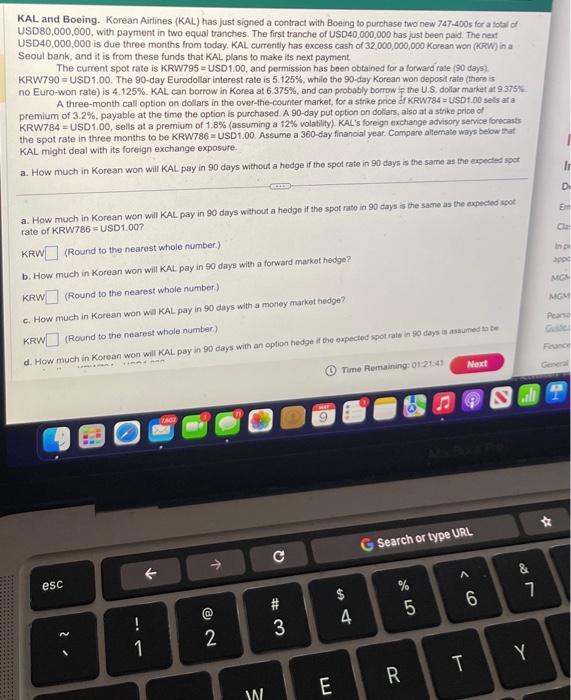

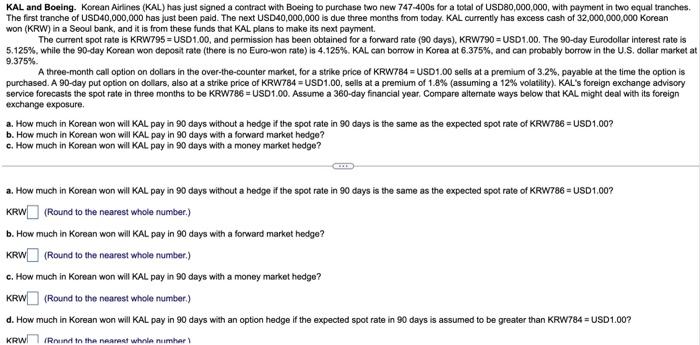

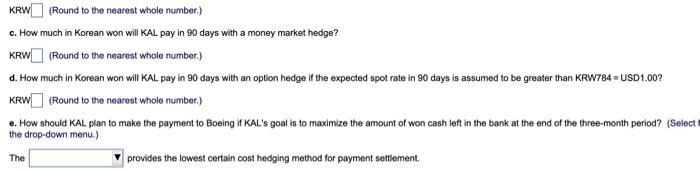

b. How much in Koroan woo wa kA. pay in 90 degs weth a fonkard maket hedge? 6. How much in Korean won we KAL. pay in 90 dayt woh a money masel hedje? 6. How shoub KM. plan to made the popment b boeing i KWu t. How much in Karean woen wo. KN. pay in 00 dew wath a tow ard masel hedge? KFRW (foumd to the harest while number) c. How much in Korsan woen wil KuL pay h 90 cays weh a moncy mulut hegpe? KRWZ (Rovits to Fe mearest ahole rumber) krow (Round to the nevest ahice nutber) b. How much in Korean won will KAL. pay in 90 days with a forward market hedge? KRW (Round to the nearest ahole number) c. How much in Korean won wil KAL pay in 90 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won wi. KAL pay in 90 days with an option hedge if the expected spot rale in 90 days is assumed to be greater than KFWr 84 = USDI , og? KRW (Round to the nearest whole mumber) a. How thould KAL plan to make the payment to Boeing if KAL's goul is to maximise the amount of won cash left in the bank at the end of the three-month period? (SEelect from the dre The provides the lowest certan cost hedging method for payment settienient KAL and Boeing. Korean Airlines (KAL) has just signed a contract with Boeing to purchase two new 747400 s for a fotal of USD 80,000,000, with payment in two equal tranches. The first tranche of USD 40,000,000 has just been paid. The neit USD40,000,000 is due three months from today. KAL currently has excess cash of 32,000,000,000 Korean won (KCWW) in a Seoul bank, and it is from these funds that KAL plans to make its next payment. The current spot rate is KRW795 = USD1.00, and permission has been obtained for a forward rate (90 days) KRW790 = USD1.00. The 90-day Eurodollar interest rate is 5.125\%, while the 90 -day Korean won deposit rate (there is no Euro-won rate) is 4.125%. KAL. can borrow in Korea at 6.375%, and can probably borrow ie the U.S. dollar marketat 9375% A three-month call option on dollars in the over-the-counter market, for a strike price df KRW784 =USD 1:00 sells at a premium of 3.2%, payable at the time the option is purchased. A 90 -day put option on doliars, also at a strike price of KRW784 = USD1.00, sells at a premium of 1,B% (assuming a 12% volatility). KAL''s foreign exchange advisory service forecaats the spot rate in three months to be KRW786 = USD1.00. Assume a 360-day finanoial year. Compare aliemate ways beiow ihat. KAL might deal with its foreign exchange exposure. a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected soet a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot: rate of KRW786 = USD1.00? KRW (Round to the nearest whole number.) b. How much in Korean won wil KAL pay in 90 days with a forward markat hedge? KRW (Round to the nearest whole number) c. How much in Korean won wil KAL pay in 90 days with a money market hedge? d. How much in Korean won Wil KAL pay in 90 days with an option hedge it the expected spot ratio in 90 days is asamed to be KRW (Round to the nearest whole number.) (b) Tume Aemaining: o1:21:4! KAL and Boeing. Korean Airlines (KAL) has just signed a contract with Boeing to purchase two new 747400 s for a total of USD80,000,000, with payment in two equal tranches. The first tranche of USD 40,000,000 has just been paid. The next USD40,000,000 is due three months from today. KAL currently has excess cash of 32,000,000,000 Korean won (KRW) in a Secul bank, and it is from these funds that KAL plans to make its next payment. The current spot rate is KRW795 = USD1.00, and permission has been obtained for a forward rate (90 days), KRW790= USD1.00. The 90-day Eurodollar interest rate is 5.125\%, while the 90-day Korean won deposit rate (there is no Euro-won rate) is 4.125\%. KAL can borrow in Korea at 6.375\%, and can probably borrow in the U.S, dollar market at 9.375% A three-month call option on dollars in the over-the-counter market, for a strike price of KRW784 = USD1.00 sells at a premium of 3.2%, payable at the time the option is purchased. A 90 -day put option on dollars, also at a strike price of KRW784 = USD1.00, sells at a premium of 1.8% (assuming a 12% volatility). KAL's foreign exchange advisory service forecasts the spot rate in three months to be KRW786= USD1.00. Assume a 360-day financial year, Compare alternate ways below that KAL might deal with its foreign exchange exposure. a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot rate of KRW786 = USD1.00? b. How much in Korean won will KAL pay in 90 days with a forward market hedge? c. How much in Korean won will KAL pay in 90 days with a money market hedge? a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot rate of KRW786= USD1.00? KRW (Round to the nearest whole number.) b. How much in Korean won will KAL pay in 90 days with a forward market hedge? KRV (Round to the nearest whole number.) c. How much in Korean won will KAL pay in 90 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won will KAL pay in 90 days with an option hedge if the expected spot rate in 90 days is assumed to be greater than KRW784 = USD1.00? KRW (Rmund in the nearast whila numhae) KRW (Round to the nearest whole number.) c. How much in Korean won will KAL pay in $0 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won will KAL pay in 90 days with an option hedge if the expected spot rate in 90 days is assumed to be greater than KRW784 = USD1.00? KRW (Round to the nearest whole number.) e. How should KAL plan to make the payment to Boeing if KAL's goal is to maximize the amount of won cash left in the bank at the end of the three-month period? (Select the drop-down menu.) The provides the lowest certain cost hedging method for payment settlement. b. How much in Koroan woo wa kA. pay in 90 degs weth a fonkard maket hedge? 6. How much in Korean won we KAL. pay in 90 dayt woh a money masel hedje? 6. How shoub KM. plan to made the popment b boeing i KWu t. How much in Karean woen wo. KN. pay in 00 dew wath a tow ard masel hedge? KFRW (foumd to the harest while number) c. How much in Korsan woen wil KuL pay h 90 cays weh a moncy mulut hegpe? KRWZ (Rovits to Fe mearest ahole rumber) krow (Round to the nevest ahice nutber) b. How much in Korean won will KAL. pay in 90 days with a forward market hedge? KRW (Round to the nearest ahole number) c. How much in Korean won wil KAL pay in 90 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won wi. KAL pay in 90 days with an option hedge if the expected spot rale in 90 days is assumed to be greater than KFWr 84 = USDI , og? KRW (Round to the nearest whole mumber) a. How thould KAL plan to make the payment to Boeing if KAL's goul is to maximise the amount of won cash left in the bank at the end of the three-month period? (SEelect from the dre The provides the lowest certan cost hedging method for payment settienient KAL and Boeing. Korean Airlines (KAL) has just signed a contract with Boeing to purchase two new 747400 s for a fotal of USD 80,000,000, with payment in two equal tranches. The first tranche of USD 40,000,000 has just been paid. The neit USD40,000,000 is due three months from today. KAL currently has excess cash of 32,000,000,000 Korean won (KCWW) in a Seoul bank, and it is from these funds that KAL plans to make its next payment. The current spot rate is KRW795 = USD1.00, and permission has been obtained for a forward rate (90 days) KRW790 = USD1.00. The 90-day Eurodollar interest rate is 5.125\%, while the 90 -day Korean won deposit rate (there is no Euro-won rate) is 4.125%. KAL. can borrow in Korea at 6.375%, and can probably borrow ie the U.S. dollar marketat 9375% A three-month call option on dollars in the over-the-counter market, for a strike price df KRW784 =USD 1:00 sells at a premium of 3.2%, payable at the time the option is purchased. A 90 -day put option on doliars, also at a strike price of KRW784 = USD1.00, sells at a premium of 1,B% (assuming a 12% volatility). KAL''s foreign exchange advisory service forecaats the spot rate in three months to be KRW786 = USD1.00. Assume a 360-day finanoial year. Compare aliemate ways beiow ihat. KAL might deal with its foreign exchange exposure. a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected soet a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot: rate of KRW786 = USD1.00? KRW (Round to the nearest whole number.) b. How much in Korean won wil KAL pay in 90 days with a forward markat hedge? KRW (Round to the nearest whole number) c. How much in Korean won wil KAL pay in 90 days with a money market hedge? d. How much in Korean won Wil KAL pay in 90 days with an option hedge it the expected spot ratio in 90 days is asamed to be KRW (Round to the nearest whole number.) (b) Tume Aemaining: o1:21:4! KAL and Boeing. Korean Airlines (KAL) has just signed a contract with Boeing to purchase two new 747400 s for a total of USD80,000,000, with payment in two equal tranches. The first tranche of USD 40,000,000 has just been paid. The next USD40,000,000 is due three months from today. KAL currently has excess cash of 32,000,000,000 Korean won (KRW) in a Secul bank, and it is from these funds that KAL plans to make its next payment. The current spot rate is KRW795 = USD1.00, and permission has been obtained for a forward rate (90 days), KRW790= USD1.00. The 90-day Eurodollar interest rate is 5.125\%, while the 90-day Korean won deposit rate (there is no Euro-won rate) is 4.125\%. KAL can borrow in Korea at 6.375\%, and can probably borrow in the U.S, dollar market at 9.375% A three-month call option on dollars in the over-the-counter market, for a strike price of KRW784 = USD1.00 sells at a premium of 3.2%, payable at the time the option is purchased. A 90 -day put option on dollars, also at a strike price of KRW784 = USD1.00, sells at a premium of 1.8% (assuming a 12% volatility). KAL's foreign exchange advisory service forecasts the spot rate in three months to be KRW786= USD1.00. Assume a 360-day financial year, Compare alternate ways below that KAL might deal with its foreign exchange exposure. a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot rate of KRW786 = USD1.00? b. How much in Korean won will KAL pay in 90 days with a forward market hedge? c. How much in Korean won will KAL pay in 90 days with a money market hedge? a. How much in Korean won will KAL pay in 90 days without a hedge if the spot rate in 90 days is the same as the expected spot rate of KRW786= USD1.00? KRW (Round to the nearest whole number.) b. How much in Korean won will KAL pay in 90 days with a forward market hedge? KRV (Round to the nearest whole number.) c. How much in Korean won will KAL pay in 90 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won will KAL pay in 90 days with an option hedge if the expected spot rate in 90 days is assumed to be greater than KRW784 = USD1.00? KRW (Rmund in the nearast whila numhae) KRW (Round to the nearest whole number.) c. How much in Korean won will KAL pay in $0 days with a money market hedge? KRW (Round to the nearest whole number.) d. How much in Korean won will KAL pay in 90 days with an option hedge if the expected spot rate in 90 days is assumed to be greater than KRW784 = USD1.00? KRW (Round to the nearest whole number.) e. How should KAL plan to make the payment to Boeing if KAL's goal is to maximize the amount of won cash left in the bank at the end of the three-month period? (Select the drop-down menu.) The provides the lowest certain cost hedging method for payment settlement